The forex trading week has come and gone, so it’s time to take a look at how the major currencies performed and what drove price action.

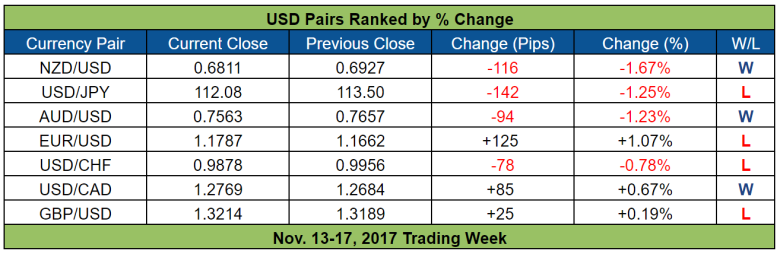

After two weeks of poor weekly volatility, we finally got a decent trading week this week. And looking at the table above, half of the top 10 movers are Kiwi pairs, with the Kiwi losing out in all cases. As such, Kiwi-bashing was a major theme this week.

But as you’ll learn later (or if you took a peek at the scoreboard), comdoll-bashing was actually the theme this week, together with demand for the lower yielders, mainly the yen.

So, what drove forex price action this week? Well, time to find out!

But before that, here’s this week’s scoreboard.

And if you only want to find out what happened to a specific currency, then you can just skip to that currency by clicking on it below.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The U.S. Dollar

The Greenback had a mixed performance this week, with diverging price action, which very obviously means that the Greenback was vulnerable to opposing currency price action.

The Greenback had a mixed but steady start but began finding sellers on Tuesday. There were no apparent catalysts for the slide on Tuesday. Although later news about the tax plan may have weighed on the Greenback.

Wednesday is the day when it became clear to all (well, those who look at their charts anyway) that the Greenback was vulnerable to opposing currencies since price action on Greenback pairs began to clearly diverge, with the Greenback winning out against the comdolls while losing out to the euro and the safe-havens and trading roughly sideways against the pound.

The October U.S. CPI report and October U.S. retail sales report were released on Wednesday, but those didn’t really do jack for the Greenback’s price action, which highlights just how vulnerable the Greenback was to opposing currency price action.

As for some details, on those economic reports, CPI rose by 0.1% month-on-month in October, which is lower than September’s 0.5% increase but is in-line with analysts’ expectations. This translates to a year-on-year increase of 2.0%, which is tad lower than September’s 2.2% reading.

Meanwhile, the core reading strengthened by 0.2% month-on-month (0.1% previous). Year-on-year, the core reading increased by 1.8%, beating expectations for a 1.7% improvement.

As for the retail sales report, that showed that total retail sales value increased by 0.2% in October, which is more than the expected 0.1% increase. That’s still a pretty drastic slowdown compared to the previous month’s upwardly revised 1.9% increase, though.

Moving on, Thursday was another mixed day for the Greenback. The biggest event on that day was the expected vote on the House’s version of the tax reform bill. However, that event turned out to be a dud, even though the House of Representatives successfully passed the bill, likely because the U.S. Senate also has to approve its version.

Anyhow, the Greenback did finally see some uniform price action, thanks to a Wall Street Journal report (with unnamed sources as per the usual) that Special Counsel Robert Mueller’s team supposedly issued a subpoena for documents on the Trump campaign related to the conspiracy theory about alleged Russian involvement in the 2016 U.S. elections that propelled Trump to the Presidency.

The Greenback’s slide lasted for a good four hours. However, it soon became obvious that opposing currencies dictated price action on Greenback pairs since price action began to diverge again.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Euro

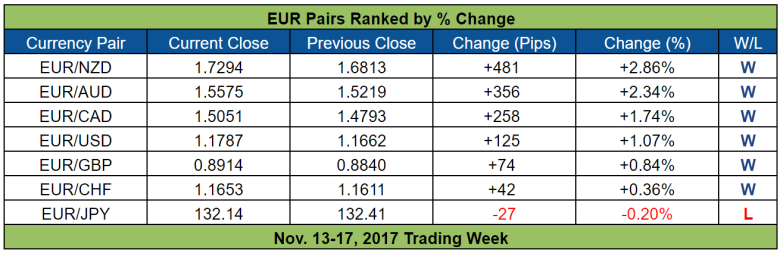

The euro was the second best-performing currency of the week. And as you can see above, the euro captured the bulk of its gains on Tuesday and the earlier half of Wednesday.

The euro then shed some of its gains during the later half of Wednesday before trading roughly sideways on Thursday and then having a more mixed performance on Friday.

As to what drove the euro higher on Tuesday and Wednesday, the catalyst was apparently Germany’s Q3 GDP report since there wasn’t really anything else.

As for specifics, Germany’s GDP expanded by 0.8% quarter-on-quarter in Q3, which is stronger than the consensus that Q3 would match Q2’s 0.6% growth rate. Year-on-year, this translates to a seasonally-adjusted reading of 2.8%, which is the strongest reading since Q1 2014, and is a very good sign for the Euro Zone’s largest economy.

Despite Germany’s strong Q3 GDP, however, the second estimate for the whole Euro Zone’s Q3 GDP, which was released a few hours after Germany’s GDP report, was unrevised at +0.6% quarter-on-quarter and +2.5% year-on-year.

Still, the Euro Zone’s annual growth of 2.5% is the strongest since Q1 2011. Also, 2.5% is already well above the ECB’s forecast that the Euro Zone economy as a whole will grow by 2.2% in 2017, as laid out in the ECB’s September Staff Projections.

From a “bigger picture” macroeconomic perspective, strong growth in the Euro Zone and prospects for even stronger growth have also apparently attracted capital flows into the Euro Zone, according to market analysts.

Some market analysts even say that Japanese investors have gained an appetite for European government bonds because European bonds are supposedly seen as attractive alternatives to U.S. government bonds because of stronger growth in the Euro Zone.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Pound Sterling

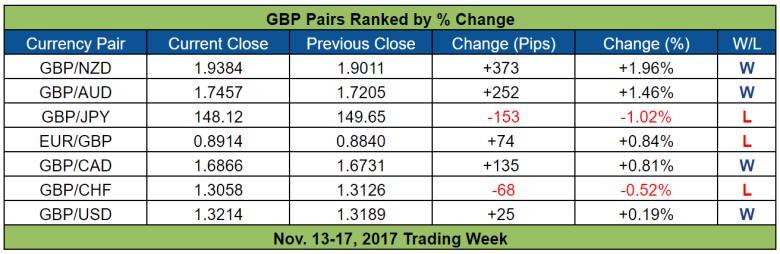

Like the Greenback, the pound had a mixed performance this week, which means that the pound was also vulnerable to opposing currency price action.

Still, it’s worth noting that price action on the pound was more uniform compared to the Greenback.

The pound, for example, gapped lower against most of its peers at the start of the week and then got swamped by even more sellers, thanks to a Sunday Times report over the weekend that claimed that as many as 40 members of Parliament agreed to sign a letter of no-confidence, which alarmed market players since it only takes 48 to trigger an official leadership challenge on the PM.

Next, the pound got slapped lower on Tuesday when the U.K.’s October CPI report was released since since headline inflation in the U.K. only printed a weak 0.1% month-on-month rise, missing expectations for a 0.2% increase and slower than the previous month’s +0.3%.

Year-on-year, CPI clocked in at +3.0%, maintaining the previous month’s pace but missing expectations that it would accelerate to +3.1%. More importantly, the +3.0% annual reading is below the BOE’s forecast that CPI will rise by 3.2% year-on-year in October, as laid out in the November Inflation Report.

Even so, the +3.0% annual increase still marks the ninth consecutive month that CPI has been well above the BOE’s inflation target of +2.0%.

And the realization that CPI is still too strong and that the BOE may still need to hike to restrain CPI likely made pound bears wary of sending the pound lower since follow-through selling on the pound was limited and the pound even began to climb higher on most pairs.

Of course, it’s also possible that pound bears who shorted on Monday were just covering their shorts because the first round of debates on the Brexit Bill, which started on Tuesday, went in favor of Theresa May’s government. Also, the rumored no-confidence challenge against Theresa May’s leadership didn’t really materialize and was quietly swept under the rug.

The pound then steadied on Wednesday before climbing higher a few hours before the U.K.’s jobs report was released.

And when the U.K.’s latest jobs report was finally released, the pound jumped even higher as a knee-jerk reaction because the report looked good on the surface, with the jobless rate for the three months to September unchanged at a record low 4.3% and the number of people who claimed unemployment benefits increasing only by 1.1K in October, which is less than the expected 2.9K increase. Also, total average weekly earnings increased by 2.6% year-on-year in September, strengthening from August’s +2.4%

However, the pound quickly found sellers, likely because wage growth was not as impressive upon closer inspection. To be more specific, wage growth accelerated in September because total bonuses surged by 16.5% (+5.4% previous).

If bonuses are excluded, then average weekly earnings only grew by 2.2%, which is a actually slower compared to the previous month’s 2.3%.

Also, inflation is taken into account, then real earnings (excluding bonuses) fell by 0.6% in September, which marks the eighth consecutive month of negative wage growth, as well as the hardest decline in wage growth in five months.

That’s pretty bad. But when you stop and think about it, persistent negative real wage growth does mean that the BOE will be less likely to tolerate higher inflation, which may have stopped forex traders from pushing the pound even lower.

However, it’s also probable that market players breathed a sigh of relief when the second day of debates on the Brexit Bill ended in favor of Theresa May’s government yet again. Also, the rumored no-confidence challenge still remained a rumor with no signs of becoming reality.

After that, the pound steadied again then dropped ahead of the U.K.’s retail sales report, only to pop higher later because the October retail sales report revealed that retail sales volume in the U.K. expanded by 0.3% in October, beating expectations for a slightly weaker 0.2% increase.

The year-on-year reading for retail sales volume printed a 0.3% decline, however, which is the first negative annual reading in four years. Even so, the annual reading was expected to print a harder year-on-year slide of 0.5%, so the -0.3% is still somewhat good.

Also, September’s reading was upgraded, which means that retail sales for all of Q3 was also upgraded from 0.6% quarter-on-quarter to 0.7%. And this likely increased expectations that U.K.’s Q3 GDP growth will get an upgrade as well since the pound found some follow-through buyers after the retail sales report was released.

And demand for the pound was notable until Friday when the pound finally began to falter. And the pound’s wobble on Friday was blamed by market analysts on profit-taking to avoid weekend risk amid renewed Brexit fears, especially after E.U. Council President Donald Tusk repeated the E.U.’s position that the U.K. needs to clarify its position on the key issues, particularly with regard to Ireland and the U.K.’s divorce bill, before the E.U. will agree to start post-Brexit trade talks by December.

Incidentally, the pound’s Friday slide is the reason why the pound had a mixed performance but still a net winner this week since the Friday slide allowed the Swissy to win out against the pound.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Swiss Franc

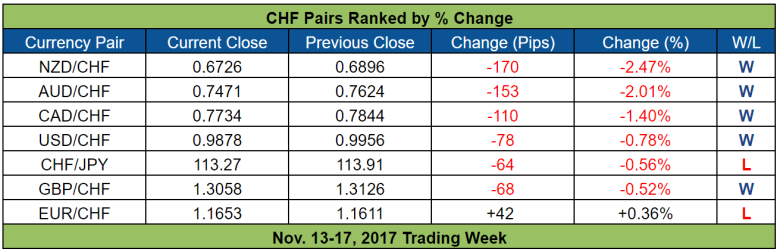

The euro was the second strongest currency of the week while the Swissy came in third place.

So, are the euro and Swissy still dancing in tandem? Yes, without a doubt. But as you can see in the sample pairs below, the euro got a bigger boost from Germany’s better-than-expected Q3 GDP report, which allowed the euro to outpace the Swissy.

As you can also see below, the Swissy was more vulnerable to risk sentiment since the euro traded roughly sideways on Thursday but the safe-haven Swissy was feeling some bearish pressure, very likely because of the returning risk-on vibes at the time.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

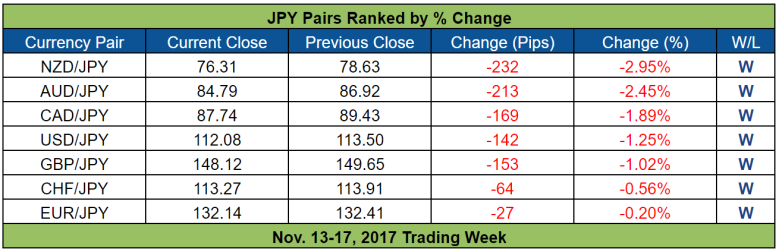

The Japanese Yen

The yen reigned supreme this week. And as usual, the yen took directional cues from bond yields. And since bond yields were down for the week because of the prevalence of risk aversion, the yen ended up getting a bullish infusion.

Oh, as marked on the overlay of inverted JPY pairs and the yield for benchmark U.S. 10-year government bonds, there was a decoupling between yen pairs and bond yields on Thursday.

However, the rise in U.S. bond yields on Thursday, did not tell the whole story. You see, U.S. bond yields rose because of positive U.S. data which reinforced expectations for a December rate hike, according to market analysts.

The same did not hold true for other bond yields, though, especially European bond yields. And this can be clearly seen when you look at the overlay of inverted JPY pairs and the yield for benchmark German 10-year government bonds.

And European bond yields were flat or down on Thursday because of strong foreign demand for European bonds amid higher expectations for stronger growth in the Euro Zone, market analysts say.

And also according to these market analysts, Japanese investors are the main buyers of European government bonds because Japanese investors supposedly see European bonds as a more attractive alternative to U.S. government bonds.

I suppose that also helps to explain why the yen took more directional cues from European bond yields rather than U.S. bond yields on Thursday.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

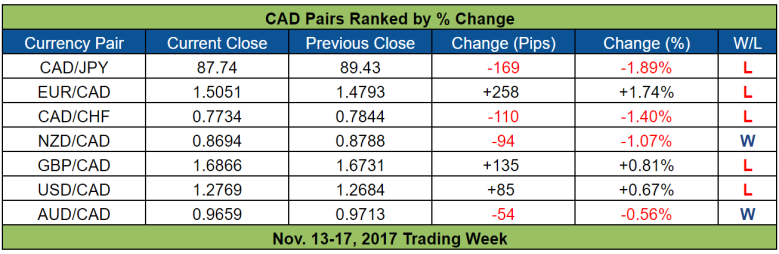

The Canadian Dollar

The Loonie was the third worst-performing currency of the week. And the Loonie suffered the bulk of its losses on Monday and Tuesday, apparently because the Loonie was tracking the slide in oil prices.

And the slide in oil prices, in turn, was blamed by market analysts on rising U.S. oil output, as well as the International Energy Agency’s (IEA) downgraded global oil demand forecasts, which contradicts OPEC’s rosier outlook that demand for oil will strengthen.

However, as marked on the overlay of CAD pairs and oil earlier, the Loonie’s positive correlation to oil began to unwind starting on Wednesday.

As marked earlier, oil began to find support on Wednesday but the Loonie continued to slide lower. And the likely reason for this is that renewed worries over NAFTA negotiations weighed on the Loonie, given that Canada challenged the U.S. on import duties imposed by the U.S. ahead of the fifth round of NAFTA talks on Friday, November 17.

Other than NAFTA-related worries, Loonie traders may have also been wary of tracking oil prices too closely because Nebraska regulators are expected to decide on whether or not to approve a route for TransCanada’s Keystone XL pipeline next Monday, November 20. And activist groups opposed to the pipeline were making a fuss ahead of the November 20 decision on Wednesday.

Thursday’s price action is a bit weird since the Loonie appeared to take cues from oil again. However, the Loonie’s price action became mixed later before showing signs of weakness again, even as oil began to tilt higher.

Preemptive positioning ahead of Canada’s CPI report is a possibility. However, a more likely reason is that forex traders were worried about the prospects for TransCanada’s Keystone XL pipeline, especially after word got around that the pipeline leaked around 5,000 barrels in South Dakota, which forced TransCanada to shut down the pipeline.

Incidentally, oil prices began to move higher and then surged higher on Friday because of news about the leak, market analysts say.

However, negative news related to the Keystone XL pipeline ain’t really very positive for the Canadian economy (and the Loonie for that matter), which is likely why the Loonie didn’t want to track oil prices higher.

The Loonie got a final bearish kick on Friday, apparently as a reaction to Canada’s October CPI report, given that headline CPI only increased by 0.1% month-on-month as expected, which is a tick slower compared to the previous month’s 0.2% increase.

Year-on-year, headline CPI increased by 1.4% in October, slowing down from September’s +1.6% and ending three consecutive months of ever stronger annual readings.

Despite the weaker annual reading, however, the +1.4% increase in October is still in-line with the BOC’s forecast that CPI will average around 1.4% in Q4, as laid out in the BOC’s October Monetary Policy Report.

The BOC’s three preferred measures for underlying inflation were a bit mixed, though, since the common component CPI ticked higher to a 16-month high of 1.6% while the weighted median CPI eased from 1.8% to 1.7%. As for the trimmed mean CPI, it printed a 1.5% increase for the third consecutive month.

Anyhow, the Loonie appeared to take directional cues from oil again after Canada’s CPI report was released, likely because Nebraskan government officials announced that Thursday’s Keystone XL pipeline leak won’t affect their decision come Monday. Even so, the damage was done and so the Loonie was a loser this week.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

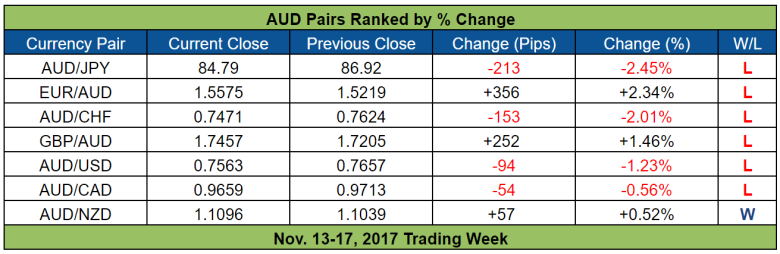

The Australian Dollar

I mentioned in last week’s AUD recap that the Aussie tracked gold prices for the most part while also noting that the Aussie was vulnerable to risk sentiment, particularly to risk aversion.

Well, it looks like the Aussie’s price action this week was dictated mostly by risk sentiment since the Aussie was a loser, even though gold closed higher, thanks to the weaker U.S. dollar, as well as safe-haven demand for gold.

The rise in gold prices likely helped to offset some of the Aussie’s vulnerability to the risk-off vibes, though, since the Aussie was less weak compared to the Kiwi.

However, it’s worth mentioning that the prevalence of risk aversion wasn’t the only reason for the Aussie’s weakness since the Aussie also got smacked lower when Australia’s wage growth index was released since it revealed that total hourly rates of pay (excluding bonuses) only increased by 0.5% quarter-on-quarter in Q3, missing expectations for a 0.7% rise.

Year-on-year, this translates to a 2.0% increase, which is softer compared to the consensus for a 2.2% increase. However, the 2.0% reading for Q3 is actually a tick faster compared to the previous four quarters’ +1.9%. It’s also the first uptick since Q2 2014. Even so, the 2.0% annual reading is still the second poorest reading since Q2 1998, which highlights just how weak wage growth in Australia is. And that likely reinforced the idea that the RBA ain’t gonna be hiking anytime soon.

Oh, Australia also released its October jobs report. And that caused the Aussie to drop as a knee-jerk reaction because employment only saw a net increase of 3.7K in October, which is way below expectations that the Australian economy would generate between 17.5K to 18.8K jobs.

Bulls quickly jumped in, however, and the Aussie ultimately went nowhere because the other details of the jobs report were a bit more positive.

To begin with, full-time jobs actually grew by 24.3K, which marks the third consecutive month of increases in full-time employment. It just so happens that 20.7K part-time jobs got axed, which is why net employment change failed to meet expectations.

Another positive detail is that the previous month’s reading was upgraded from a net gain of 19.8K jobs to 26.6K jobs.

Also, the jobless rate ticked lower from 5.5% to 5.4%, which is the best reading since February 2013. And the jobless rate improved because the number of employed people rose as the number of unemployed Australians fell from 710K to 701K.

Admittedly, however, the fall in number of unemployed was partially due to the labor force participation rate ticking lower from 65.2% to 65.1%.

Overall, a mixed but somewhat positive jobs report, which is why there was no follow-through selling on the Aussie.

Gold was steady on that day, however, and it looks like the Aussie opted to take directional cues from gold since risk sentiment finally improved on Thursday but the Aussie traded roughly sideways, unlike the Kiwi, which was beginning to tilt to the upside at the time.

Risk aversion returned on Friday, though. And the surge in gold prices was unable to prevent the Aussie’s defenses from crumbling. But as a consolation prize of sorts, the Aussie was able to win out against the Kiwi on Friday, which saved the Aussie from the (dis)honor of being the worst-performing currency of the week.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

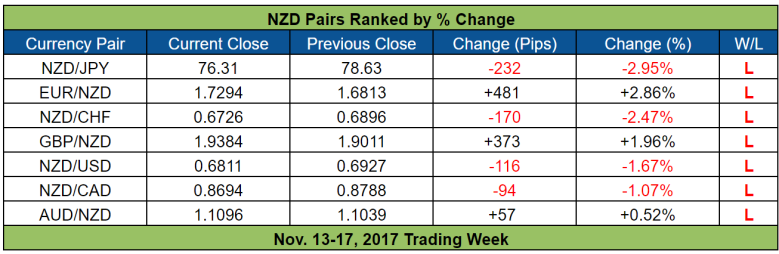

The New Zealand Dollar

The Kiwi got a mighty good whoopin’ this week, which is really great (for Kiwi bears like me). There were no major catalysts for the Kiwi this week, so like last week, the Kiwi took directional cues from risk sentiment.

The Kiwi started the trading week on a steady footing. But as noted in Monday’s morning London session recap, Kiwi bears began coming out of the woods because the risk aversion that started during the earlier Asian session intensified during the course of the London session, thanks to a string of poor earnings reports.

And risk sentiment only deteriorated further during the U.S. session because of growing doubts with regard to U.S. tax reforms, market analysts say.

Risk aversion prevailed on Tuesday, so the Kiwi got slammed by another wave of sellers. However, the Kiwi became a bit vulnerable to opposing currency price action near the end of the morning London session. Even so, the Kiwi was still down and out for the day.

Wednesday was a bit wonky since risk aversion was still the dominant sentiment during the day but the Kiwi got bid higher during the Asian and early London session. There were no apparent catalysts for the Kiwi’s strength at the time. But as noted in Wednesday’s London session recap, global bond yields got crushed, which may have given the higher-yielding Kiwi the yield advantage and attracted buyers.

Unfortunately for Kiwi bulls, all became right with the world again because the Kiwi resumed its slide on most pairs during the U.S. session.

Risk sentiment finally improved during Thursday’s morning London session, which gave the Kiwi support. The Kiwi even began trading a bit higher on some pairs. However, risk aversion made a comeback on Friday and so the Kiwi plumbed new intraweek lows, forcing Kiwi bulls to run away crying.