After seven consecutive weeks of easing their net bearish bias on the Greenback, large speculators became more bearish on the Greenback again since the value of net short positions on the Greenback rose from $643 million to $3.15 billion during the week ending on November 21, according to calculations done by Reuters.

And the latest Commitments of Traders (COT) forex positioning report from the CFTC reveals that the Greenback lost ground to the euro, the yen, and the pound while continuing to take ground from the others.

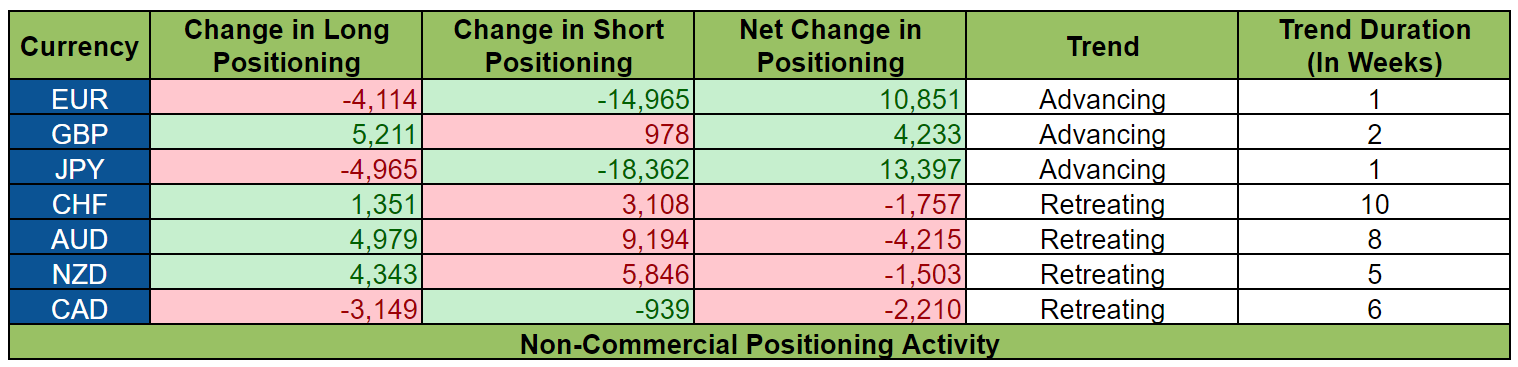

Oh, please keep in mind that the numbers below show the net positioning of non-commercial forex traders against the U.S. dollar.

And if you’re feeling overwhelmed by all these figures, you might need to review our School of Pipsology lesson on How to Gauge Market Sentiment Using the COT Report in order to learn how to pinpoint potential forex market reversals.

And here is how positioning activity played out during the week ending on November 21, 2017.

Positioning wasn’t very favorable to the Greenback during the week ending on November 21. Even so, positioning wasn’t broadly against the Greenback since the Greenback lost ground to the euro, the yen, and the pound while taking ground from its other forex rivals. As such, positioning activity was likely driven by catalysts for the other currencies, rather than the Greenback.

With that said, the Greenback was likely vulnerable because of Fed Chair Yellen’s comment that she is “very uncertain” on whether or not inflation will pick up the pace within the next year or two.

And this is compounded by the fact that the October U.S. CPI report was released less than a week ago and that showed that CPI rose by 0.1% month-on-month, which is within expectations but slower than September’s 0.5% rise. The year-on-year reading also showed a slowdown from +2.2% to +2.0%.

Other than that, worries related to the tax reform bill may have dented sentiment on the Greenback a bit since the House of Representatives successfully passed their version of the bill, but the U.S. Senate has yet to do so and there are conflicting provisions between the two versions, which increases the risk for a possible delay.

Anyhow, as noted earlier, positioning activity was a bit mixed, so catalysts for the other currencies likely affected positioning activity as well. And here are the major events, reports, and other catalysts for the other currencies:

EUR

Positioning activity was favorable for the euro because 14,965 short contracts on the euro got culled, which were able to more than offset the loss of 4,114 long contracts on the euro.

Both euro bulls and euro bears substantially increased their respective positions during the previous week. And the reduction in both euro longs and euro shorts during the week ending on November 21 likely shows euro bulls taking some profits off the table and euro bears getting spooked by ECB President Draghi’s November 17 speech.

You see, Draghi said in his speech that “the latest data and surveys [are] pointing to unabated growth momentum in the period ahead.”

Moreover, Draghi expressed that the ECB is confident “that the recovery is robust and that this momentum will continue going forward” because “the drivers of growth are increasingly endogenous rather than exogenous.”

Given the expected strong growth in the Euro Zone, Draghi said that:

“Low-for-long interest rates might contribute to a build-up of financial risks, and this has to be carefully monitored.”

That’s a pretty hawkish statement since Draghi is basically saying that the ECB has a tightening bias on monetary policy, particularly interest rates. However, Draghi was quick to add that:

“At present we do not see systemic risks emerging at the euro area level.”

So, the ECB will need to tighten monetary policy to avoid financial risks, but such risks haven’t emerged yet, which is why the ECB is not ready to move too much.

Even so, the cat’s out of the bag and it’s now clear that the ECB has a tightening bias, which seems to go against its most recent forward guidance that it’s neutral on interest rates while still having an easing on its QE program. And that’s likely far more euro bears decided to call it quits.

Other than that, it’s also possible that positioning activity shows some euro bulls taking their profits and running away because of news that negotiations to form a coalition government in Germany apparently failed and that the Social Democratic Party (SPD) didn’t want to cooperate.

Of course, we now know that SPD leader Martin Schulz relented and said that his party will cooperate with Merkel, which renewed hopes that a coalition government in Germany will finally be formed, which apparently boosted demand for the euro. However, the most recent COT report does not yet reflect that.

GBP

Bearish bias on the pound eased even further, so much so that net positioning on the pound is now within licking distance of switching to net bullish.

And looking at positioning activity, the improving sentiment on the pound was due to another wave fresh pound longs.

Pound bulls were likely enticed to jump in by the U.K.’s October retail sales report since that showed that retail sales volume in the U.K. grew by 0.3% in October, which is a tick stronger than the consensus for a 0.2% increase.

Other than that, easing Brexit-related jitters and/or political uncertainty may have convinced pound bulls to jump in since debates on the Brexit Bill ended favorably for Theresa May’s government. Not only that, the rumors about a no-confidence challenge to Theresa May didn’t materialize.

The pound did see a small increase in pound shorts, though. And that was a likely a reaction to E.U. top Brexit negotiator Michel Barnier’s comments since he warned about the possible negative consequences of a hard Brexit, which includes U.K. banks will losing access to the E.U. single market’s “500 million consumers and 22 million businesses.”

JPY

The yen took a substantial chunk of ground from the Greenback. However, a closer look at positioning activity shows that both yen bulls and yen bears were slashing their respective positions. However, the reduction of 18,362 short contracts on the yen was significantly more than the loss of 4,965 long contracts on the yen, which is why net change in positioning was substantially favorable for the yen.

Positioning activity on the yen likely shows profit-taking by yen bulls and yen bears getting scared off because of falling bond yields and the prevalence of risk aversion at the time.

CHF

Large players became even more bearish on the Swissy, which marks the tenth consecutive week of deteriorating sentiment on the Swissy.

However, positioning activity shows that Swissy bulls and Swissy bears reinforced their respective positions. It just so happens that more short contracts on the Swissy were opened compared to fresh longs.

The increase in Swissy longs was likely due to the risk-off vibes at the time. As for the increase in Swissy shorts, that was likely due to the Swiss government’s statement that the Swissy is still “highly valued”.

And since the Swissy was showing strength at the time, partly because of the risk-on vibes and partly because the Swissy has been tracking the euro higher, it’s also likely that the increase in Swissy shorts show speculative bets on the expectation that the SNB will step in to try and weaken the Swissy.

AUD

Net bullish bias on the Aussie eased some more, marking the eighth consecutive week of easing bullish bias on the Aussie. Both Aussie bulls and Aussie bears were ramping up their positions, though.

The increase in Aussie longs was likely due to RBA Governor Lowe’s speech since he basically spelled out that the RBA has a long-term hiking bias when he said that:

“If the economy continues to improve as expected, it is more likely that the next move in interest rates will be up, rather than down.”

Low did stress that:

“There is not a strong case for a near-term adjustment in monetary policy”

Other than that, the influx of Aussie longs may reflect interest rate differentials in favor of the higher-yielding Aussie since Fed Chair Yellen’s comment that she is “very uncertain” about the pick-up in inflation caused odds for a follow-up March 2018 rate hike to drop.

As for the increase in Aussie shorts, that was likely due to the risk-off vibes at the time and disappointment over Australia’s wage price index and latest jobs report.

NZD

Positioning activity on the Kiwi was quite similar to the Aussie in that Kiwi bulls and Kiwi bears both added to their bets, with bears having the advantage.

There were no major positive catalysts for the Kiwi at the time, so the fresh Kiwi longs likely reflects interest rate differentials in favor of the higher-yielding Kiwi since Fed Chair Yellen’s comment that she is “very uncertain” about the pick-up in inflation caused odds for a follow-up March 2018 rate hike to drop.

The increase in Kiwi shorts, meanwhile, was likely due to the prevalence of risk aversion at the time, as well as disappointment over the GDT price index slumping by 3.5% in the latest dairy auction.

CAD

Like in the previous week, both Loonie bulls and Loonie bears were trimming their respective positions, with more Loonie longs getting culled, so the Loonie retreated against the Greenback for the sixth consecutive week.

The reduction in Loonie longs, which overwhelmed the small decrease in Loonie shorts, likely reflects worry related to news that the Keystone pipeline suffered a leak in South Dakota, which forced TransCanada to shut down the pipeline, which isn’t good for the Canadian economy.

Aside from that, Loonie longs may have been spooked by Canada’s October CPI report since headline CPI only ticked higher by 0.1% month-on-month, which is a tick slower compared to the previous month’s 0.2% increase.

Year-on-year, this translates to a 1.4% increase, which is slower than the previous month’s 1.6% increase and puts an end to three straight months of ever stronger annual readings.

Got any other conclusions you can draw from this latest COT Report? Feel free to share your thoughts in the comments section or if you’re looking for further discussion, community member ForExchange has a lively thread called Trading based on Market Sentiment in the forums awaiting your participation.