The forex trading week has come and gone, so it’s time to take a look at how the major currencies performed and what drove price action.

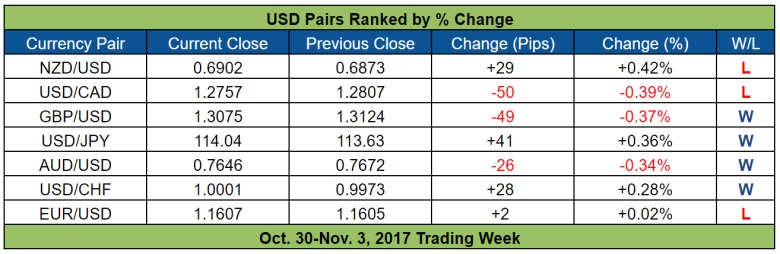

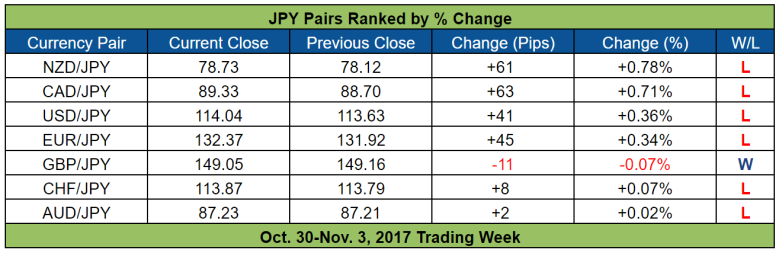

Looking at the table above 6 out of the top 10 movers are Kiwi pairs and the Kiwi is winning out in all of ’em, so Kiwi strength was apparently the main theme this week.

Another observation you may have gleaned is that none of the top 10 movers were able to reach the 1% mark for the weekly % change, so longer-term traders probably didn’t enjoy the trading week too much, despite a ton of reports and events. Shorter-term traders probably had a good time, though.

As to why the directional movement was in short supply, month-end / start-of-month flows are the likely culprits since hedge funds, mutual funds, pension funds, and other large players usually rebalance their portfolios at the end of a month, resulting in some rather wonky price action.

Anyhow, what drove forex price action this week? And what about the other currencies? How did their price action play out and what drove them? Time to find out!

But before that, here’s this week’s scoreboard.

And if you only want to find out what happened to a specific currency, then you can just skip to that currency by clicking on it below.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The U.S. Dollar

Overlay of USD Pairs: 1-Hour Forex Chart

After two weeks of broad-based strength, the Greenback turned out a more mixed performance this week but was still a net winner.

And while price action on the Greenback was kinda messy and directional movement was limited, likely because of month-end / start-of-month capital flows, there were actually a lot of events for the Greenback as marked in the overlay of USD pairs above.

Anyhow, the Greenback had a tough start because of rumors that Trump may pick Powell to replace Yellen as Head of the Fed, rather than Taylor, who is considered as the more hawkish candidate.

The Greenback’s troubles only worsened as the day progressed, thanks to news that special counsel Robert Mueller filed charges against Trump’s associates from the election campaign.

The charges were not really relevant to Trump himself or Trump’s election campaign since Paul Manafort and Rick Gates were charged with money laundering, tax evasion, fraud, and failure to disclose and register that they are agents of a foreign principal under the Foreign Agents Registration Act (FARA) for activities on behalf of Ukraine (NOT Russia) between the years 2006 until 2014.

Moving on, the Greenback found support and began trading higher on Tuesday. There were no direct catalysts, but some market analysts pointed to relief buying aftermarket players realized that Mueller’s charges against Trump’s former aides weren’t really that damaging to Trump, as well as renewed hopes that Trump may pick a more hawkish candidate to replace Yellen as Fed Head.

After that, the Greenback’s price action became a mess on Wednesday as the FOMC statement loomed.

And when the FOMC statement did finally roll around, the Greenback jumped higher on most pairs, likely because the Fed decided to keep rates steady while maintaining the following forward guidance:

“The Committee expects that economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run.”

This was apparently taken to mean that the Fed is still on track for a December rate hike. However, the Fed didn’t really say anything new, so follow-through buying didn’t materialize and the Greenback quickly steadied after the initial reaction before getting slapped lower when Thursday’s Asian session came about, likely because of a flurry of news reports from The New York Times and The Wall Street Journal (among others) claiming that Trump will choose Powell as the next Fed Head.

The Greenback then steadied and even caught a bid ahead of the House’s Tax plan bill. And when the Tax plan was revealed, the Greenback reacted negatively, probably because of worries that the tax plan may not be able to pass through Congress as well as worries that even if the plan is passed, the impact on the U.S. economy would not be that meaningful. Well, that’s what some market analysts think anyway.

Moving on, the next major event was Trump’s announcement that he chose Powell as the next Fed Head. And interestingly enough, that event was a dud, probably because forex traders have had enough of all those Fed rumors all week and were looking forward to the NFP report. Also, the U.S. Senate has to confirm Powell’s nomination.

Speaking of the October NFP report, that was a disappointment since non-farm payrolls only increased by 261K, missing expectations for a 313.0K increase. Although the loss of 33K jobs in September was revised to show a small 18K increase, which is good.

And while the jobless rate ticked lower from 4.2% to 4.1%, that was largely due to the labor force participation rate deteriorating from 63.1% to 62.7%.

Also, wage growth was a disappointment since it was flat month-on-month for October after rising by 0.5% previously. A more precise reading is even more disappointing since it reveals that wages actually fell by 0.04%, which is the first monthly decline in almost three years. Year-on-year, wage growth slowed from 2.83% to 2.43%, which is the weakest reading since February 2016.

Given all that, the Greenback reacted quite negatively. However, there was no follow-through selling and the Greenback even snapped higher after both U.S. factory orders (1.4% vs. 1.2% expected, same as previous) and ISM’s non-manufacturing PMI reading (60.1 vs. 58.5 expected, 59.8 previous) both exceeded expectations.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Euro

Overlay of EUR Pairs: 1-Hour Forex Chart

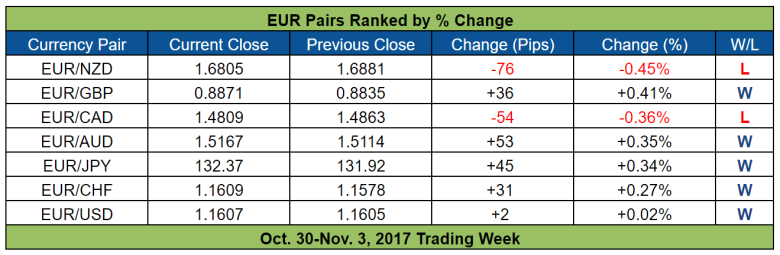

The euro had a good run this week after last week’s losses in the wake of the ECB’s dovish taper.

But as you can see in the overlay of EUR pairs above, the euro’s price action was actually rather messy, with lots of diverging price action, which means that the euro was vulnerable to opposing currency price action.

The euro did have roughly uniform price action at first when it trended higher from Monday to Tuesday. Incidentally, this is the period when the euro captured the bulk of its gains on most pairs.

And the rally was likely initially fueled by easing concerns over Catalonia, thanks to a poll over the weekend from an anti-independence newspaper showing that support for independence has waned, as well as reports on Monday that there were little signs of unrest in Catalonia despite calls by the Catalan government for civil disobedience.

Other than that, it’s also likely that euro bears, who profited when the euro tanked because of the ECB’s taper, were covering their shorts.

The euro’s last hurrah came on Tuesday, apparently because of the Euro Zone’s October HICP report.

Interestingly enough, the headline reading came in at 1.4% year-on-year, which is a tick slower than the +1.5% consensus as well as the ECB’s 2017 forecast, also of +1.5%.

However, HICP is still meeting the ECB’s preferred measures for core inflation since HICP less energy came in at 1.2% year-on-year in, which is in-line with the ECB’s 2017 forecast of 1.2%.

The other preferred measure for core inflation, HICP less energy and unprocessed food, came in 1.1% year-on-year, which is also still in-line with the ECB’s 2017 forecast of 1.1%.

And since underlying inflation is still evolving as expected, the euro found itself some fresh buyers. But as mentioned earlier, that was the euro’s last hurrah since the euro’s price action became a total mess after that. There was no clear reason why, however.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Pound Sterling

Overlay of GBP Pairs: 1-Hour Forex Chart

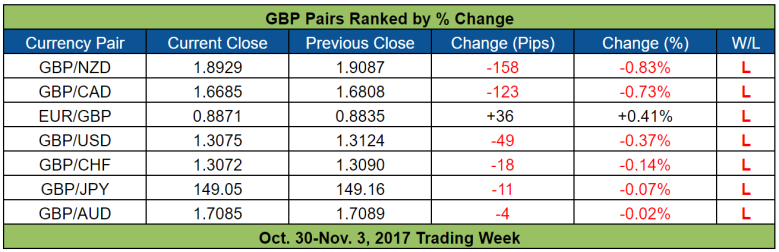

After being a net winner for three consecutive weeks, the pound got dethroned and thrown to the bottom of the forex heap this week.

Interestingly enough, the pound was actually the best-performing currency from Monday to Wednesday. And according to market analysts, the pound’s pre-BOE rally was driven by preemptive bets ahead of the BOE statement on speculation that the BOE will deliver on a highly anticipated rate hike.

Markit released the latest manufacturing PMI (56.3 vs. 55.8 expected, 56.0 previous) and construction PMI (50.8 vs. 48.3 expected, 48.1 previous) for the U.K. ahead of the BOE’s statement. But they didn’t really have a bullish effect on the pound, even though they printed better-than-expected readings.

In fact, pound bulls apparently used those PMI reports to exit their positions since the pound began tilting grudgingly to the downside after the manufacturing PMI report was released.

Anyhow, when the BOE statement finally rolled around, the BOE did deliver on a rate hike, which is the first hike in a decade and caused the pound to jump higher as a knee-jerk reaction.

However, pound bears quickly faded the would-be rally, apparently because of the BOE’s dovish outlook on inflation, which only warrants a “gently rising path” for the Bank Rate.

To quote directly from the BOE’s meeting minutes (emphasis mine):

“The MPC still expects inflation to peak above 3.0% in October, as the past depreciation of sterling and recent increases in energy prices continue to pass through to consumer prices. The effects of rising import prices on inflation diminish over the next few years, and domestic inflationary pressures gradually pick up as spare capacity is absorbed and wage growth recovers. On balance, inflation is expected to fall back over the next year and, conditioned on the gently rising path of Bank Rate implied by current market yields, to approach the 2% target by the end of the forecast period.”

Also according to the BOE’s meeting minutes, this “gently rising path” means only “two additional 25 basis point increases in Bank Rate over the three-year forecast period.”

What a bummer (for pound bulls). And to rub salt on the pound’s wound, the BOE also expressed concern about Brexit when it noted the following:

“Uncertainties associated with Brexit were weighing on domestic activity, which had slowed even as global growth had risen significantly. And Brexit-related constraints on investment and labour supply appeared to have been reinforcing the marked slowdown that had been increasingly evident in recent years in the rate at which the economy could grow without generating inflationary pressures.”

Moreover, the vote for a rate hike was not unanimous because:

“Two members … did not support an increase in Bank Rate. These members felt that there was insufficient evidence so far that domestic costs, in particular wage growth, would pick up in line with the Inflation Report’s central projection. It was possible that there was a greater degree of slack in the economy than was assumed in the central case, for example, if a larger part of the recent weakness in productivity had been cyclical. In addition, for those members, recent experience suggested that wage growth could continue to be less responsive to falling unemployment than past experience would suggest.”

Moving on, the pound later found support and even began climbing higher after Markit released the latest U.K. services PMI report, which revealed that the reading for October came in at 55.6, jumping from the previous month’s 53.6 and contrary to expectations that the reading would deteriorate slightly to 53.3.

The damage was already done, however. And so the pound ended up as this week’s main loser.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Swiss Franc

Overlay of CHF Pairs: 1-Hour Forex Chart

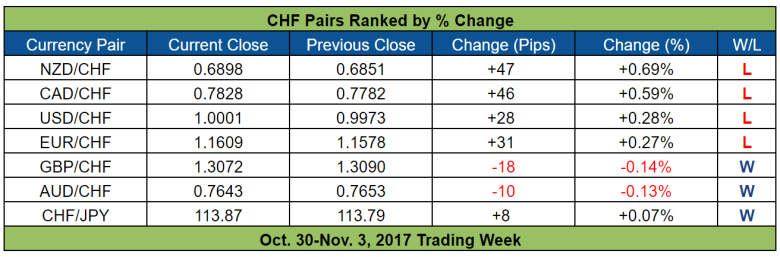

The Swissy had a report performance since it had another mixed week. And as usual, the Swissy and the euro were dancing in-step for the most part. But as you can see in the sample pairs below, the Swissy did not get a lift from the Euro Zone’s HICP report on Tuesday. Also, the safe-haven Swissy was much more vulnerable to the risk-on vibes on Wednesday.

USD/CHF (inverted, red) vs. EUR/USD (black): 1-Hour Forex Chart

NZD/CHF (inverted, red) vs. EUR/NZD (black): 1-Hour Forex Chart

CHF/JPY (red) vs. EUR/JPY (black): 1-Hour Forex Chart

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Japanese Yen

Overlay of Inverted JPY Pairs & US10Y Bond Yield (Black Line): 1-Hour Forex Chart

The yen was the second weakest currency of the week, even though global bond yields fell, which should have provided support for the yen.

And while the BOJ announced its latest monetary policy decision this week, that event turned out to be a dud (as usual) and yen pairs were still taking directional cues from bond yields at the time.

As for specifics on what the BOJ had to say, well, the BOJ maintained its current monetary policy, including its so-called QQE with yield curve control framework that targets the bond yields of 10-year Japanese government bonds. In addition, the BOJ upgraded its growth forecasts for fiscal year 2017 (again) while downgrading its inflation forecasts for the 2017 and 2018 fiscal years (yet again).

Overall, nothing really new or unexpected, which is probably why the event was a dud (as usual) and yen pairs turned to bond yields for directional cues.

However, bond yields and yen pairs began diverging come Wednesday since global bond yields began falling but the yen continued to weaken against its peers.

There were no apparent catalysts, but the most likely reason appears to be the news that the Japanese Lower House re-elected Shinzo Abe as Prime Minister since that means another round of Abenomics, which likely means that the BOJ won’t be budging from its super loose monetary policy any time soon. Moreover, expectations are high that Japan will take a harder stance on North Korea under Abe.

Anyhow, there were signs that yen pairs still tried to track bond yields. However, selling pressure was persistent after Shinzo Abe was re-elected as the Japanese PM.

Of course, it’s also possible that we’re just seeing wonky price action related to month-end and/or start-of-month capital flows. After all, hedge funds, mutual funds, pension funds, and other large players usually rebalance their portfolios, so there’s usually some weird price action going on.

At any rate, it sure would be interesting to see what would happen next week, huh? I guess we’ll know next week if the yen is finally decoupling from bond yields or this week’s decoupling is just a fluke.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

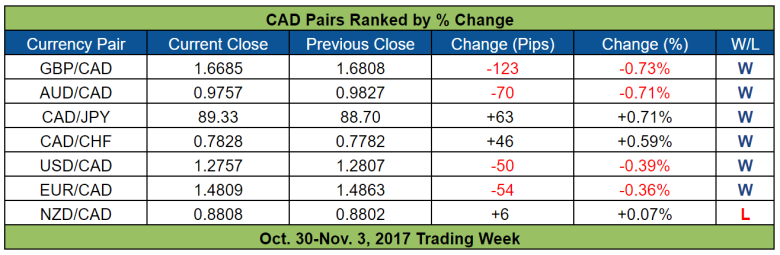

The Canadian Dollar

Overlay of CAD Pairs & Crude Oil (Black Line): 1-Hour Forex Chart

I mentioned in last week’s CAD recap that there were signs that the Loonie was taking directional cues from oil again. And, well, we got even more signs this week, as you probably saw in the overlay of CAD pairs and oil above.

The Loonie’s price action was not dictated solely by oil prices, though, since Canadian economic data also had an impact, namely the Canadian monthly GDP report, which surprised by printing a 0.1% contraction in August instead of growing by 0.1% as expected.

The details of the report show that declines in manufacturing and mining, quarrying and oil and gas extraction were the reasons for the negative month-on-month reading, with the 0.8% contraction in the mining, quarrying, and oil and gas extraction sector being the main drag as well as the most disappointing since it marked the third consecutive monthly decline.

Moving on, oil prices began to rise on Tuesday, thanks to speculation that U.S. oil inventories will show a decline, market analysts say. Even so, the Loonie was very reluctant to climb higher, likely because market players were waiting on what BOC Boss-Man Poloz has to say when he testifies before the House of Commons Standing Committee on Finance.

And when Poloz did testify, he warned that:

“We are at a crucial spot in the economic cycle, and significant uncertainties are clouding the way forward.”

Poloz then specified that these uncertainties comprise: inflation, the degree of excess capacity, continued softness in wage growth, and the elevated level of household debt.

Poloz then admitted that the BOC has not included “the risk of a significant shift toward more-protectionist trade policies in the United States, given the range of potential outcomes and the uncertainty about timing.”

The market has likely already discerned and priced in that last bit about the BOC not incorporating the risk of protectionist U.S. policies, which is likely why the Loonie has (until recently) been taking cues from NAFTA-related news and Canadian economic reports rather than oil.

Getting back on topic, Poloz then concluded that “the economy is likely to require less monetary stimulus over time,” which is a hawkish message. However, Poloz reiterated the BOC’s forward guidance that the BOC “will be cautious in making future adjustments to our policy rate” because of the uncertainties already mentioned.

Poloz then ended by saying that:

“[T]he Bank will be guided by incoming data to assess the sensitivity of the economy to interest rates, the evolution of economic capacity, and the dynamics of both wage growth and inflation.”

In other words, the BOC’s stance on monetary policy is essentially neutral, but it is cautiously leaning more towards a hiking bias.

Anyhow, this overall dovish message, plus the continued disappointment over Canada’s GDP report, is likely why the Loonie traded roughly sideways even as oil prices surged.

Wednesday’s was opposite that of Tuesday’s price action in that oil was down for the day, thanks to profit-taking, market analysts say, but the Loonie was mostly higher for the day.

Again, forex traders were likely waiting to see if Poloz had anything new to say. And while Poloz’s opening statement was practically the same as his speech on Tuesday, he did have something new to say about the Loonie during the Q&A portion, namely the following (emphasis mine):

“The interest rate difference between Canada and the United States is an important determinant of the Canadian dollar at any point in time.”

“If interest rates are holding constant, then it will be oil prices that do most of the acting. But if oil prices are constant, it tends to be expectations about interest rates that have their biggest influence on the dollar.”

Poloz also talked about how expectations with regard to monetary policy have caused the Loonie to decouple from oil, but he added that from a longer-term perspective, it’s the relationship between oil and the Loonie that usually holds sway.

And on that note, oil was on the second leg of its upward push for the week. And this time, the Loonie took directional cues from oil prices since it steadily climbed on Thursday, even though there were no other catalysts.

The Loonie decoupled from oil on Friday, though, since the Loonie jumped ahead of oil prices, thanks to Canada’s jobs report.

You see, the Canadian economy generated 35.3K jobs in October, which is more than double the consensus figure of +15.0K. Even better, jobs growth was fueled by the 88.7K increase in full-time jobs, which was partially offset by the loss of 53.4K part-time jobs.

And while the jobless rate deteriorated by ticking higher from 6.2% to 6.3%, it wasn’t all that bad since the labor force participation rate climbed higher from 65.6% to 65.7%, which means more Canadians were encouraged to look for jobs, but the Canadian economy wasn’t able to completely absorb the influx of new and returning workers.

On a much more upbeat note, average hourly wages grew by 2.4% year-on-year, which is the strongest reading since April 2016 and is likely the decisive factor that caused the Loonie to spurt higher across the board since wage growth is more directly related to consumer spending and inflation.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

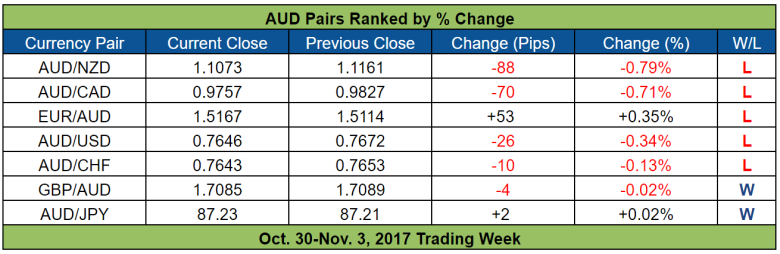

The Australian Dollar

Overlay of AUD Pairs & Gold (Black Line): 1-Hour Forex Chart

As you can see in the overlay of AUD pairs and gold above, the Aussie was tracking gold prices for the most past, as has been the case for the past few weeks since the Aussie decoupled from iron ore.

And since gold was down for the week because of the prevalence of risk appetite, the Aussie ended up as a net loser, even though the Aussie is considered a higher-yielding currency.

There were a few Australian economic reports that were released during the week, but only Australia’s retail sales report had a noticeable effect on the Aussie’s price action since gold was somewhat steady at the time but the Aussie got kicked sharply lower across the board.

As for specifics, retail trade turnover showed no growth during the September period, which is a disappointment because the consensus was for a 0.4% gain after last month’s 0.5% decline.

The year-on-year reading is even more disappointing since it came in at 2.0% (+2.5% previous), which marks the fourth consecutive month of ever weaker readings, as well as the weakest reading since October 2008 when the annual reading also came in at 2%. By the way, did I mention that the 2% reading is a record low? Yep, that’s how it is, which is likely why the Aussie reacted quite negatively to the retail sales report.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

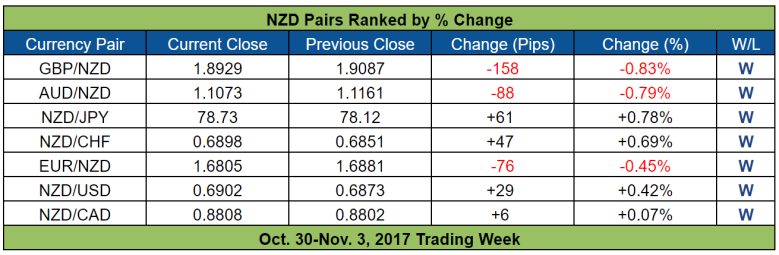

The New Zealand Dollar

Overlay of NZD Pairs: 1-Hour Forex Chart

For what it’s worth (given the small weekly % changes), the Kiwi was the best-performing currency of the week. And Kiwi bulls can thank New Zealand’s Q3 jobs report for that.

You see, employment grew by 2.2% quarter-on-quarter in Q3, which is a much stronger growth compared to the consensus for a 0.8% increase.

And this surge in employment caused the jobless rate to slide from 4.8% to 4.6%, which is the best reading since Q4 2008. And the slide in the jobless rate was all due the stronger jobs growth since the labor force participation rate actually jumped from 70% to 71.1%, which is an all-time high and means that the New Zealand economy was able to absorb new workers, the unemployed, and people who decide to rejoin the labor force.

Even better, the labor cost index increased by 1.9% year-on-year. This is faster than the previous quarter’s +1.7% and is the strongest reading since Q3 2012.

More importantly, the +1.9% reading is already exceeding the RBNZ’s forecast of +1.5% for 2017, which is likely the Kiwi’s bullish reaction to the jobs report was relatively strong.

After the Kiwi’s bullish reaction, however, there was little follow-through buying and the Kiwi ended up trading roughly sideways against most of its rivals, likely because forex traders were wary of positioning heavily ahead of next week’s RBNZ statement.

And on that note, make sure to keep an eye on the Kiwi next week since there’s going to be a presser after the RBNZ statement and it’s very likely that the press will try to ask what the RBNZ thinks about the new government and its plans to add full employment to the RBNZ’s mandate.

Moreover, the RBNZ will be releasing its latest Monetary Policy Statement (you can find it here when it’s available). Aside from the RBNZ’s updated economic forecasts, forex traders will likely be keen to find out if the RBNZ is still on track for a 2019 hike to the OCR.

After all, New Zealand Finance Minister Grant Robertson said last Sunday that the new government’s planned policy changes for the RBNZ could “potentially” mean lower rates, which is why the Kiwi initially had a tough time this week before springing higher because of New Zealand’s jobs report.