The Trump administration announced that Israel and Lebanon agreed to implement a ceasefire and establish security zones in southern Lebanon, contingent on a complete halt to Hezbollah fire and evacuation of its operatives from the South Litani sector. It was the second such ceasefire agreement in as many months, with the first having failed to hold. President Trump suggested a deal with Iran could materialize over the weekend.

The U.S. House of Representatives passed a war powers resolution to block further U.S. strikes on Iran, though the White House dismissed it and analysts broadly characterized the vote as largely symbolic. Reports indicated Trump told aides privately he would not resume all-out war unless American troops were killed, a threshold markets may have interpreted as confirming the administration is managing conflict rather than seeking wider escalation.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Australia Balance of Trade for April 2026: 1.79B (-1.3B forecast; -1.84B previous)

- Swiss CPI Growth Rate for May 2026: 0.6% y/y (0.8% y/y forecast; 0.6% y/y previous); 0.2% m/m (0.3% m/m forecast; 0.3% m/m previous)

- Swiss Unemployment Rate for May 2026: 3.0% (2.9% forecast; 3.0% previous)

- U.K. New Car Sales for May 2026: 7.1% y/y (3.7% y/y forecast; 24.0% y/y previous)

- U.K. S&P Global Construction PMI for May 2026: 38.2 (40.3 forecast; 39.7 previous)

- Euro area Retail Sales for April 2026: 1.0% y/y (0.7% y/y forecast; 1.2% y/y previous); -0.4% m/m (-0.6% m/m forecast; -0.1% m/m previous)

- U.S. Challenger Job Cuts for May 2026: 97.01k (90.0k forecast; 83.39k previous)

- U.S. Initial Jobless Claims for May 30, 2026: 225.0k (216.0k forecast; 215.0k previous)

- U.S. Nonfarm Productivity Final for Q1 2026: 0.3% q/q (0.8% q/q forecast; 1.8% q/q previous)

- U.S. Unit Labor Costs for Q1 2026: 1.8% (2.3% forecast; 4.4% previous)

- EIA Natural Gas Stocks Change for May 29, 2026: 95.0Bcf (92.0Bcf previous)

Promotion: TradeZella is the top journaling app in the industry, and its new AI trading partner feature can break down and analyze your trades & build a game plan, freeing up time and energy to focus on the next moves!

Start Your Trading Journey with Tradezella & use code “PIPS20” for 20% off your first purchase!

Disclosure: To help support our free daily content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

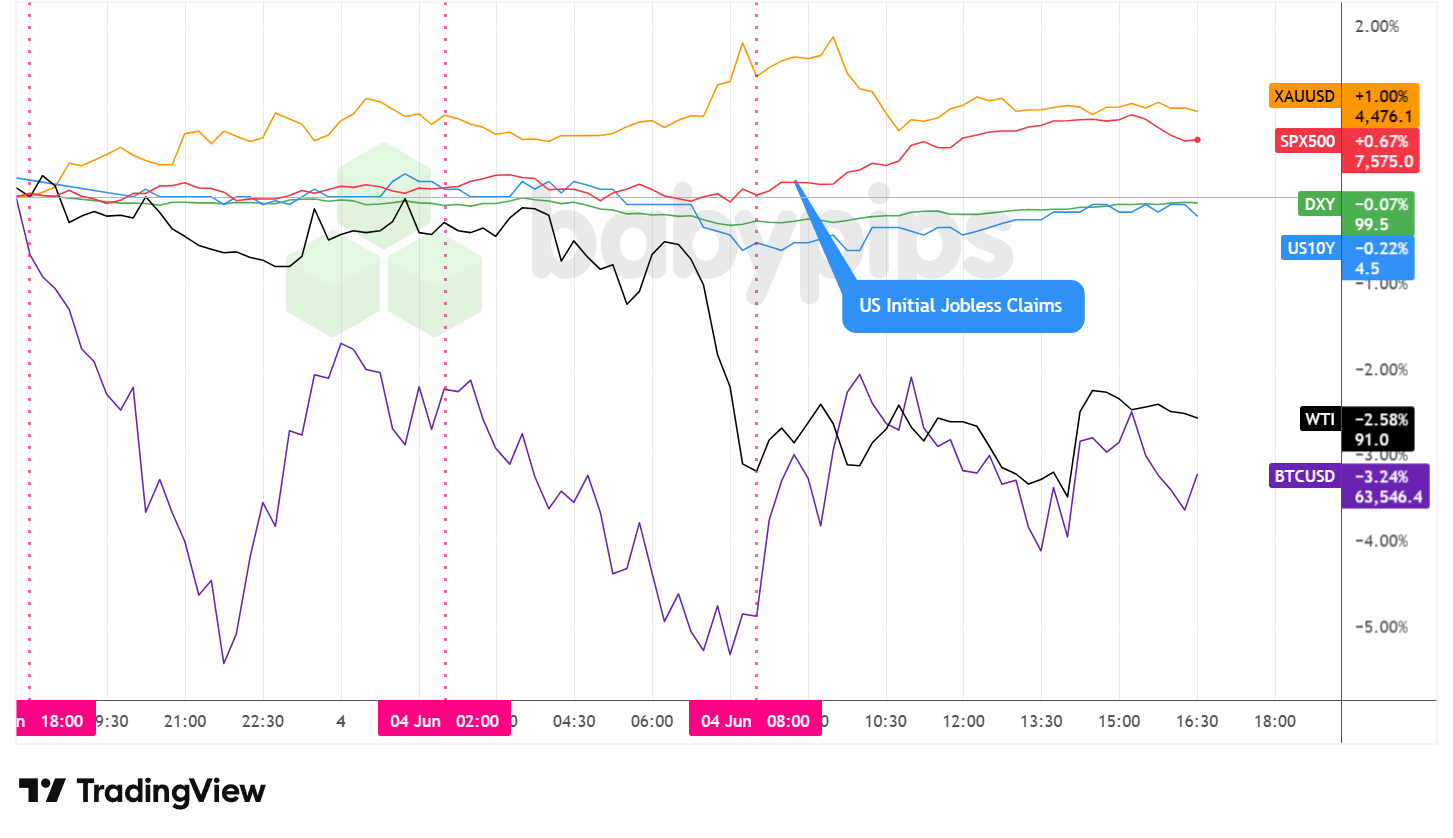

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Thursday’s broad market session featured a clear bifurcation in asset performance: equities and gold rallied meaningfully while crude oil and Bitcoin both declined, with Treasury yields nudging lower as well. The dominant narrative remained the evolving geopolitical backdrop in the Middle East, alongside a pre-positioning dynamic ahead of Friday’s critical U.S. employment situation report.

Gold was the standout performer among the assets tracked, climbing approximately 1.10% to close near $4,480. The precious metal climbed steadily from the Asian session through the early European hours before reaching an intraday peak around the London open. Following a brief pullback, it found support and settled into a relatively narrow consolidation range through the U.S. afternoon. The gains likely reflected a combination of safe-haven demand tied to ongoing Middle East uncertainty and a softer dollar environment through much of the day.

The S&P 500 gained approximately 0.74% to close near 7,584. The index traded largely sideways in the Asian and London sessions, but saw a sharp acceleration higher following the U.S. open, advancing in a near-uninterrupted grind through midday before easing slightly from session highs. The Dow Jones Industrial Average reached an all-time high during the session. The advance appeared driven by dip buying following weakness related to Broadcom’s disappointing outlook, with analysts noting that enthusiasm for AI infrastructure spending and signs of a resilient economy underpinned broad market optimism. Small-cap stocks also outperformed, with a measure of smaller companies climbing around 1.7%.

WTI crude oil declined approximately to close near $91.20 per barrel, extending losses that began during the London session. The selloff appeared to correlate with optimism over a potential U.S.-Iran deal following Trump’s weekend timeline suggestion, as markets may have priced in reduced near-term supply risk. The intraday chart shows oil’s most aggressive leg lower occurred around the London open, with the bulk of the move completed before the U.S. open, after which price stabilized and traded in a choppy range.

Bitcoin fell approximately 2.68% to close near $63,480. The cryptocurrency sold off sharply through the Asian session before reaching a daily trough near $62,100 around the U.S. open, after which it recovered to trade back above $63,000 for the remainder of the session. The move lower appeared to track broader risk-off sentiment from early in the session, with the partial recovery possibly coinciding with the improved equity tone following the Wall Street open.

The U.S. 10-year Treasury yield declined approximately 0.18% to close near 4.50%. Yields drifted lower from early in the session, with the most notable leg down occurring during the European morning hours before partially stabilizing into the U.S. afternoon. The softer yield environment aligned with the day’s mix of weaker-than-expected U.S. labor market data, including initial jobless claims and Challenger job cuts both coming in above forecasts, and a final Q1 nonfarm productivity reading that missed estimates.

Promoted: Is Your Small Account Holding Your Strategy Back?

Trading $100 isn’t the same as trading $100k. Emotional discipline & trading flexibility is easier when you have the right backing. FTMO is a global prop firm with a 4.8★ rating on 40K+ reviews, serving traders since 2015! No time limits. Free trials. Up to $200K in Demo Capital.

Start a free trial with FTMO!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

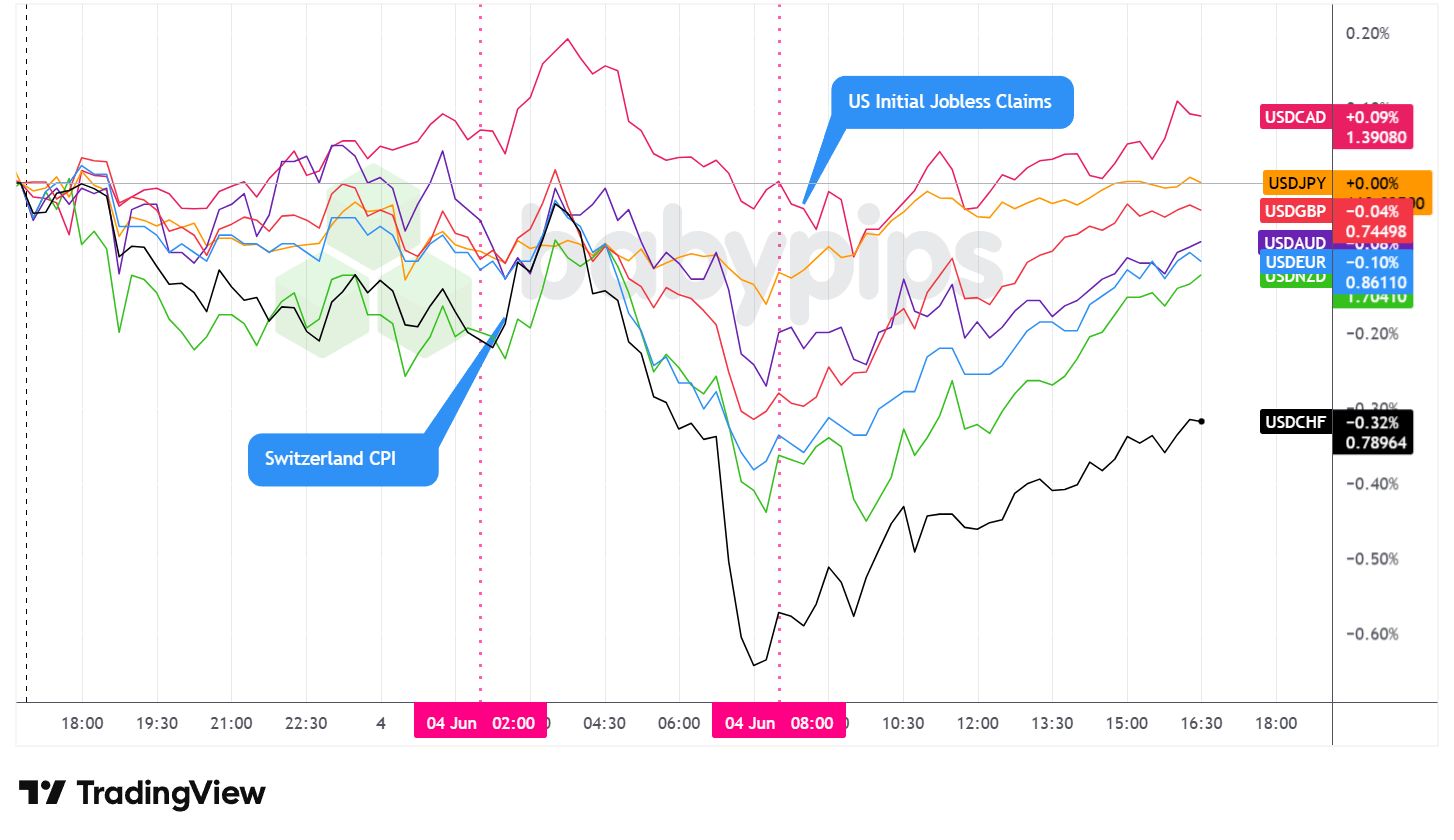

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar closed Thursday as a net underperformer against most major currencies, though the session featured pronounced intraday swings before settling into a broadly bearish closing picture. Only against the British pound did the dollar manage a slight net gain on the day.

During the Asian session, the dollar traded choppy and mostly sideways with a net bearish bias. The moves were relatively contained across major pairs, with no significant regional catalyst driving clear directional momentum.

The London session brought a more directional shift. The dollar initially rebounded against the major currencies following the European open, possibly reflecting positioning adjustments ahead of the busy data calendar and central bank commentary. That rebound proved short-lived, however, and the dollar turned lower against the majors with a bearish bias heading into the U.S. session. The Swiss franc’s strength was particularly pronounced around this period, with USDCHF falling sharply to reach its intraday trough near the U.S. open. Swiss inflation coming in slightly below forecast for May may have contributed to some early CHF demand as a safe-haven flow, though the broader softening of the dollar through this window suggests geopolitical and risk-sentiment dynamics were also at play.

During the U.S. session, the dollar rebounded against all of the major currencies. The recovery was broad-based but varied in magnitude across pairs. The USDCHF rebound was the most visually prominent on the overlay chart, recovering a significant portion of its London session losses. Despite the afternoon recovery, the dollar could not fully retrace its earlier declines, and the closing picture remained net bearish on the day.

Promotion: When Geopolitics and NFP Jitters Collide, Are You Reacting or Executing?

Between sudden safe-haven flows into the Swissy, oil supply speculation, and the market holding its breath for Friday’s U.S. employment data, Thursday’s session tested every trader’s discipline. When the news cycle creates choppy, headline-driven price action, even the best technical setups can fall victim to emotional execution.

In Positive Trading Psychology, renowned market psychologist Brett Steenbarger reveals that the secret to navigating these uncertain, bifurcated markets isn’t “fixing” your emotional flaws—it’s doubling down on your innate character strengths. Learn how to stay clinical and protect your capital while the rest of the market reacts blindly to the next news drop.

Learn more about “Positive Trading Psychology: Turning personal strengths into trading strengths” on Amazon!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- Japan Overtime Pay for April 2026 at 11:30 pm GMT

- Japan Household Spending for April 2026 at 11:30 pm GMT

- Japan Average Cash Earnings for April 2026 at 11:30 pm GMT

- Australia RBA Hauser Speech at 4:30 am GMT

- Japan Leading Economic Index Prel for April 2026 at 5:00 am GMT

- U.K. Halifax House Price Index for May 2026 at 6:00 am GMT

- Swiss Foreign Exchange Reserves for May 2026 at 7:00 am GMT

- Euro area Employment Change Final for March 31, 2026 at 9:00 am GMT

- Euro area GDP Growth Rate 3rd Est for March 31, 2026 at 9:00 am GMT

- U.K. BBA Mortgage Rate for May 2026 at 9:00 am GMT

- Canada Employment Situation Update for May 2026 at 12:30 pm GMT

- U.S. Employment Situation Update for May 2026 at 12:30 pm GMT

- Bank of England Dhingra Speech at 1:40 pm GMT

- Canada Ivey PMI s.a for May 2026 at 2:00 pm GMT

- Bank of England Gov Bailey Speech at 6:00 pm GMT

- U.S. Consumer Credit Change for April 2026 at 7:00 pm GMT

Friday’s calendar is headlined by the simultaneous release of the U.S. and Canadian employment situation updates at 12:30 pm GMT. The U.S. payrolls report carries elevated market importance given the week’s softer labour market signals, including jobless claims above forecast, higher-than-expected Challenger job cuts, and a disappointing Q1 productivity revision.

Analysts have flagged the need for a “Goldilocks” outcome to sustain equity momentum, meaning growth solid enough to support earnings but not so strong as to revive rate hike concerns. Any meaningful deviation from expectations could generate sharp moves across equities, Treasuries, and the dollar. The Fed’s Daly speech Thursday evening could also offer an early read on how policymakers are framing the labour market picture ahead of Friday’s data.

Stay frosty out there, forex friends!