How y’all doing, forex buddies? New Zealand isn’t the only one that will be releasing its latest retail sales report this week since Canada will be releasing its September retail sales report tomorrow (Nov. 23, 1:30 pm GMT) .

And if you wanna get up to speed on what happened last time and what’s expected this time, then it’s time to read up on another edition of my Event Preview.

What happened last time?

- Headline retail sales m/m: -0.3% vs. +0.5% expected, +0.4% previous

- Core retail sales m/m: -0.7% vs. +0.3% expected, +0.2% previous

In my previous Event Preview for Canada’s August retail sales report, I noted that the leading and related indicators were mixed. On the one hand, Canada’s August jobs report showed that wage growth picked up the pace while the retail trade sector increased its payrolls.

But on the other hand, the August trade report hinted that demand for vehicles and general consumer goods weakened in August, which is contrary to the consensus that headline retail sales will increase at a faster pace, as well as the implied consensus that a pickup in non-vehicles sales will drive up retail sales growth and boost the core reading.

I also noted back then that historical tendencies for the headline reading were fuzzy but that the core reading had a historical tendency to print worse-than-expected readings.

As it turns out, the August retail sales report revealed that headline retail sales in Canada fell by 0.3% in August, which is in-line with the August trade report but contrary to the consensus that headline retail sales would increase 0.5% (+0.4% previous).

And a closer look at the report shows that 8 of the 11 retail store types reported declines in sales.

As such, the core reading contracted by 0.7% instead of rising by 0.3% as expected (+0.2% previous), which is also in-line with the August trade report and affirmed the historical tendency for downside surprises.

In summary, Canada’s August retail sales report was pretty bad, which is why the Loonie got dumped hard. Although Canada’s CPI report, which was released simultaneously with the retail sales report, was also pretty disappointing (+0.2% vs. +0.3% expected, +0.1% previous) and likely helped to push the Loonie lower.

What’s expected this time?

- Headline retail sales m/m: +0.9% expected vs. -0.3% previous

- Core retail sales m/m: +1.0% expected vs. -0.7% previous

For the upcoming September retail sales report, the general consensus among economists is that

Canada’s headline retail sales increased by 0.9% month-on-month after the previous months 0.3% slide. The core reading, meanwhile, is expected to rebound by a solid 1.0% after dropping by 0.7% previously.

Most analysts therefore think that consumer spending strengthened in September. Moreover, the core reading (excludes vehicles sales) is expected to outpace the headline reading (includes vehicles sales), so there is also an implied consensus that non-vehicles sales increased substantially and that vehicles sales may have weakened further.

The consensus, therefore, is that retail sales strengthened in Canada during the August period.

Okay, time to take a look at the leading and related economic indicators!

First up is Canada’s September jobs report and it shows that the wholesale and retail trade industries increased their payroll numbers by 16.6K, which is a good sign that the retail trade industry strengthened.

However, Canada’s October jobs report revealed the wholesale and retail trade industries shed 35.9K jobs in October, which could mean that the business activity weakened.

But on a more optimistic note, both the September jobs report and October jobs report showed that wage growth accelerated. Although this does not automatically mean that consumer spending also ramped up.

Next, wholesale sales in September fell by 1.2%, which is also a bad sign. Although it’s worth pointing out that weakness in the wholesale trade industry does not always lead to weakness in the retail trade industry.

Moving on to Canada’s September trade report, imports of motor vehicles and parts only increased by 0.5% after jumping by 3.1% previously. Imports of consumer goods, meanwhile, fell by 1.9% after already falling by 1.4% previously.

The leading and related economic indicators are therefore hinting that both headline and retail sales likely contracted in September, which goes against the conensus that both readings for retail sales rebounded.

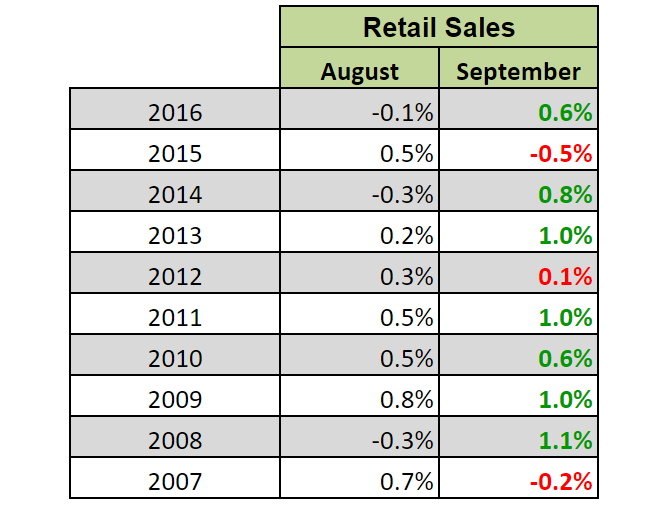

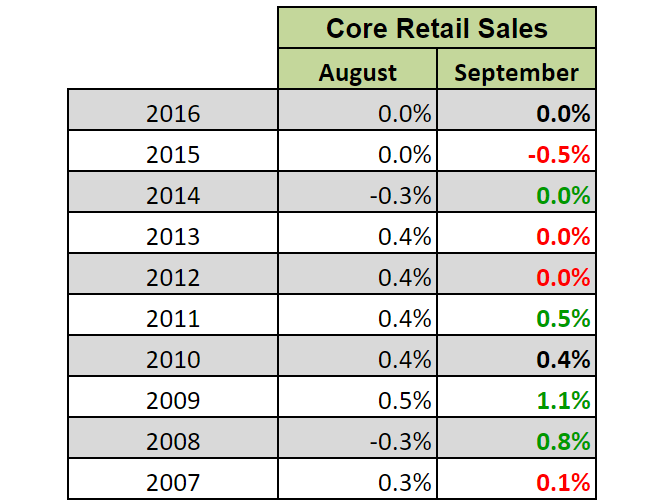

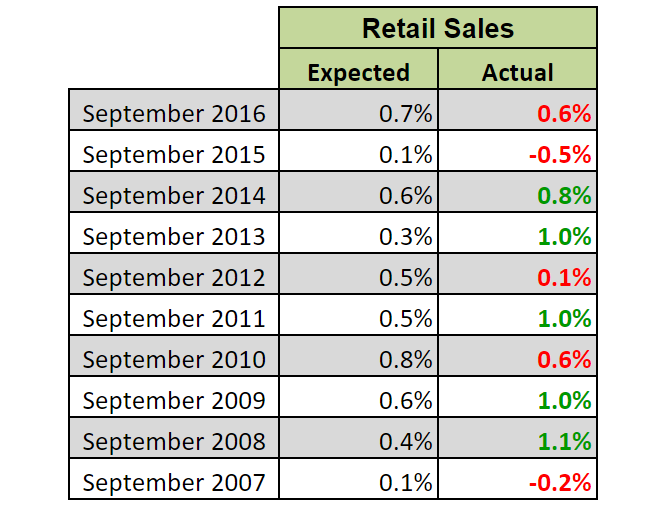

How about historical tendencies? Do they offer additional insights?

Well, looks like the consensus that headline retail sales will recover in September does have a historical basis since the headline readings for September tends to be better than the headline readings for August.

However, the same can’t be said for the consensus that the core reading will also rebound since there’s no clear historical tendency.

As for how economists did with their guesstimates, it’s a mixed bag of nuts for the headline reading since economist overshot their guesstimates half of the time in the last 10 years while undershooting their guesstimates for the other half.

However, economists clearly tend to be too optimistic when it comes to the core reading since there have far more downside surprises recently.

Final Thoughts

To summarize, the leading and related indicators are mixed once again. This time around, however, they lean more towards a possible weakness for both the headline and core readings for Canadian retail sales.

After all, higher wage growth does not necessarily lead to stronger consumer spending. And while the retail and wholesale trade industries added to their payrolls in September, they did axe more jobs in October than they added in September, which likely means that business activity wasn’t too good.

Also, the September trade report showed that imports of vehicles and parts increased at a weaker pace, which is a bad sign for the headline reading. However, the core reading also likely took a hit as well since imports of consumer goods contracted at a faster pace in September.

Finally, wholesale trade suffered in September, which may be a sign that the retail trade industry suffered as well.

As for historical tendencies, that’s also mixed since the reading for September has historically been better compared to August. However, there’s no clear pattern when it comes to how economists fared with their guesstimates for the headline reading.

Economists tend to be too optimistic when it comes to forecasting the core reading, though, which is why there are more downside surprises.

Anyhow, just keep in mind that better-than-expected readings usually trigger a quick Loonie rally while worse-than-expected readings usually lead to a quick Loonie selloff. And the Loonie’s reaction to the previous retail sales report is a classic example of the latter scenario.

But if the readings come in mixed for some reason, then forex traders usually have their sights on the core reading for the retail sales report.

Also, since this is an economic report for the Loonie, and since the Loonie has been taking directional cues from oil again, it may be prudent to keep an eye on oil prices. And if you didn’t know, you can check real-time prices of oil futures here and here.