Iran’s formal refusal to join ceasefire talks sent WTI crude surging nearly 7% and erased an earlier equity advance, while a hotter-than-expected New Zealand CPI print, strong U.S. retail sales data, and Kevin Warsh’s Senate confirmation hearing combined to push the U.S. dollar higher across the board.

At the Tuesday close, the greenback stood as the best-performing major currency, with gold bearing the session’s sharpest losses as rising Treasury yields and a firmer dollar unwound some of the precious metal’s recent gains.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- New Zealand NZIER Business Confidence for March 31, 2026: -4.0% (29.0% forecast; 48.0% previous)

- New Zealand CPI Growth Rate for March 31, 2026: 0.9% q/q (0.6% q/q forecast; 0.6% q/q previous); 3.1% y/y (2.8% y/y forecast; 3.1% y/y previous)

- Swiss Balance of Trade for March 2026: 2.7B (4.5B forecast; 4.4B previous)

-

U.K. Employment Change for February 2026: 25.0k (-35.0k forecast; 84.0k previous)

- U.K. Unemployment Rate for February 2026: 4.9% (5.2% forecast; 5.2% previous)

- U.K. Claimant Count Change for March 2026: 26.8k (10.0k forecast; 24.7k previous)

- U.K. Average Earnings incl. Bonus (3Mo/Yr) for February 2026: 3.8% (3.7% forecast; 3.9% previous)

- Germany ZEW Economic Sentiment Index for April 2026: -17.2 (-10.0 forecast; -0.5 previous)

- Euro area ZEW Economic Sentiment Index for April 2026: -20.4 (-16.0 forecast; -8.5 previous)

- U.S. Retail Sales for March 2026: 1.7% m/m (1.1% m/m forecast; -0.2% m/m previous); 4.0% y/y (2.4% y/y forecast; 3.7% y/y previous)

- U.S. Pending Home Sales for March 2026: 1.5% m/m (0.5% m/m forecast; 1.8% m/m previous); -1.1% y/y (0.7% y/y forecast; -0.8% y/y previous)

- Kevin Warsh, Trump’s Fed Chair nominee, pledged independence before the Senate Banking Committee during his confirmation hearing but deliberately avoided near-term rate guidance; called for a new framework for dealing with persistent inflation; said Trump never asked him to commit to a specific rate decision; confirmed he would sell undisclosed assets before being sworn in

-

Geopolitical updates:

- Iran informed the U.S. that it would not attend ceasefire talks slated for Wednesday in Islamabad

- Parliament Speaker Ghalibaf said Tehran would not accept negotiations “under the shadow of threats”

- VP Vance called off his planned trip to Islamabad

Promoted: Day traders & Scalpers have better odds of making great decisions if they see market catalysts right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

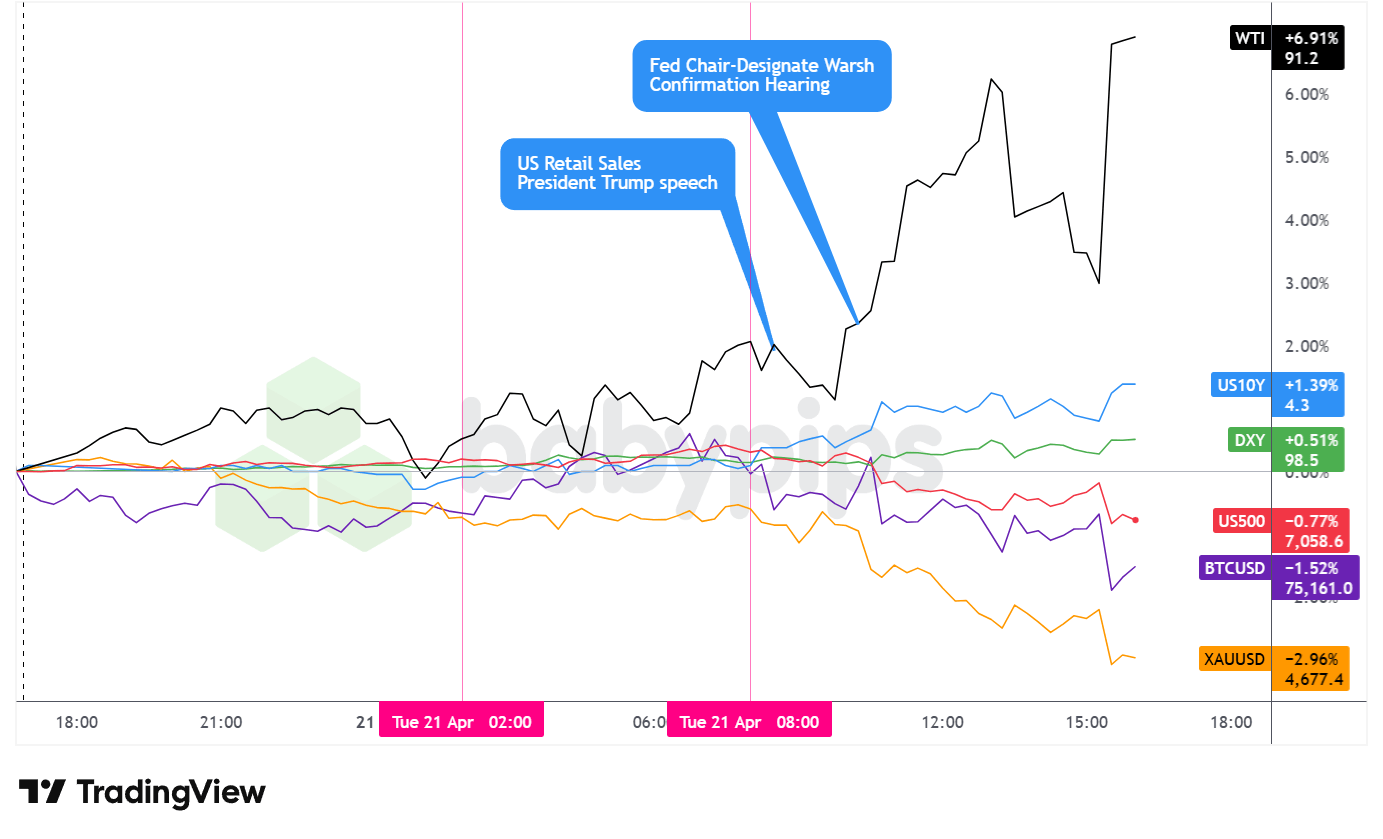

Broad Market Price Action:

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Tuesday’s session was shaped almost entirely by escalating U.S.-Iran diplomatic uncertainty. Equities erased what had been a record-pacing advance as Iran’s formal refusal to send a delegation to Islamabad crossed newswires, crude oil surged to multi-week highs, Treasury yields climbed, and gold sold off sharply despite the intensifying geopolitical backdrop.

WTI crude oil was the session’s dominant story, surging 6.89% to close at $91.18 per barrel. Crude had traded in a relatively contained range through the Asian and London sessions, hovering in the mid-to-upper $80s, before launching higher once U.S. trading got underway and reports confirmed Iran would not attend talks. Brent crude briefly topped $100 per barrel intraday. The Strait of Hormuz has remained effectively closed to most commercial traffic since the start of the conflict in late February, and commodity analysts have warned that an extended stalemate could push markets toward depleted stockpile levels within weeks if flows do not resume.

The S&P 500 declined 0.74% to close at 7,060.7. The index had been on pace for a record close earlier in the session, reaching approximately 7,146 during the London session, before reversing sharply as Iran-related headlines hit. The sell-off accelerated into the close, with the index surrendering roughly 85 points from its intraday peak. Kevin Warsh’s confirmation hearing commentary — specifically his call for a new inflation framework and his historically hawkish stance on Fed balance sheet reduction — appeared to generate some additional headwind for equities during the U.S. afternoon, though the Iran headlines likely drove the bulk of the directional move.

Gold fell sharply, declining 2.98% to close at $4,676.9 per ounce. The precious metal had already been under pressure from the Asian session open, trading down from prior-session highs near $4,833, with selling extending through both the London and U.S. sessions. The decline possibly reflected a combination of rising Treasury yields reducing the opportunity cost of holding non-yielding bullion, a notably stronger U.S. dollar, and potential profit-taking following gold’s extended rebound since March lows.

Bitcoin declined 1.63% to close at $75,071.26. The cryptocurrency climbed to approximately $76,800 during the early London session before gradually retreating through the U.S. hours. No direct crypto-specific catalyst appeared to drive the move; the decline likely reflected broader risk-off sentiment as surging oil prices raised concerns about inflation persistence and dampened appetite for speculative assets.

The 10-year U.S. Treasury yield rose 1.10% to close at 4.30%. Yields climbed steadily from the U.S. session open, with the move appearing to correlate with Warsh’s confirmation hearing — where commentary about regime change at the Fed, a new inflation framework, and balance sheet reduction appeared to weigh on Treasuries — and with higher oil prices feeding near-term inflation expectations. Multiple newswire reports noted that a strong U.S. retail sales print contributed to traders scaling back rate-cut expectations during the session, adding further upside pressure to yields.

Promoted: Pay Once. Trade Forever.

Most prop firms quietly drain your account with monthly subscription fees long before you ever see a payout. Tradeify operates differently — evaluations are a one-time purchase with no recurring charges. Pass the eval, get activated instantly, and keep more of what you earn. With ~$150M in verified payouts and growing, the math speaks for itself.

Learn More About Tradeify!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

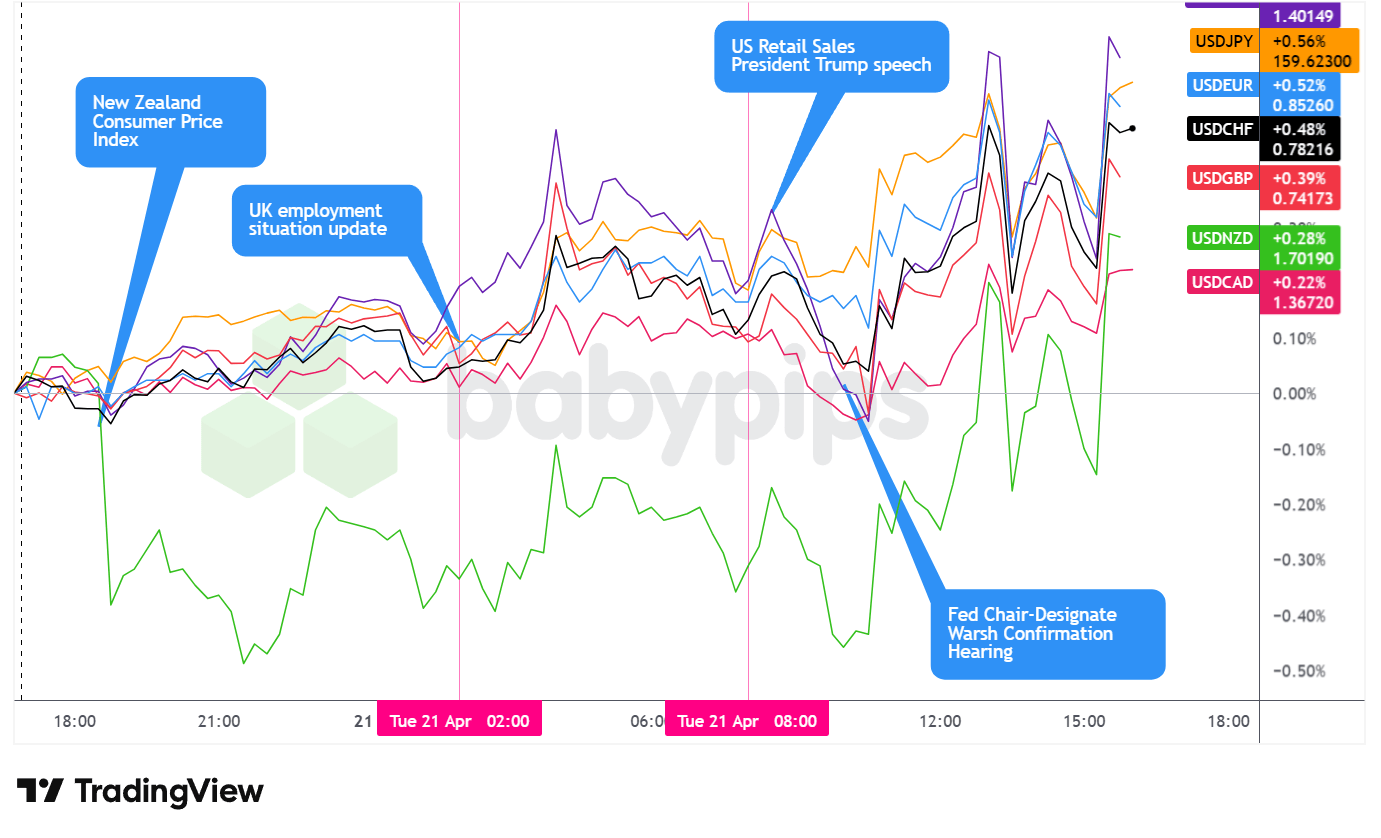

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar closed Tuesday as the best-performing major currency on a daily basis, with the DXY finishing at 98.53, up approximately 0.50%, and the greenback posting consistent gains across all tracked pairs.

During the Asian session, the dollar traded with mostly low volatility and a net bullish lean against the major currencies. The main outlier was the New Zealand dollar, which reacted directly to New Zealand’s Q1 2026 CPI report. The data showed annual inflation holding at 3.1%, above both the 2.9% forecast and the RBNZ’s own projection, while the quarterly print of 0.9% also beat the 0.8% consensus. The hotter-than-expected result lifted market pricing for a May RBNZ rate hike to approximately 42% from below 30% the prior day, contributing to NZD volatility that stood apart from the otherwise low-key Asian session tone. Notably, Stats NZ flagged that the full pass-through from the Middle East conflict on petrol and transport costs has only begun to filter through, suggesting inflation pressures could remain elevated well into 2026. Elsewhere, the broader dollar bid appeared to reflect cautious pre-positioning ahead of U.S. catalysts and ongoing uncertainty around the Iran ceasefire deadline.

During the London session, the dollar continued to see a bullish bias that was quickly capped, and the greenback pulled back against the major currencies heading into the U.S. session open. The UK employment report offered a mixed picture: the ILO unemployment rate came in at 4.9%, well below the 5.2% forecast and slightly above the prior 5.0%, pointing to underlying labor market resilience that arguably reduces urgency for Bank of England rate cuts in the near term. German ZEW economic sentiment collapsed to -17.2 in April, far below the -5.0 consensus and the lowest reading since late 2022, with the shortfall likely reflecting the growing drag from the U.S.-Iran conflict on German investor morale, via higher energy costs and weaker growth expectations. ECB’s de Guindos reinforced a cautious tone, explicitly calling on the central bank to keep a cool head on rates given geopolitical uncertainty.

After the U.S. session opened, the dollar dipped briefly before rebounding to trade with a net bullish lean heading into the daily close. A strong U.S. retail sales print likely prompted traders to scale back rate-cut expectations and pushing the policy-sensitive 2-year Treasury yield up as much as seven basis points to 3.79%, likely reinforced the dollar’s renewed bid.

The Warsh confirmation hearing added a layer of hawkish undertone to the session, with the nominee calling for a new inflation framework and warning that the Fed’s balance sheet remains too large — commentary that appeared to reinforce a higher-for-longer rate narrative despite his avoidance of near-term rate guidance.

Iran’s formal refusal to attend peace talks, which accelerated the surge in oil prices, may have also contributed to broad safe-haven flows into the greenback during the afternoon.

Upcoming Potential Catalysts on the Economic Calendar

- US-Iran ceasefire deadline: Trump extended the original Tuesday deadline to Wednesday midnight U.S. time, allowing an extra 24 hours for potential talks in Islamabad; any breakthrough or breakdown in negotiations could generate significant moves across crude oil, equities, and FX — particularly pairs involving the yen, franc, and commodity-linked currencies

- Japan Balance of Trade for March 2026 at 11:50 pm GMT

- Australia Westpac Leading Index MoM for March 2026 at 1:00 am GMT

- U.K. Inflation Updates for March 2026 at 6:00 am GMT

- Euro area ECB Lane Speech at 7:40 am GMT

- U.S. MBA 30-Year Mortgage Rate & Mortgage Applications for April 17, 2026 at 11:00 am GMT

- Canada New Housing Price Index for March 2026 at 12:30 pm GMT

- ECB Lane Speech at 1:15 pm GMT

- Euro area Consumer Confidence Flash for April 2026 at 2:00 pm GMT

- U.S. EIA Crude Oil Stocks Change for April 17, 2026 at 2:30 pm GMT

- ECB President Lagarde Speech at 5:30 pm GMT

Markets enter Wednesday in a state of elevated uncertainty, with the single most important variable being whether US-Iran negotiations materialize before the revised ceasefire deadline. A deal that reopens the Strait of Hormuz would likely trigger a sharp reversal in crude oil, a relief rally in equities, and renewed pressure on safe-haven currencies and the dollar. A breakdown — or further extension of the deadline — would likely sustain the current dynamic of elevated oil, softer risk assets, and a bid dollar.

Stay frosty out there, forex friends!

Promoted: How Do Professionals Trade Geopolitical News?

You’ve seen the retail reaction to the geopolitical whiplash—now see the institutional one. Brent Donnelly’s “The Art of Currency Trading” (4.7 stars & 517 reviews on Amazon) bridges the gap between the news headlines you read and the execution on your screen. It’s a practical, “no-fluff” guide to how professional FX desks navigate the exact type of geopolitical volatility described in today’s recap.

Learn more about “The Art of Currency Trading” at Amazon

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.