No major reports from Canada this week, which means CAD traders will be looking at other catalysts for volatility.

Here are some leads on potential market movers:

Monthly GDP (Jan 31, 1:30 pm GMT)

- The economy shrank by 0.1% October, which marked the first contraction since February

- CAD barely reacted to the report as traders expect the impact of the U.S. auto strike to rebound in the next release

- Markets expect to see a 0.1% uptick in November

Market risk appetite and crude oil price action

- Coronavirus concerns and its impact on travel and logistics (and therefore crude oil) patterns can weigh on the oil-related Canadian dollar

- Britain’s scheduled exit from the EU at the end of the month could inspire volatility among high-yielding currencies like the Loonie

- Top-tier economic events such as the FOMC and BOE’s policy announcements, as well as Uncle Sam’s advance GDP data, can cause volatility among major currencies

Technical snapshot

- Stochastic and Bollinger Bands are pointing at CAD’s “oversold” conditions against USD and JPY

- Williams %R labels CAD as “oversold” against CHF, USD, and JPY

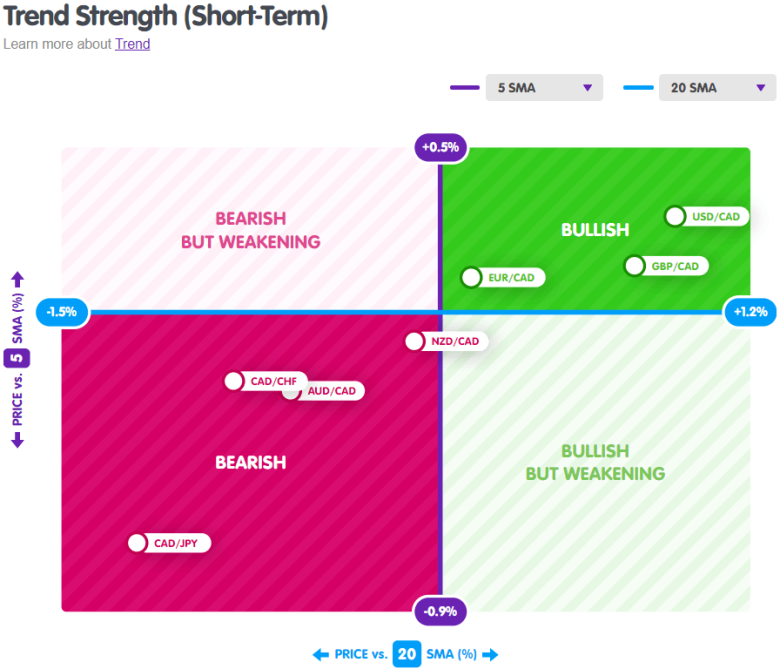

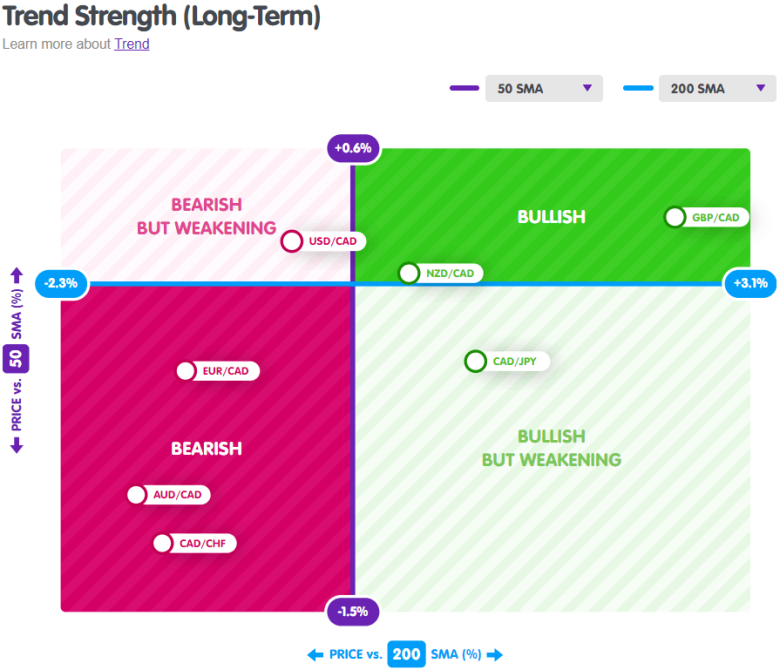

- CAD/JPY is “bullish but weakening” on long-term SMAs and “bearish” with shorter-term SMAs

- USD/CAD is “bullish” compared to short-term SMAs and “bearish but weakening” with longer-term SMAs

Missed last week’s price action? Read CAD’s price recap for January 20 – 24!