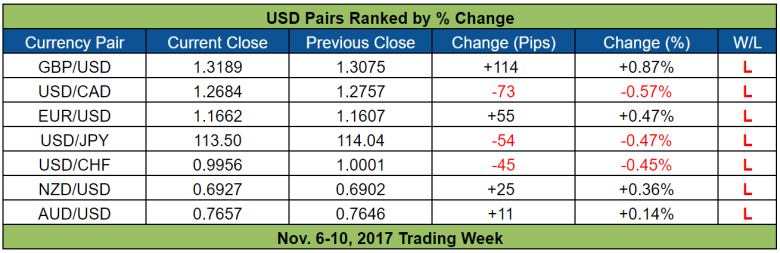

The forex trading week has come and gone, so it’s time to take a look at how the major currencies performed and what drove price action.

Like in the previous week, none of the top 10 movers were able to reach the 1% mark for weekly % change, so volatility was relatively tight once again and longer-term traders probably had another tough week.

With that said, half of the top 10 movers are GBP pairs, with the pound winning out in every one of ’em, so pound strength was clearly a theme this week. Another theme was Greenback weakness since USD was the worst-performing currency of the week and half of the top 10 movers are Greenback pairs.

So, what drove forex price action this week? And what about the other currencies? How drove their price action this week? Time to find out!

But before that, here’s this week’s scoreboard.

And if you only want to find out what happened to a specific currency, then you can just skip to that currency by clicking on it below.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

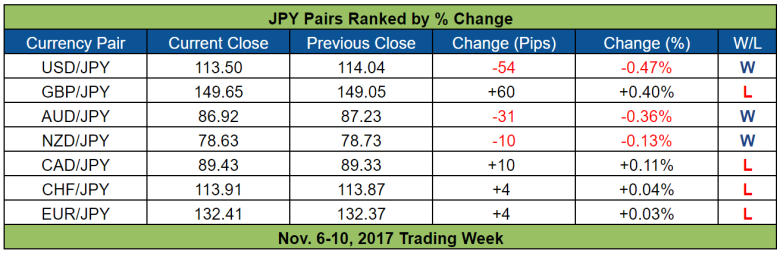

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The U.S. Dollar

The Greenback was the main loser this week. And while price action on the Greenback looks kinda messy, it does get better if we simply remove GBP/USD from the overlay of USD pairs.

As you can see above, the Greenback was drifting lower before finally finding support on Thursday. And practically all market analysts blamed the Greenback’s weakness on worries related to the much-awaited Republican Tax Bill.

Interestingly enough, the Greenback actually found support when the U.S. Senate’s version of the tax plan was revealed late on Thursday, even though the Senate’s version is a bit different compared to the tax plan released by the House last week.

As for details, Bloomberg has a quick write-up comparing the two versions, so read it here, if you’re interested.

However, the biggest cause of concern for most analysts is that the House wants to slash corporate taxes from 35% to 20% starting next year while the Senate wants the same tax cut but starting on January 2019, which is a full year away and stoked fears of a possible delay to the bill.

Anyhow, the Greenback’s reaction to the actual announcement heavily implies that the Greenback’s slide really was driven by worries related to the tax bill and that market players were using the release of the actual tax plan to cover their shorts.

In other words, a “sell the rumor, buy the news” scenario played out.

And it certainly helped (Greenback bears) that rumors about the tax plan began circulating as early as Tuesday.

For example, the Washington Post ran a story on Tuesday that cited “four people familiar with a draft of the legislation” as saying that the U.S. Senate’s version of the tax plan will be different and that one major difference is that corporate tax cuts won’t be implemented until 2019. And as mentioned earlier, the Senate’s version was different, so that Washington Post report turned out to be accurate.

Also worth noting is that the tax bill was leaked hours before the actual, official announcement, so, yeah, a “sell the rumor, buy the news” scenario apparently played out.

Anyhow, this tax bill drama is not over yet since the House will be voting on the tax bill next week. The Senate doesn’t have a clear timetable, but the tax bill markup is expected to start on Monday next week.

Drama related to the tax bill ain’t the only possible catalyst for the Greenback, however, since the U.S. will also be releasing its latest CPI and retail sales reports next week. Also, a lot of FOMC members are scheduled to give speeches next week.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

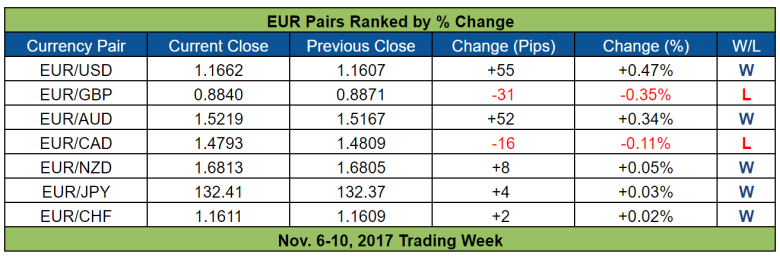

The Euro

The euro ended up as a net winner this week, but it actually had a weak start. There were no apparent catalysts, but some market analyst said in hindsight that the euro’s early slide may have been due to monetary policy divergence between the ECB and the Fed.

I’m not too sure about that, however, since the euro traded roughly sideways against the Greenback but was weak against most other currencies. But then again, the Greenback was also showing weakness at the time.

In any case, the euro had a more mixed performance while trading roughly sideways after that before finally catching a bid come Thursday, apparently because of comments from ECB’s Cœuré, the positive economic forecasts from the European Commission, and the ECB’s upbeat economic assessment.

As for details, I already gave a decent breakdown during Thursday’s London session recap. But to summarize, the ECB’s latest economic bulletin revealed that the ECB thinks that “Risks surrounding the euro area growth outlook remain broadly balanced.”

On the one hand, prospects for the Euro Zone’s economy is positive since “consumption growth is expected to remain resilient” and “business investment should continue to grow in the third quarter of 2017” while “survey-based indicators point to sustained momentum” in-line with sustained global growth.

But on the other hand, “downside risks continue to relate primarily to global factors and developments in foreign exchange markets.”

The European Commission’s (E.C.) Autumn 2017 Economic Forecast, meanwhile, showed that the E.C. upgraded its growth forecasts, with the 2017 forecast of +2.2% being the fastest rate of expansion in a decade.

The E.C.’s forecasts for HICP were more mixed but net positive, however, since the E.C. downgraded its forecast for 2017 while upgrading its forecast for 2018 and then projecting a HICP to accelerate to 1.6% by 2019.

And like the ECB, the E.C. assessed that “The risks that economic developments could turn out better or worse than forecast are broadly balanced.”

As for ECB Board Member Benoît Cœuré’s comments, he gave the following rather hawkish statements:

“A lot of people would like us to continue quantitative easing forever, but the depth of European capital markets is totally different to that in the United States.”

“Personally, I don’t think quantitative easing can be a permanent instrument of ECB monetary policy simply because financial markets are not deep enough.”

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

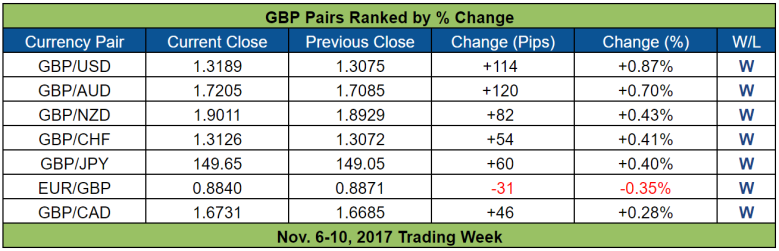

The Pound Sterling

After stumbling last week, the pound resumed its upward push this week and took back its throne as king of pips (or queen, if you like). The pound’s climb was not exactly easy, which is why weekly % changes on pound pairs are relatively subdued.

Anyhow, the pound’s path to the top started from the get-go when the pound started climbing higher on Monday.

There were no apparent catalysts, but some market analysts pointed to profit-taking by pound shorts after last week’s pound selloff in the wake of the BOE’s dovish hike.

The pound’s rally finally started to run out of steam during Wednesday’s Asian session. Again, there were no apparent catalysts, but the most likely reason for the pound’s slide is renewed Brexit-related jitters since the 6th round of Brexit negotiations were scheduled to begin on Wednesday.

However, some market analysts also blamed the pound’s slide on growing political uncertainty amid growing doubts over Theresa May’s authority after Secretary of State for International Development Priti Patel failed to disclose meetings with Israeli officials while Patel was supposedly on holiday.

I’m not really sure about that, though, since news about Patel began to circulate early on Monday and the pound just shrugged that off.

Anyhow, the pound had a very choppy Thursday before rising broadly higher on Friday, apparently as a reaction to positive U.K. data.

As for specifics, total industrial production in the U.K. during the September period expanded by 0.7% month-on-month, beating the consensus that it would match the previous month’s pace of +0.3%, as well as marking the sixth consecutive month of growth.

The year-on-year reading is also impressive since total industrial production surged by 2.5% (+1.9% expected, +1.8% previous), which is the best reading in seven months and marks the fourth consecutive month of stronger readings to boot.

Another upbeat report was the U.K.’s September trade report since it showed that the U.K.’s total trade deficit fell to £2.75 billion from £3.46 billion.

However, the picture for Q3 as a whole ain’t as pretty since exports fell by around 0.2% between Q2 and Q3, while imports surged by 1.6%, which means that trade was very likely a drag on Q3 growth. However, it remains to be seen if the bigger trade gap for Q3 will result in a downgrade for the U.K.’s Q3’s GDP reading.

At this point, it should also be worth mentioning that the 6th round of Brexit talks ended on Friday. Not much progress was made, so much so that Michel Barnier, the E.U.’s top Brexit negotiator, referred to the talks as “hardly anything.” However, talks didn’t deteriorate at the very least.

Also, there was a bright spot for a possible start to trade talks by December since Barnier gave the U.K. two weeks to either provide concessions (i.e. pony up more cash) or clarify its positions on the E.U.’s three key issues, namely the U.K.’s Brexit divorce bill, the Irish border, and citizens’ rights. And this bright spot may have also contributed to the pound’s Friday rally.

Hopefully, we’ll get more volatility from the pound next week since the U.K. will be releasing its latest jobs report, CPI report, and retail sales report. Also, BOE Guv’nah Carney and friends are scheduled to speak and maybe they’ll sing a different tune this time (or not).

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

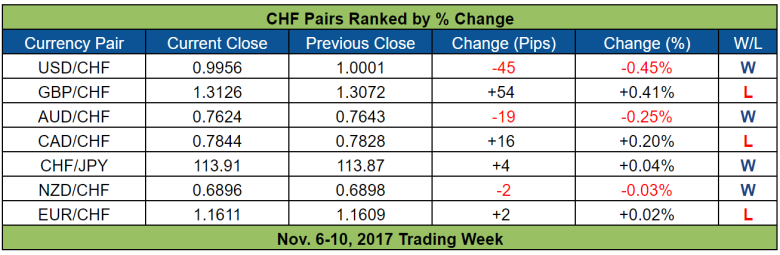

The Swiss Franc

The euro edged out the Swissy, so the Swissy had a more mixed performance this week while still a net winner. And yes, the Swissy and the euro were still dancing in tandem.

Interestingly enough, the Swissy actually outperformed the euro at first, likely because of the risk-off vibes. However, the Swissy suffered a weird bout of weakness on Friday and that was literally all it took for the euro so steal a better ranking from the Swissy.

I kid you not. Just look at the sample pairs below. As to what caused the Swissy to weaken even though risk aversion prevailed, there’s no clear reason for that. Perhaps the SNB was sneakily weakening the Swissy again?

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Japanese Yen

I asked in last week’s JPY recap if the yen is finally decoupling from bond yields. And, well, the answer appears to be “no” since the yen took directional cues from global bonds yields this week, at least from Monday to Thursday.

However, the yen acted as a safe-haven as well. And this is made clear when bond yields began climbing after the U.S. Senate’s tax plan was revealed but the yen held its ground and only grudgingly weakened on some pairs, very likely because disappointment over the U.S. Senate’s version of the tax plan caused global risk sentiment to sour, which then likely sent safe-haven flows towards the yen.

Incidentally (well, not really), the yen’s mixed price action on Friday is also the reason why the yen had a mixed performance this week.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

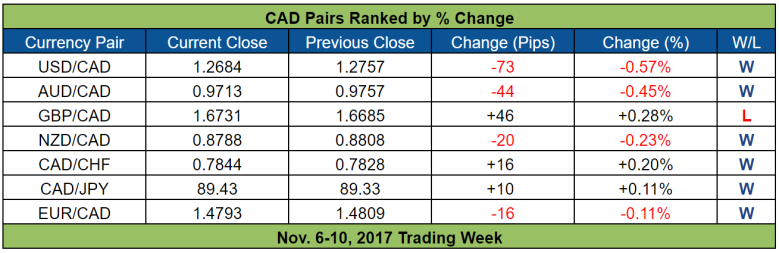

The Canadian Dollar

That overlay of CAD pairs already exclude GBP/CAD and NZD/CAD but the Loonie’s overall price action still looks kinda messy, which means that the Loonie was somewhat vulnerable to opposing currency price action.

Still, the Loonie did end up as the second-strongest currency of the week (for what it’s worth). Oil was likely a factor since most Loonie pairs climbed higher when oil surged on Monday. And it also looks like the Loonie was taking directional cues from oil on Thursday and less so on Friday.

However, the Loonie also diverged from oil on Tuesday and Wednesday, especially after the text of BOC Boss-Man Poloz’s speech was released. In fact, the Loonie caught a bid on most pairs after Poloz’s speech was released.

So what did Poloz have to say? Well, he reiterated the BOC’s neutral forward guidance when he said the following:

“As we said last month, while the economy is likely to require less monetary stimulus over time, we will be cautious in making future adjustments to our policy rate. In particular, the Bank will be guided by incoming data to assess the evolution of economic capacity, the dynamics of both wage growth and inflation, and the sensitivity of the economy to higher interest rates.”

However, Poloz also added that “A lot of pieces need to fall into place before we can be certain that the economy has made it all the way home.” Still, Poloz did note that “the underlying trend in inflation is well within the target range we have committed to.”

Overall, Poloz did not really say anything dovish. One can even argue that his assessment that “the underlying trend in inflation is well within the target range” is a bit hawkish. And as such, market analysts generally viewed Poloz’s speech as balanced or less-dovish-than-expected, which is likely why the Loonie caught a bid even as oil fell on Wednesday.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

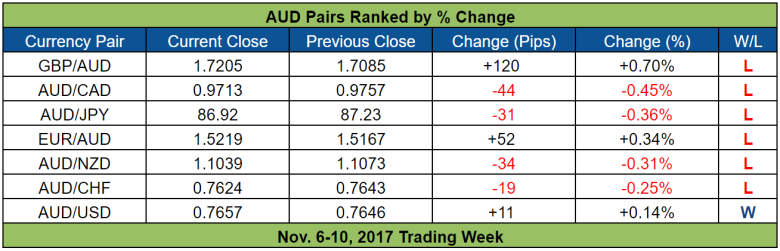

The Australian Dollar

As usual, the Aussie was tracking gold prices for the most part. However, the Aussie was also vulnerable to risk sentiment this week, particularly to risk aversion.

And this can be clearly seen when the gold rose on Thursday but the Aussie tanked, even though there were no apparent catalysts, which leaves the prevalence of risk aversion on that day as the sole culprit.

Oh, we also had the latest RBA monetary policy decision this week, which caused the Aussie to toss and turn. However, that event was ultimately a dud and the Aussie ended up taking directional cues from gold prices.

As for some details, the RBA kept the cash rate unchanged at 1.50% while sounding neutral. And as usual, the RBA did not have any real forward guidance. Also as usual, the RBA repeated its warning that:

“The Australian dollar has appreciated since mid year, partly reflecting a lower US dollar. The higher exchange rate is expected to contribute to continued subdued price pressures in the economy. It is also weighing on the outlook for output and employment. An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.”

Another RBA-related event was the release of the RBA’s Statement on Monetary Policy. And that caused the Aussie to react negatively at first, likely because the RBA downgraded its CPI projections.

The Aussie quickly rebounded, however, likely because “the assessment of pricing pressures in the near term has not changed” and inflation is still expected to gradually rise, according to the RBA.

Moreover, the RBA explained that “inflation has been revised a little lower over the forecast period to allow for the upcoming reweighting of the CPI in the December quarter.”

Also, the RBA gave the closest thing to a forward guidance when it said that:

“The cash rate is assumed to move broadly in line with market pricing.”

And in its market-based forecast for the cash rate, the RBA sees a 25 basis point rise by the middle of next year. The implication, of course, is that the RBA is expected to hike next year.

The RBA apparently didn’t want to appear hawkish, though, which is why it was quick to add the following disclaimer:

“This does not represent a commitment by the Reserve Bank Board to any particular path for policy.”

Even so, the RBA’s implied hawkish leanings apparently caught the eye of some Aussie bulls since the Aussie grinded higher in defiance of easing gold prices.

Unfortunately for the Aussie, Aussie bulls were forced to scream “we surrender” when gold continued to trend lower and risk sentiment deteriorated on Friday.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

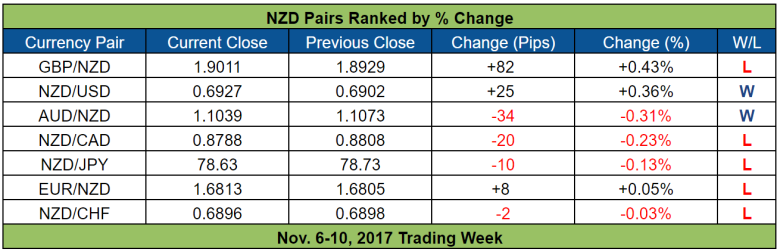

The New Zealand Dollar

The Kiwi was the third worst-performing currency this week and the Kiwi’s price action was dictated by risk sentiment for the most part.

As such, the Kiwi broadly rose on Monday when risk-taking was the name of the game and then dipped on Tuesday when risk sentiment soured ahead of the latest dairy auction. Speaking of the latest dairy auction, that was a bummer since the GDT price index slumped by 3.5%, which likely helped to push the Kiwi lower.

Going back to risk sentiment, risk sentiment recovered on Wednesday but began to deteriorate again during the morning London session and ahead of the RBNZ statement.

Fortunately for Kiwi bulls, the RBNZ statement was quite surprising. Forex Gump already has the details so read up on his 4 Takeaways from the November RBNZ Statement & Presser, if you want the details.

The gist of it is that the RBNZ’s remained optimistic on the New Zealand economy and even assessed the new government’s policies as positive overall. Moreover, the RBNZ was not too worried about having full employment added to its mandate, which is why the RBNZ upgraded its forecasts for the OCR to show a possible rate hike by Q2 2019 (Q3 2019 previously) and even forecasted a second hike by Q3 2020.

The RBNZ did frame its forward guidance on the assumption that the Kiwi will remain at current low levels, however. In other words, if the Kiwi rises then that may force the RBNZ to downgrade the path for the OCR. And that probably scared away some Kiwi bulls since the Kiwi’s rally quickly ran out of steam.

To make matters worse for the higher-yielding Kiwi, global risk sentiment became bearish on Thursday and Friday, especially after the U.S. Senate’s version of the Republican tax plan caused doubts to grow that much-awaited tax cuts will be implemented soon.