According to calculations done by Reuters, large speculators eased their bearish bias on the Greenback for the seventh consecutive week. In fact, large players almost became net bullish on the Greenback after they reduced the value of their net short positions on USD from $1.92 billion to $643 million during the week ending on November 14.

And the latest Commitments of Traders (COT) forex positioning report from the CFTC reveals that positioning activity still broadly favors the Greenback but the pound was able to take back some lost ground.

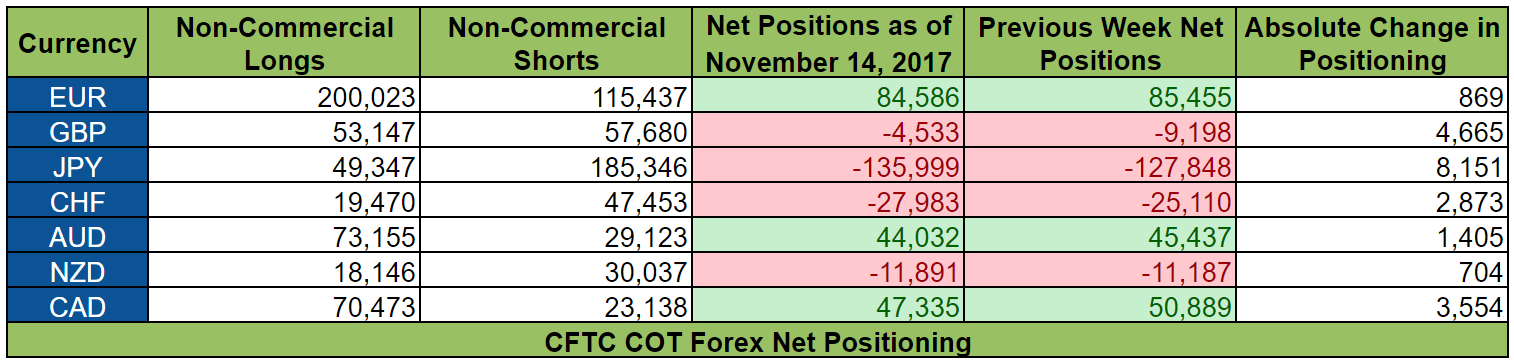

Oh, please keep in mind that the numbers below show the net positioning of non-commercial forex traders against the U.S. dollar.

And if you’re feeling overwhelmed by all these figures, you might need to review our School of Pipsology lesson on How to Gauge Market Sentiment Using the COT Report in order to learn how to pinpoint potential forex market reversals.

And here is how positioning activity played out during the week ending on November 14, 2017.

Sentiment on the Greenback improved further during the week ending on November 14, so much so that net positioning on the Greenback almost became net bullish.

And as has been the case during the past few weeks, sentiment on the Greenback improved broadly at the expense of the Greenback’s forex rivals.

Interestingly enough, the most recent COT report already reflects how large players reacted to the U.S. Senate’s version of the tax reform bill.

And apparently, large players were not fazed by that, even though the Senate’s version is different when compared to the House’s version of the tax plan, particularly with regard to the implementation date since the Senate wants to slash corporate tax rates in 2019, which is a year later compared to the House’s version.

More than that, it’s possible that the improving sentiment on the Greenback shows that large players are expecting the tax reform bill to successfully push through despite the differences.

Anyhow, here are the major events, reports, and other catalysts for the other currencies:

EUR

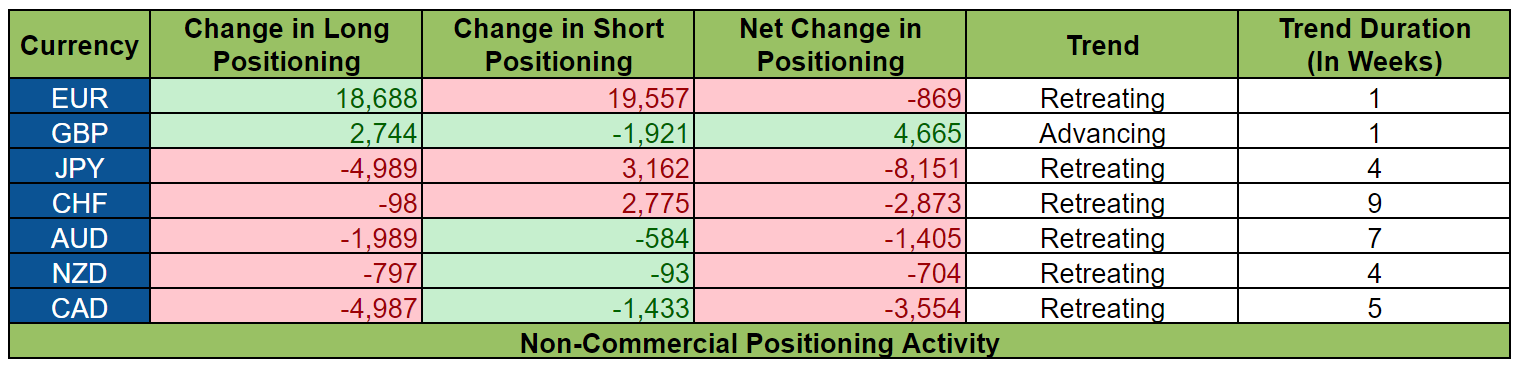

Net change in positioning on the euro was only minimal. However a closer look at positioning activity shows that euro bulls and euro bears both significantly boosted their respective positions.

The large buildup in euro longs was likely due to The European Commission’s Autumn 2017 Economic Forecast since the growth forecast for 2017 was upgraded from 1.7% to 2.2% while the growth forecast for 2018 was upgraded from 1.8% to 2.1%.

And while the 2017 forecast for the Euro Zone’s HICP was from 1.6% to 1.5%, 2018’s inflation forecast was upgraded from 1.3% to 1.4%. And HICP is expected to accelerate to 1.6% in 2019.

As for the rather substantial increase in euro shorts, there’s no clear reason for that. However, it’s possible that some large players were none too happy with the ECB’s latest economic bulletin since the ECB noted that while risks to the Euro Zone economy were balanced, the downside risks do exist and they “relate primarily to global factors and developments in foreign exchange markets.”

The ECB also implied that the euro was overbought when it noted that the euro’s recent depreciation against the Greenback and the pound were “largely offset by other developments, with the euro appreciating vis-à-vis most other major currencies.”

The European Commission’s Autumn 2017 Economic Forecast also shared this sentiment since it listed “a stronger appreciation of the euro” as one of the downside risks to its forecasts.

GBP

Bearish bias on pound eased a bit as pound bulls reinforced their positions while pound bears decided to pull back from theirs.

Pound bulls were likely enticed to add to their bets because of net positive U.K. data. To be more specific, total industrial production grew by 0.7% month-on-month in September, which is stronger than the expected 0.3% growth. Year-on-year, industrial production in the U.K. accelerated for the fourth consecutive, increasing by 2.5% in September.

Also, the U.K.’s trade deficit narrowed from £3.46 billion to £2.75 billion in September.

And while the U.K.’s October CPI only increased by 3.0% year-on-year, which is below the BOE’s +3.2% forecast, October’s reading still marks the ninth consecutive month that CPI has been exceeding the BOE’s inflation target of +2.0%.

As for the reduction in pound shorts, profit-taking by pound bears is a possibility after a rumored no-confidence vote against Theresa May failed to materialize.

JPY

Positioning activity on the yen was rather bearish since yen bulls trimmed their positions while yen bears added even more to theirs. And this was likely due to the rise in global bond yields at the time.

Also, it also likely that positioning activity reflects ongoing positioning in favor of the Greenback and at the expense of the yen due to the monetary policy divergence between the Fed and the BOJ, given that the Fed is expected to hike again in December.

CHF

The Swissy was pushed even deeper into bearish territory, which marks the ninth consecutive week of worsening sentiment on the Swissy. And as usual, the monetary policy divergence between the Fed and the SNB may have been the driver behind positioning activity since risk aversion was actually the prevailing sentiment during the week ending on November 14.

AUD

Net bullish bias on the Aussie eased for the seventh consecutive week, thanks to the unwinding of 1,989 long contracts on the Aussie. Aussie bears were shedding some of positions as well, though.

And positioning activity on the Aussie likely reflects bulls calling it quits because of falling gold prices at the time.

Large players favored the Greenback over the Aussie even more during the week ending on November 7, which marks the sixth week of deteriorating sentiment on the Aussie.

Aussie bulls and Aussie bears were paring their respective positions, though. It just so happens that more Aussie bulls were calling it quits.

Also, bulls may have been disappointed to find out that the RBA downgraded its inflation forecasts in its latest Statement on Monetary Policy, which also likely put monetary policy divergence in play since lower inflation forecasts mean that the RBA is even less likely to hike. In contrast the Fed is expected to hike this December, with more hikes in the cards next year.

As for the reduction in Aussie shorts, profit-taking by Aussie bears because of falling gold prices and the RBA’s Statement on Monetary Policy is a possibility.

NZD

Net positioning change on the Kiwi was only minimal. And the same can be said of positioning activity.

Interestingly enough, positioning activity already reflects the November RBNZ Statement. Even so, positioning activity was only minimal, which implies that large speculators were not sure on what to think about the latest RBNZ statement.

And this seemingly confused reaction to the RBNZ statement was likely due to the fact that the RBNZ’s surprisingly hawkish forecast of 2 rate hikes in 3 years is based on the assumption that the Kiwi remains at current low levels.

CAD

Both Loonie bulls and Loonie bears were slashing their positons. However, net bullish bias on the Loonie deteriorated further because more Loonie longs got culled.

Positioning activity likely reflects Loonie bulls getting spooked and Loonie bears unwinding their shorts because of the rather hard drop in oil prices on November 14.

Got any other conclusions you can draw from this latest COT Report? Feel free to share your thoughts in the comments section or if you’re looking for further discussion, community member ForExchange has a lively thread called Trading based on Market Sentiment in the forums awaiting your participation.