Wednesday should have been a good day for the U.S. dollar.

Minutes from the Federal Reserve’s June meeting showed policymakers growing more worried about inflation. That’s usually the kind of news that pushes a currency higher.

Instead, the dollar fell against every major currency except the yen.

New Zealand’s central bank, meanwhile, actually raised rates. Its currency did what the textbook predicts: it rose.

Both central banks leaned hawkish, but only one currency got rewarded for it, and that gap tells us a lot about what traders are actually focused on.

What Actually Happened?

Two events arrived within hours of each other. Both carried a hawkish tone, meaning a policy stance that favors higher interest rates to fight inflation.

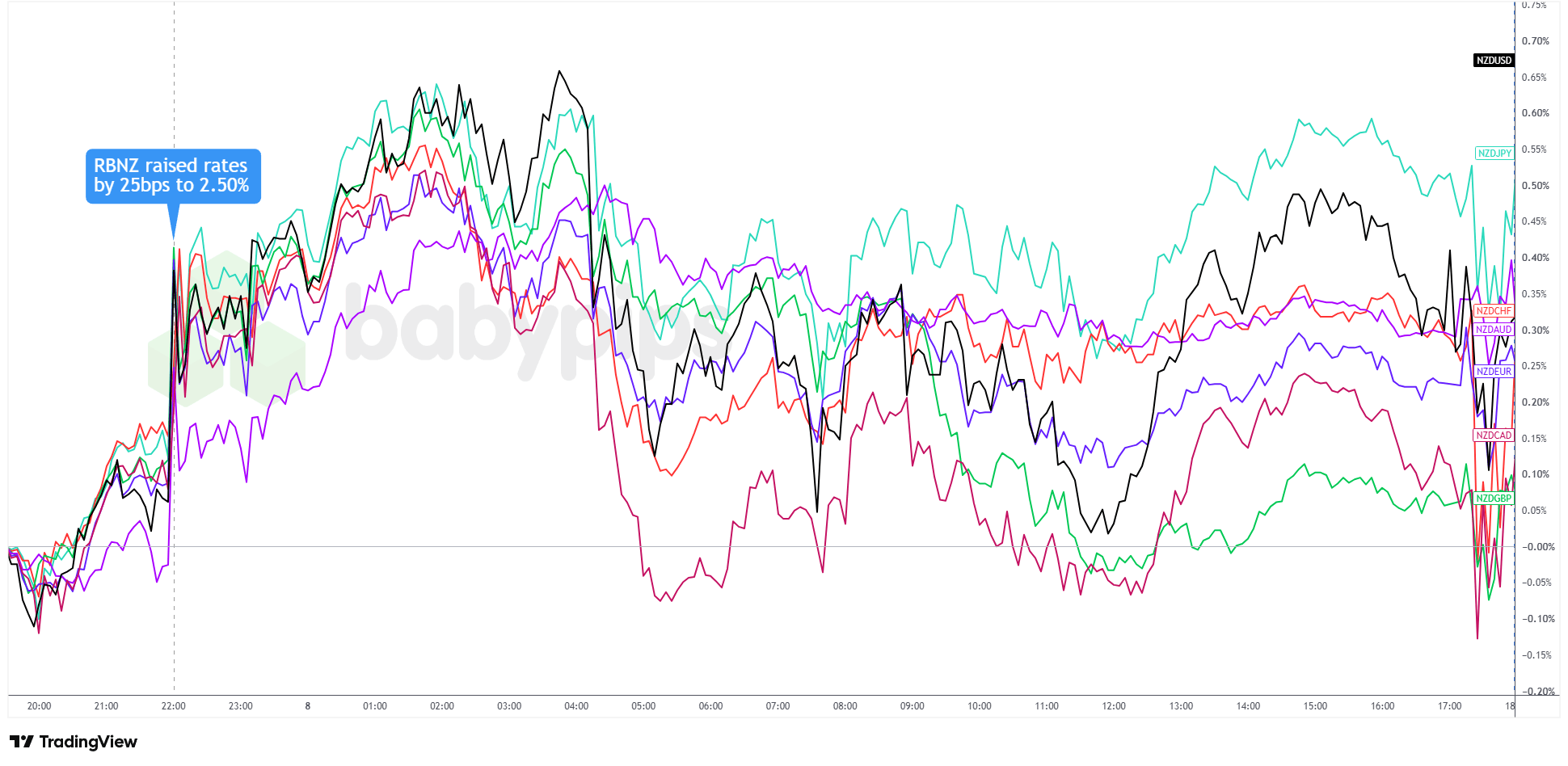

First, the Reserve Bank of New Zealand raised its Official Cash Rate by 25 basis points to 2.50%. Going in, market-implied odds of a hike had eased to under 70%, down from over 80% a week earlier. The move carried genuine surprise.

The New Zealand dollar responded by catching fresh bids and extending higher in an immediate reaction to the decision, becoming the day’s strongest major currency.

New Zealand Dollar vs. Major Currencies: 5-min

Overlay of NZD vs. Major Currencies Chart Faster with TradingView

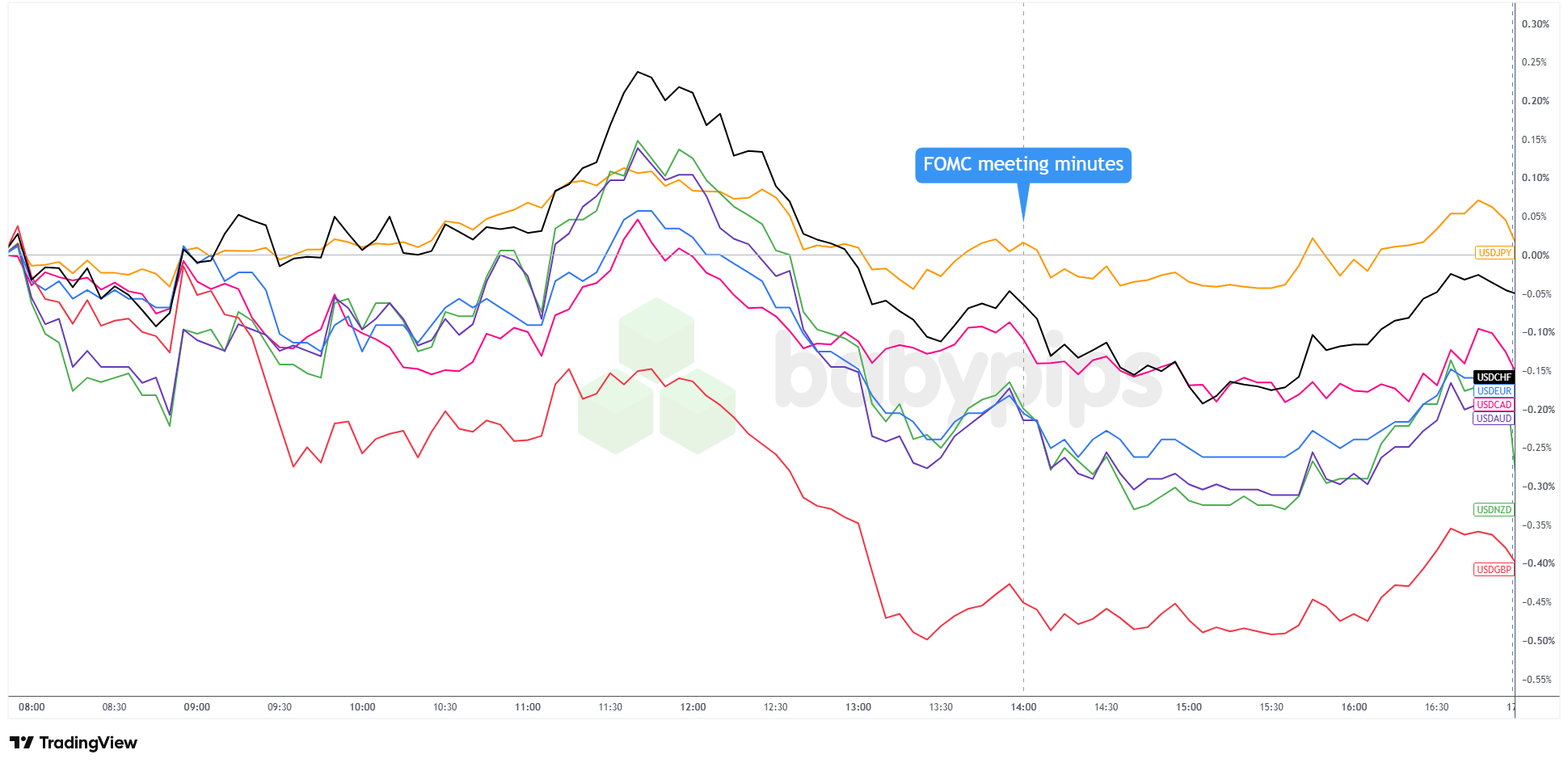

Then, near the end of the trading day, the Fed released its June meeting minutes, published weeks after the fact. This batch showed a few officials had seen a case for raising rates back in June. Inflation concern was building inside the room.

By the usual playbook, that should have supported the dollar too. It didn’t. The dollar index slipped roughly 0.15% on the day, losing ground against the euro, pound, Canadian dollar, Swiss franc, and Kiwi. It only held against the yen.

U.S. Dollar vs. Major Currencies: 5-min

Overlay of USD vs. Major Currencies Chart Faster with TradingView

Promoted: Hawkish News Doesn’t Always Move Markets the Way You Expect.

When central bank headlines hit, the first move doesn’t always tell the full story. FinancialJuice helps traders track real time market moving news, central bank updates, and risk sentiment shifts so they’re not trading yesterday’s read.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Why Did This Happen?

A hawkish signal isn’t the same thing as a hawkish surprise. And on any given day, surprise isn’t the only thing moving a currency.

Start with what markets had already priced in. The RBNZ hike had meaningful odds going into the decision, so part of the move was likely baked into the Kiwi ahead of time. What pushed it higher was probably the slice traders hadn’t fully priced, not the rate hike by itself.

The dollar’s story was different, and the reaction pattern tells the tale. The dollar index popped briefly after the Fed minutes hit the tape, then reversed and drifted lower into the close.

That spike-then-fade pattern shows up often enough around scheduled releases to be worth watching. Traders react to the first headline, then adjust once they’ve had time to read the full document and catch the caveats.

There was also a bigger backdrop in play. Earlier that day, President Trump declared the ceasefire between the U.S. and Iran “over” after a fresh exchange of strikes. That escalation seems to have pulled broader risk sentiment in a direction that mattered more for currency positioning than the Fed’s debate over a meeting that happened weeks earlier.

When risk sentiment turns, capital flows and hedging demand can overpower a single rate signal.

Put it all together, and the dollar had a tough setup: a hawkish signal that was already partly expected, a document traders needed time to digest, and a fresh geopolitical shock competing for attention. That’s a lot standing in the way of a clean “hawkish Fed equals stronger dollar” reaction.

What Does This Mean for Markets?

Here’s the practical takeaway for any new trader using interest rate differentials as a shortcut for currency direction: rate expectations matter, but they’re one input among several. How much a signal moves a currency often depends on how much of it the market had already absorbed beforehand.That logic carries into the rest of the week. Thursday brings the European Central Bank’s account of its own June meeting, alongside US jobless claims and China’s CPI and PPI data. Each carries its own rate-expectation content. Each will land against the same competing risk-sentiment backdrop that dominated Wednesday.

A hawkish-sounding ECB account, for instance, may not automatically lift the euro if broader market mood is pulling the other way.

The same likely applies to Fed speeches from officials like Williams and Logan later this week. Their comments could reinforce or contradict the minutes’ hawkish lean. But the market’s response may hinge less on the words themselves than on how surprising those words are relative to what’s already priced in, and on whatever the broader risk mood happens to be that day.

None of this means rate differentials stopped mattering. It means they work best as one piece of a larger picture, not a standalone signal.

The Bottom Line

- A hawkish rate signal doesn’t guarantee currency strength if the market already expected most of it

- The RBNZ’s hike moved the New Zealand dollar partly because a portion of the decision was a genuine surprise, not simply because rates went up

- The US dollar fell despite hawkish Fed minutes, partly because the initial reaction reversed once traders digested the full document, and partly because a fresh geopolitical shock pulled broader sentiment the other way

- Reaction patterns around scheduled releases, like an early spike that fades, are common enough to watch for rather than trade on impulse

- Comparing what a central bank actually says against what was already priced in tends to explain currency moves better than headline tone alone

What to Watch Next

Thursday’s calendar is dense: the ECB’s account of its June meeting, US initial jobless claims, China’s CPI and PPI prints, and Fed speeches from John Williams and Lorie Logan.

Any fresh Iran-related headlines could still overshadow all of it, given how quickly geopolitical developments have reshaped sentiment this week.

If you’re new to reading central bank decisions, it’s easy to assume that a hawkish signal always translates to a stronger currency, but this article shows why that equation breaks down. Premium members can read our lesson:

📖 Market Expectations: Why Good News Can Tank a Currency

Reading this helps you understand why currencies move on the deviation from expectations, how “priced in” dynamics explain the gap between tone and market reaction, and why the same hawkish signal can strengthen one currency while leaving another flat.

And if you’re not a Premium subscriber yet, now’s a good time to sign up.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just what a central bank announced, but how much of that announcement the market had already priced in before it landed.