The minutes of the Federal Reserve’s June 16-17 policy meeting revealed a central bank sharply divided over whether inflation will cool as the Middle East conflict eases or stay elevated as AI-related investment keeps upward pressure on prices.

This marked the first meeting held under new Fed Chairman Kevin Warsh, and while the committee voted unanimously to hold the federal funds rate steady at 3.50%–3.75%, the accompanying discussion pointed to a policy path that is far from settled for the second half of the year.

FOMC June 2026 Meeting Minutes: Key Takeaways

- The FOMC kept its target range unchanged at 3.50%–3.75% in a unanimous 12–0 vote, and the Fed also held the interest rate on reserve balances at 3.65% and the primary credit rate at 3.75%.

- A few participants said there was a case for raising rates at this meeting but ultimately backed holding steady.

- Policymakers are evenly split on the year-end path. Half of the 18 officials who submitted projections favored a rate hike by year-end, while the other half favored holding steady or cutting. Chairman Warsh did not submit a forecast, saying he prefers not to lock the committee into a fixed approach.

- Inflation is running hot and broad-based. Core PCE inflation was estimated at 3.4% in May, with total PCE inflation near 4.1%, both above the Fed’s 2% target.

- AI investment is a genuine two-sided risk. Many participants flagged that sustained demand for AI infrastructure is likely to keep upward pressure on prices for semiconductors, other technology goods, and electricity.

- The labor market looks stable. Unemployment held near 4.3% in May, and payroll growth has kept pace with labor force growth.

- Inflation expectations are becoming a bigger concern. The New York Fed’s survey showed one-year consumer inflation expectations climbing to 3.7% — the highest in nearly three years — while three-year expectations rose to 3.3%, a four-year high.

- The Fed is rethinking its communications. Several participants supported shortening the post-meeting statement and dropping language that had signaled an easing bias.

- Growth remains resilient. Real GDP is tracking near potential, supported by strong consumer spending and continued heavy investment in data centers, high-tech equipment, and software tied to the AI buildout.

Though the Fed kept rates unchanged as expected, the underlying vote masked some disagreement since half of the committee members favored tightening by year-end while the other half leaned towards either holding or cutting. Chairman Warsh did not submit a forecast, saying he prefers not to lock the committee into a fixed approach.

Link to official FOMC Minutes (June 2026)

More hawkish policymakers pointed to elevated inflationary pressures, mainly attributed to lingering tariff effects, supply disruptions tied to the closure of the Strait of Hormuz, and robust AI-related demand. In addition, members warned that persistently elevated expectations could become self-fulfilling.

Some officials noted, however, that AI-driven productivity gains could eventually ease cost pressures. In addition, most participants said the labor market is not currently a source of inflationary pressure.

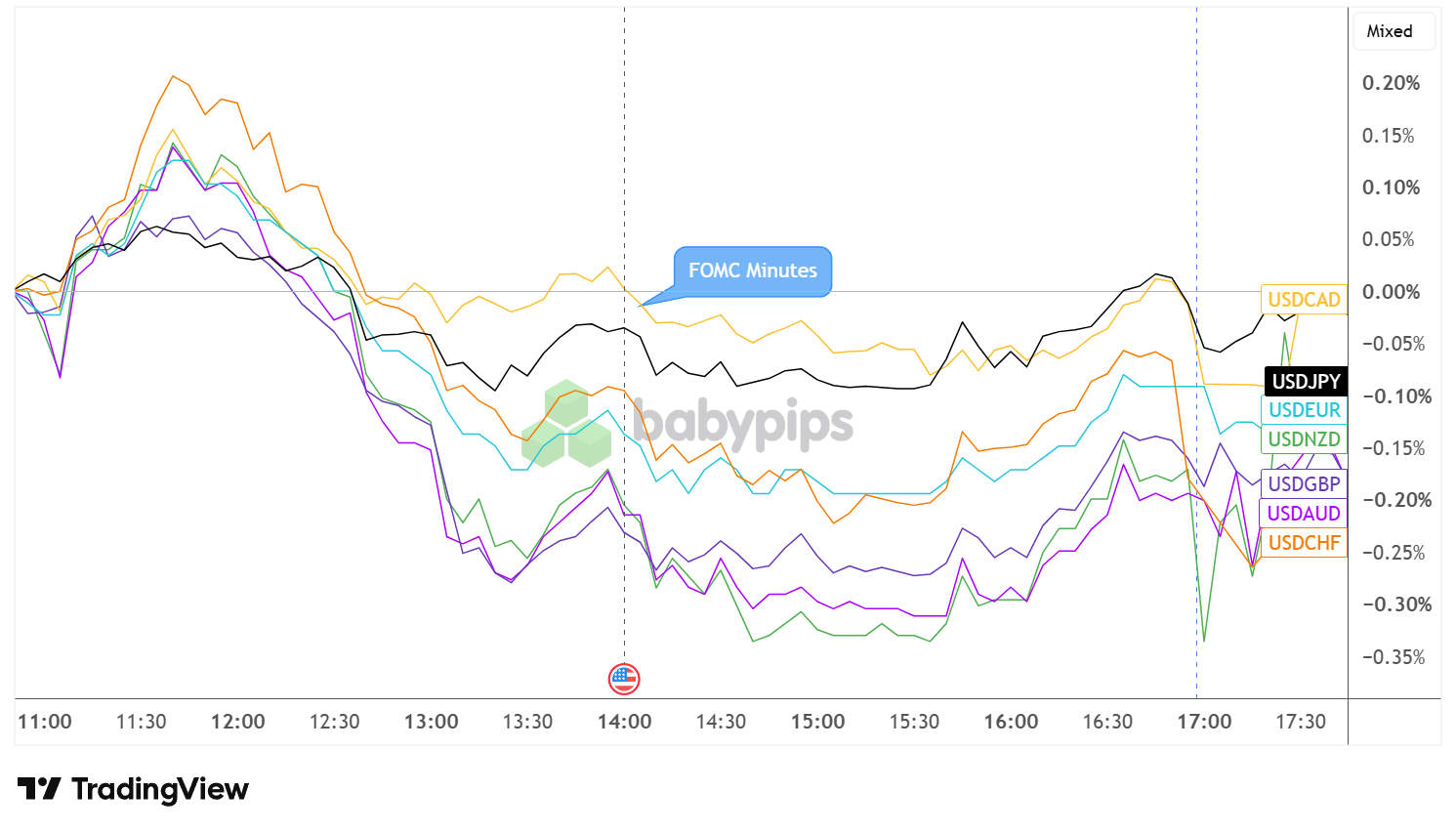

Market Reaction

U.S. Dollar vs. Major Currencies: 5-min

Overlay of USD vs. Major Currencies Chart Faster with TradingView

Once the minutes hit, the dollar extended its slide against most major currencies, with the declines most pronounced against the Australian dollar, New Zealand dollar, and British pound — all falling toward roughly -0.25% to -0.30% relative to the dollar in the two hours that followed.

The U.S. dollar held up comparatively better against the yen and Canadian dollar, which stayed closer to flat, consistent with a market response driven more by shifting rate-hike odds than a broad flight to safety.

Losses were fairly stable through the mid-afternoon before a sharp, brief move towards the end of the session. By then, most pairs had pared back a portion of their post-minutes losses, leaving the dollar’s overall reaction mixed rather than decisively one-directional.

The Fed’s June minutes revealed a committee split down the middle on whether to hike or cut by year-end, and the dollar’s choppy, two-sided reaction shows why the actual decision matters less than what was already priced in. Premium members can read our lesson:

📖 How to Trade Central Bank Decisions Using Market Expectations

Reading this helps you understand what “priced in” really means, how to read market-implied probabilities ahead of a decision, and why a unanimous hold vote can still produce a messy, mixed currency reaction like the one seen after these minutes.

And if you’re not a Premium subscriber yet, now’s a good time to sign up.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just whether the Fed hiked, held, or cut, but how to read the split votes, the dot plot, and the language shifts that move the dollar long before the next decision even lands.