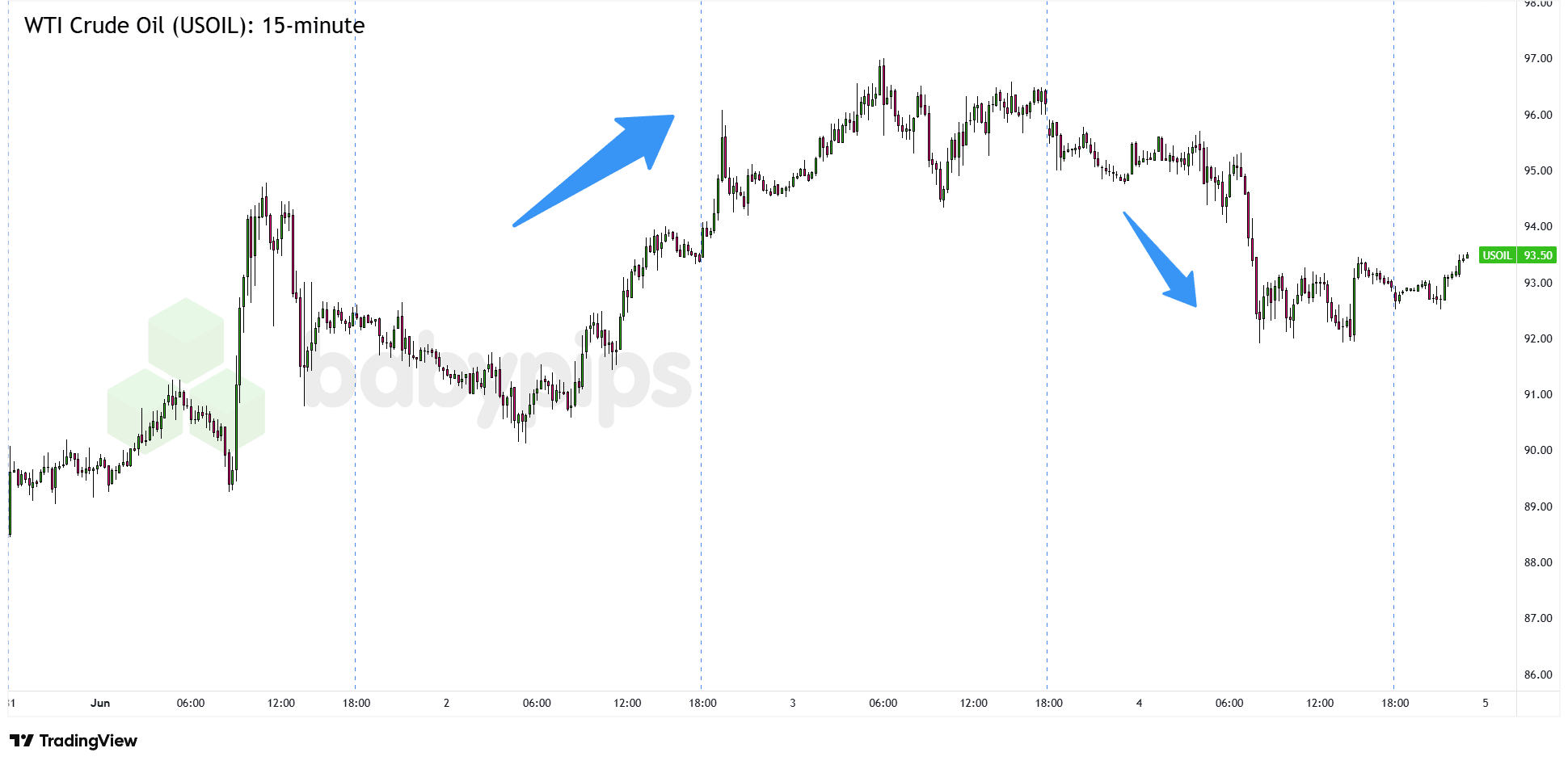

Last week, WTI crude oil was sitting near $88. A few days later, it tapped $97. Then, just like that, it slipped back below $92.

Same barrel of oil. Same physical supply. So what changed?

The market’s price tag on risk.

More specifically, traders were repricing the chance that supply could get disrupted.

That gap between “what’s happening right now” and “what could go wrong next” is called a geopolitical risk premium.

Let’s break down what happened, why the Middle East can still push oil prices around in a hurry, and how this kind of wild ride ripples through the broader financial markets:

The Week, Candle by Candle

The week started quietly enough, with WTI crude hanging around $88. Then traders showed up and kicked the door open.

WTI Crude Oil (USOIL) 4-hour –Chart Faster with TradingView

On Monday, Iran threatened to fully close the Strait of Hormuz – the narrow waterway that carries roughly 20% of the world’s seaborne oil – while reports also pointed to missile strikes on a U.S. air base in Kuwait. Just like that, traders went from calm to “not today,” and WTI jumped nearly 5% in a single session to close above $92.

The move kept going on Tuesday and Wednesday. Fresh Iranian strikes on Gulf facilities, stronger U.S. economic data keeping the higher-for-longer Fed story alive, and lingering worries over the Strait of Hormuz pushed oil to a weekly high near $97.Then, the tides changed on Thursday. The Trump administration announced a ceasefire between Israel and Lebanon, while Trump also suggested a U.S.-Iran deal could come together over the weekend. That was enough to take some fear out of the market, and oil dropped sharply to close near $91.20.

By Friday morning, WTI was trading around $93. Still elevated, sure, but nowhere near the panic highs.

Take note that no oil field changed production. No tanker was seized. The physical market barely budged.

Most of the move came from traders pricing in uncertainty, then quickly repricing it when the headlines cooled down.

Why This Matters Beyond the Oil Market

Oil’s relevance for forex traders isn’t just about energy stocks or commodity CFDs.

The transmission runs straight through to currency pairs, and it works differently depending on which side of the trade a country sits on.

The Oil Importers (A Tax on the Currency)

Japan imports roughly 90% of its energy needs. India imports around 85% of its oil. When prices spike, both countries must spend more U.S. dollars to pay for the same volume of fuel. That increased dollar demand puts direct selling pressure on their local currencies.

This week, USD/JPY approached the 160 level that prompted Japanese intervention warnings in 2024, and Japan’s Finance Minister deployed a verbal warning about currency management. The Indian rupee, meanwhile, has been Asia’s worst-performing major currency in 2026, with analysts citing the enlarged import bill as a key structural drag.

The Euro Area sits in a similar position. Europe imports most of its energy. A sustained oil rally narrows the current account and compounds the ECB’s inflation management problem — both headwinds for the euro.

The Oil Exporters (The Petrocurrencies)

Canada sends a significant portion of its oil production to global markets, making the Canadian dollar a petrocurrency: one whose value tends to move with crude prices. When WTI rallies, USD/CAD tends to fall. When oil drops on ceasefire news, USD/CAD tends to rise.

Thursday’s pullback in crude toward $91.20 was visible in USD/CAD, which closed near 1.3908.

Promoted: Is Your Small Account Holding Your Strategy Back?

Trading $100 isn’t the same as trading $100k. Emotional discipline & trading flexibility is easier when you have the right backing. FTMO is a global prop firm with a 4.8★ rating on 40K+ reviews, serving traders since 2015! No time limits. Free trials. Up to $200K in Demo Capital.

Start a free trial with FTMO!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

The Dollar’s Own Complication

The U.S. dollar doesn’t have a clean relationship with oil. It runs on two competing channels simultaneously.

Higher oil can lift U.S. inflation expectations, which can push Fed hike expectations higher and support the Greenback through wider rate differentials. That was in play this week, with markets raising the odds of a 25bp Fed hike by year-end to around 85%. DXY also hit 99.54 on Thursday, its highest level since April.

But the dollar is also getting safe haven support from the geopolitical mess. When peace headlines hit on Thursday after the Lebanon ceasefire announcement, some of that safety premium faded, even though rate expectations stayed elevated.

Both channels ran simultaneously this week. The result was a dollar that was choppy rather than directional — pulled in opposite directions, pending a bigger fundamental resolution.

Quick Takeaways

- A geopolitical risk premium is the extra cost baked into an asset’s price to reflect the possibility of a supply disruption — not an actual one.

- Oil-importer currencies (JPY, EUR, INR) tend to weaken when crude rises; oil-exporter currencies (CAD) tend to strengthen.

- The dollar’s reaction to oil is two-sided: rate expectations pull one way, safe-haven flows pull the other.

- Risk premiums unwind faster than they build. Watch sustained daily closes, not intraday prints, to confirm whether a move is structural or a headline fade.

What to Watch Now

- Today’s NFP release (8:30 AM ET) matters for oil indirectly. A soft labor print would ease inflation concerns, reduce rate-hike probability, and soften the dollar — potentially allowing commodity-linked currencies like CAD to recover ground.

- The bigger variable remains the US-Iran deal. Trump suggested something could happen this weekend. If a formal agreement materializes, the Hormuz risk premium — currently still priced into that $93 handle — could unwind quickly, pulling WTI toward $84–$87 and relieving pressure on oil-importer currencies in the process. A deal collapse does the opposite.

This article breaks down how a geopolitical risk premium in oil prices rippled through currency markets, and the forces behind that transmission may not be familiar to all readers. Premium members can read our lesson:

📖 Geopolitical Risk, Trade Policy, and Safe Haven Flows

Reading this helps you understand how geopolitical events move currencies, what drives safe haven flows, and why oil-importer and oil-exporter currencies respond in opposite directions when supply disruption fears spike.

And if you’re not a Premium subscriber yet, now’s a good time to sign up.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just what a geopolitical risk premium is, but how it flows through commodity prices into the currencies you’re actually trading.