Howdy, forex friends! We will be getting Canada retail sales and CPI reports tomorrow (Oct. 20, 12:30 pm GMT).

These are top-tier economic reports, so there’s a very good chance that the Loonie may get a volatility infusion that will allow us to pillage some quick pips from the Loonie before the weekends.

However, since the BOC statement is coming up next week, there’s also a good chance that we’ll be seeing some follow-through buying or selling. And if you need to get up to speed on what happened last time, as well as what’s expected this time around, then you better gear up by reading up on today’s write-up.

1. Canada’s Retail Sales Report (August)

What happened last time?

- Headline retail sales m/m: +0.4% vs. +0.2% expected, +0.1% previous

- Core retail sales m/m: +0.2% vs. +0.4% expected, +0.4% previous +0.7%

In last month’s write-up, I concluded that the leading and related indicators pointed to a general weakness in the retail trade industry, which will likely hit the core reading.

Moreover, I mentioned that historical tendencies were leaning more towards a downside surprise for both headline and core readings.

However, I also noted that the higher imports of passenger vehicles will likely result in a stronger headline reading.

Well, retail sales in Canada increased by 0.4% back in July, which was stronger than the consensus for a 0.2% increase.

And looking at the details of the report, the 0.8% increase in sales from motor vehicles and parts dealers drove the increase in total retail sales, which is what I mentioned in my preview.

However, vehicles sales are excluded from the core reading. And since 5 of the 10 remaining retail store types reported declines in sales, the core reading for retail sales only saw a 0.2% increase, which is a weaker growth rate compared to the consensus that the core reading would print a 0.4% rise. Not only that, the previous month’s core reading was downgraded from +0.7% to +0.4%.

In summary, Canada’s July retail sales report was mixed on the surface but the details were a tad more disappointing because the stronger headline reading was driven by vehicles sales. And vehicles sales tend to be volatile. In addition, 5 of the remaining 10 retail store types reported declines in sales, which aren’t very positive signs for stronger consumer spending in Canada.

What’s expected this time?

- Headline retail sales m/m: +0.5% expected vs. +0.4% previous

- Core retail sales m/m: +0.3% expected vs. +0.2% previous

For the this Friday’s August retail sales report, most economist forecast that total retail sales increased by 0.5%, which is a tick stronger than the previous month’s +0.4% read.

Meanwhile, the core reading is expected to come in at +0.3%, which is also faster than the previous month’s 0.2% rise.

The consensus, therefore, is that retail sales strengthened in Canada during the August period.

Moreover, there is an implied consensus that stronger non-vehicles sales would drive up retail sales since both the headline and core readings are expected to improve. And remember, vehicles sales are excluded from the core reading because of their volatility nature.

Moving on to the available leading and related economic indicators,

Looking at the available leading and related indicators,

Canada’s August jobs report reveals that the wholesale and retail trade industries shed 6.7K jobs back in August.

However, the September jobs report shows that the wholesale and retail trade industries later bumped up their payroll numbers by 16.6K jobs.

This implies that the retail and wholesale trade industries initially had a hard time and were shedding their employment numbers. However, conditions improved later and so they decided to increase their number of employees.

Of course, another possible implication is that the retail and wholesale trade industries were anticipating stronger business activity in September and October and were boosting their employment numbers, and not necessarily stronger retail and wholesale sales activity during the August period.

And while we’re talking about the jobs report, the August jobs report also revealed that average hourly earnings rebounded by 0.54% in August after contracting by 0.35% back in July, which is supportive (but not necessarily an evidence) of stronger consumer spending.

Moving on, Canada’s August trade report reveals that imports of consumer goods fell by 1.8% month-on-month in August, which is stronger drop compared to the 1.1% slide back in July. This is not really very supportive of the implies consensus that retail sales would be driven up by stronger non-vehicle sales.

Speaking of vehicles sales, the trade report also shows that imports of passenger cars and light trucks only increased by 0.1%, which is substantially weaker than the previous month’s 2.6% surge.

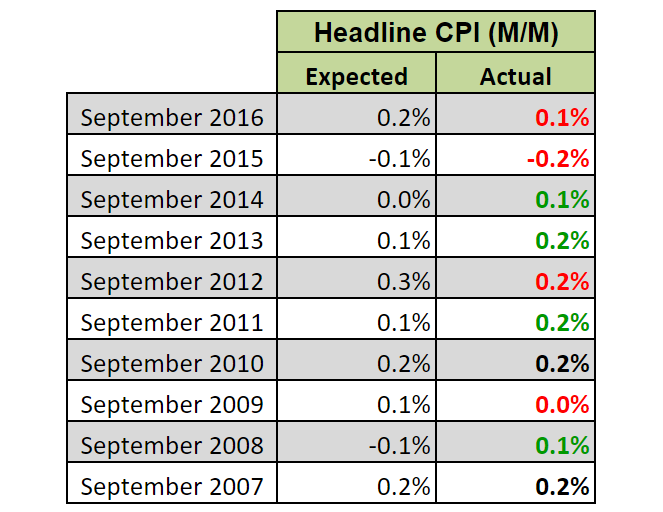

Okay, but what the historical tendencies?

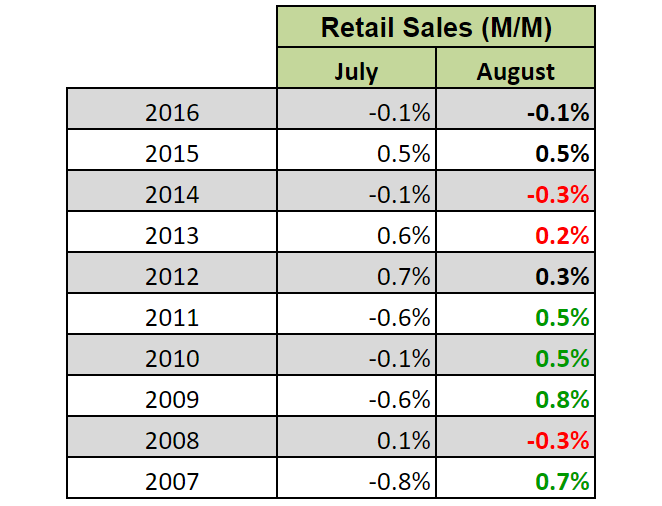

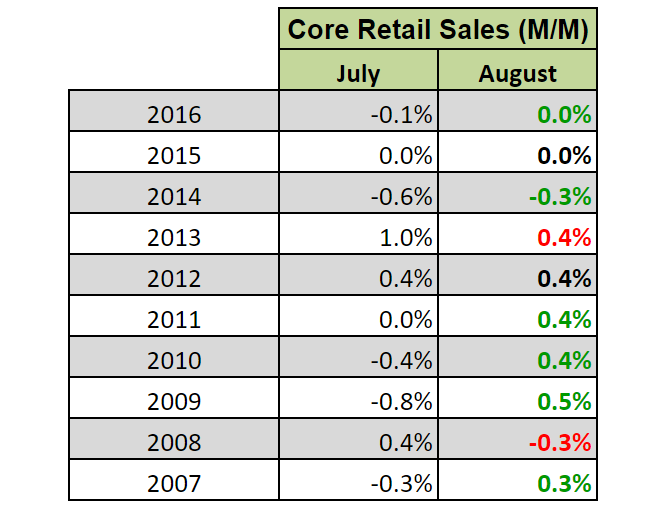

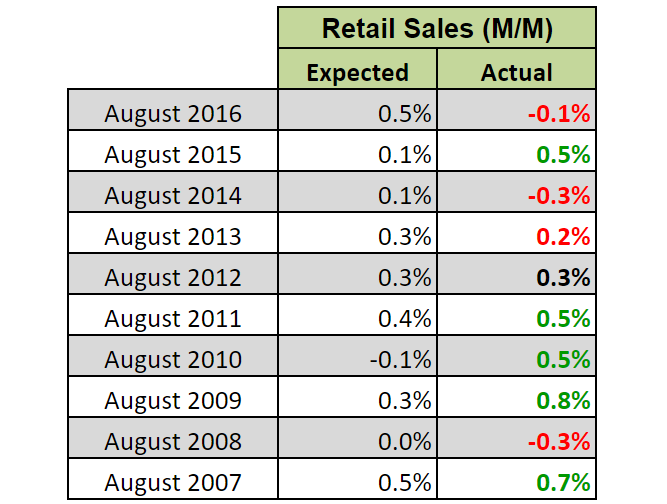

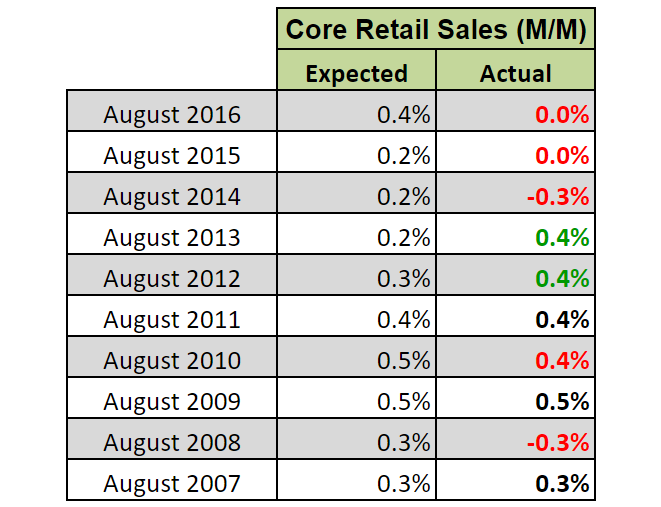

Well, the consensus that the headline and core readings will print stronger numbers compared to the previous month are in-line with historical tendencies. Although I just want to point out that the historical tendency for the headline reading has weakened in recent years, as you can see below.

As to how economists fared with their guesstimates, they have an inconsistent track record when it comes to the headline reading. However, they tend to be too optimistic and overshoot their forecasts for the core reading, resulting in more downside surprises.

To summarize, the leading and related indicators are mixed since the jobs report is pointing to the possibility of stronger business activity in the retail trade sector because of the later increase in employment, as well as the rebound in wage growth.

The trade report, meanwhile, is hinting that demand for vehicles and consumer goods in general weakened during the August period, which is contrary to the implied consensus that a pickup in non-vehicles sales will drive up retail sales growth.

Also, historical tendencies for the headline reading are fuzzy. However, the core reading usually prints a stronger reading in August compared to July. But at the same time, economist tend to be too optimistic with their forecasts, which result in more downside surprises. So probability therefore seems skewed more towards a downside surprise, at least as far as the core reading is concerned.

2. Canada’s CPI Report (September)

What happened last time?

- Headline CPI m/m: +0.1% vs. +0.2% expected, +0.0% previous

- Headline CPI y/y: +1.4% vs. +1.5% expected, +1.2% previous

- Trimmed Mean CPI y/y: +1.4% vs. +1.3% previous

- Weighted Median CPI y/y: +1.7%, same as previous

- Common Component CPI y/y: +1.5% vs. +1.4% previous

If any of you were able to read up on last month’s Canadian CPI preview, I pointed out economists tend to be too optimistic and overshoot their forecasts, which is why there are far more downside surprises than upside surprises when it comes to the monthly reading for CPI.

And as it turns out, that historical tendency was affirmed since headline CPI only increased by 0.1% in August, missing expectations for a 0.2% rise.

The year-on-year reading was also a disappointment, since it came in at +1.4%, which is a tick slower compared to the consensus for a 1.5% increase.

Despite the misses, both the monthly and annual headline readings still increased at a faster pace compared to their respective previous readings.

However, a closer look at the details reveals that the monthly reading saw a 0.1% increase after printing a flat reading previously, mainly because of the 0.4% increase in transportation costs (-0.4% previous). And the increase in transportation costs, in turn, was due to the 2.9% surge in gasoline prices (-0.6% previous).

Although the higher costs for shelter helped as well (0.2% vs. -0.1% previous).

But of the 6 remaining CPI components, 4 reported declines or weaker increases compared to the previous month.

Higher transportation costs was also the main driver for the year-on-year reading, thanks to the 8.6% surge in gasoline prices (+4.6% previous).

And of the 7 remaining CPI componets, 4 printed declines or weaker annual increases while 2 reported slightly stronger readings and 1 (shelter) maintained the previous month’s pace.

Still, two of the BOC’s preferred measures for underlying CPI printed increases.

Specifically, trimmed mean CPI ticked higher from 1.3% to a five-month high of 1.4% while common component CPI rose from 1.4% to an 11-month high of 1.5%.

As for the weighted median CPI, it held steady at 1.7%, which is the highest reading since March 2017.

Overall, the CPI report was disappointing, although some of that disappointment was offset by the fact that the BOC’s preferred measures for underlying inflation were able to print further increases.

What’s expected this time?

- Headline CPI m/m: +0.3% vs. +0.1% previous

- Headline CPI y/y: +1.7% vs. +1.4% previous

The consensus among market analysts is that headline inflation picked up the pace in September, since CPI is expected to increase by 0.3% month-on-month (+0.1% previous) and 1.7% year-on-year (+1.4% previous).

But what do the available leading indicators have to say?

Well, the prices index of the comprehensive September Ivey PMI report slumped further from 59.9 to 52.4, which means that survey respondents reported further weakness in the increase in input costs.

Markit’s manufacturing PMI report contradicts this, however, since Markit noted that “input cost inflation reached its highest level for four months in September, which manufacturers overwhelmingly linked to rising raw material prices.”

It should be pointed out, however, that Markit’s PMI report only covers the manufacturing sector, so Markit doesn’t present the complete picture of the inflation situation in Canada.

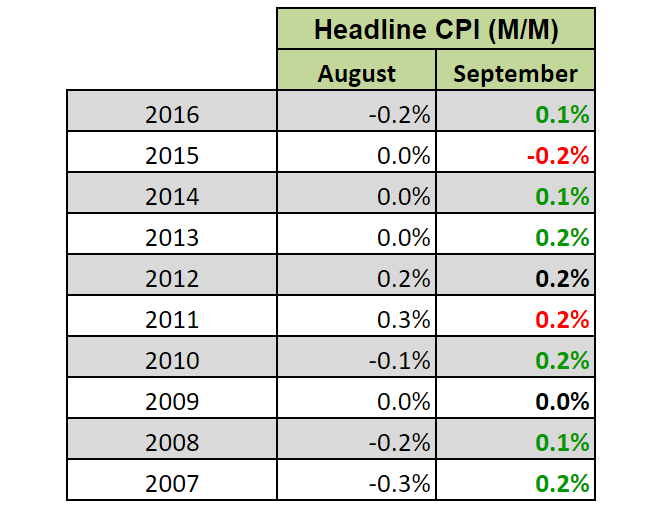

Moving on to historical tendencies, there isn’t really a historical tendency when it comes to how market analysts fared with their guesstimated for the headline month-on-month reading. And the historical data for the year-on-year reading is too limited to draw a conclusion.

However, the monthly reading has historically been stronger in September more often than not, which is in-line with consensus.

In summary, Markit and ISM are sending conflicting signals and there is no clear historical tendency, so it’s a coin toss when it comes to whether the actual reading will meet, beat, or miss expectations. However, the reading for September has historically (most of the time, not always) been better compared to the reading for August.

Final thoughts

Like last time, Canada’s retail sales and CPI reports will be released simultaneously. So if both top-tier reports beat expectations, then that would likely revive rate hike expectations and propel the Loonie higher, especially with the BOC statement coming up next week. On the flip side, a miss for both top-tier reports will likely send the Loonie lower.

And if the readings are mixed, then the CPI report usually takes precedence, with the headline month-on-month reading usually in focus.

Last month’s reaction to the mixed retail sales report and disappointing CPI report is a textbook example of this.

Overlay of CAD Pairs: 15-Minute Forex Chart

Do note, however, that the retail sales report does play a part in follow-through buying or selling, particularly the core reading for retail sales. Last month’s subsequent price action after the initial reaction is an example of this.

Although it also worth pointing out that last month’s follow-through selling was actually rather weird since two of the BOC’s three preferred measures for underlying inflation were able to print further improvements, but the Loonie didn’t seem to react to that.