New Zealand’s annual inflation held steady at 3.1% in Q1 2026, unchanged from the prior quarter but coming in hotter than the 2.9% forecast.

On a quarterly basis, price growth picked up to 0.9% from 0.6%, driven mainly by higher petrol and pharmaceutical costs.

That keeps inflation hovering just above the Reserve Bank of New Zealand’s (RBNZ) 1 to 3% target band and adds a bit of pressure on the central bank. It also nudges expectations toward an earlier interest rate hike, as markets start to question how long policymakers can stay patient.

Key Takeaways

- Annual CPI held at 3.1% y/y in Q1 2026, unchanged from Q4 2025 and above the 2.9% market forecast. Quarterly CPI rose 0.9%, beating both the 0.8% consensus and the RBNZ’s own projection. (Stats NZ Q1 2026 CPI)

- Electricity was the largest annual contributor for the third consecutive quarter, surging 12.5% year-over-year and accounting for more than a tenth of the 3.1% annual rate.

- Petrol prices were the biggest quarterly driver, rising 3.5% in Q1 after falling in January and February before climbing in March. Pharmaceutical prices jumped 17.7% in the quarter due to higher prescription charges.

- Rents rose just 1.2% annually — the smallest increase in 16 years — while lower international airfares (-7.0%) and cheaper milk, cheese and eggs (-2.0%) provided partial offsets.

- Non-tradeable (domestic) inflation rose 3.5% annually; tradeable (imported) inflation came in at 2.5%. Underlying inflation measures pointed to an annual rate of around 2.2–2.5%.

- The RBNZ held its Official Cash Rate at 2.25% in April and had forecast Q1 CPI at 3.0%. The hotter-than-expected result lifted the implied probability of a May rate hike to 42%, from under 30% the day prior.

Link to official Stats NZ Quarterly CPI (Q1 2026)

Electricity was the main driver for the third straight quarter, jumping 12.5% and making up more than a tenth of the headline print, while local rates and meat prices also pushed higher. Meanwhile, rents barely budged, rising just 1.2%, the slowest pace in 16 years.

Petrol and pharmaceuticals also did a lot of the heavy lifting. Petrol rose 3.5% while pharmaceutical prices surged 17.7%, together accounting for more than a quarter of the quarterly increase, though cheaper international airfares helped take a bit of the edge off.

What matters for traders is what is not fully in the data yet. Stats NZ made it clear the Middle East conflict has only started to filter through, meaning the bigger wave of oil and transport cost pressures is likely still ahead. That lines up with expectations that inflation could stay above target for longer, potentially delaying a return to the 1 to 3% range until mid 2027.

Markets are already adjusting. Pricing now leans toward around three OCR hikes to 3.0% by year end, with the odds of a move as soon as May jumping to 42% from below 30% just a day earlier.

Market Reactions

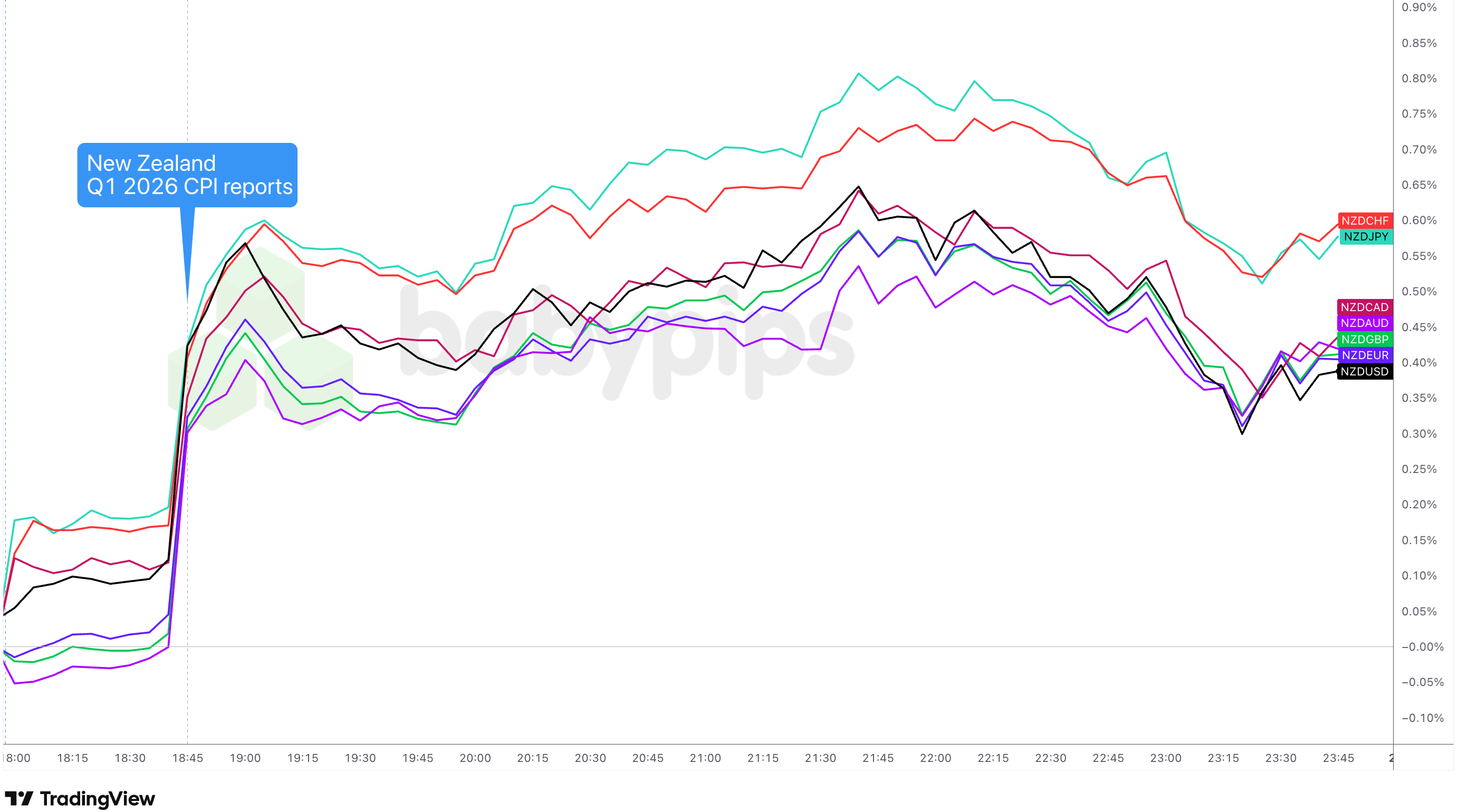

New Zealand Dollar vs. Major Currencies: 5-min

NZD vs. Major Currencies 5-min Forex – Chart Faster with TradingView

After a quick pullback, buyers stepped back in and kept NZD climbing into the close, with the biggest gains against the Swiss franc and yen as safe-haven trades unwound, while moves against other majors were more modest.

With inflation still above target and the full oil shock yet to hit, the RBNZ may not have much time to wait. Markets are already pulling forward hike expectations, so attention now turns to Q2 inflation. A move toward the RBNZ’s 4.2% forecast would likely lock in a June hike and keep NZD supported.

Promoted: Fast markets are stressful enough. Don’t let account access be the weak link.

NZD surged after a hotter-than-expected CPI print pushed rate hike expectations higher, with traders scrambling to react in real time. The last thing you need in moments like this is a login issue or a compromised account.

Secure Your Accounts with LastPass Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.