Markets surged Wednesday as a US-Iran ceasefire agreement sparked a massive risk rally, with oil plunging over 17% and equities erasing much of March’s decline, though doubts emerged about the durability of the truce amid conflicting terms and ongoing regional strikes.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Early in the Asia session, the United States and Iran agreed on a two-week ceasefire brokered by Pakistan

- U.S. API Crude Oil Stock Change for April 3, 2026: 3.72M (10.26M previous)

- Japan Overtime Pay for February 2026: 3.3% y/y (1.3% y/y forecast; 3.3% y/y previous)

- Japan Average Cash Earnings for February 2026: 3.3% y/y (2.5% y/y forecast; 3.0% y/y previous)

- Japan Current Account for February 2026: 3,933.0B (4,100.0B forecast; 941.6B previous)

- New Zealand RBNZ Interest Rate Decision for April 8, 2026: 2.25% (2.25% forecast; 2.25% previous)

- Japan Eco Watchers Survey Outlook for March 2026: 38.7 (49.2 forecast; 50.0 previous)

- Germany Factory Orders for February 2026: 0.9% m/m (5.7% m/m forecast; -11.1% m/m previous)

- U.K. Halifax House Price Index for March 2026: -0.5% m/m (0.3% m/m forecast; 0.3% m/m previous); 0.8% y/y (1.3% y/y forecast; 1.3% y/y previous)

- Swiss Unemployment Rate for March 2026: 3.1% (3.2% forecast; 3.2% previous)

- Euro area PPI for February 2026: -0.7% m/m (-0.6% m/m forecast; 0.7% m/m previous); -3.0% y/y (-2.9% y/y forecast; -2.1% y/y previous)

- Euro area Retail Sales for February 2026: -0.2% m/m (-0.1% m/m forecast; -0.1% m/m previous); 1.7% y/y (1.8% y/y forecast; 2.0% y/y previous)

- U.S. MBA 30-Year Mortgage Rate for April 3, 2026: 6.51% (6.57% previous)

- U.S. MBA Mortgage Applications for April 3, 2026: -0.8% (-10.4% previous)

- U.S. EIA Crude Oil Stocks Change for April 3, 2026: 3.08M (5.45M previous)

- Iran officials see Israeli’s strikes in Lebanon as violating the terms of the ceasefire

- The FOMC meeting minutes showed that officials raised their 2026 inflation outlook, noted uncertainty from Middle East developments, and showed a shift in risks toward persistent inflation over employment concerns, with projections indicating one rate cut this year.

Promotion: Use TradeZella’s AI Powered trade journal to deep-dive into your execution and see exactly how you performed during today’s trading session.

Click here to get the TradeZella Edge and use code PIPS20 to save 20% on your first purchase!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

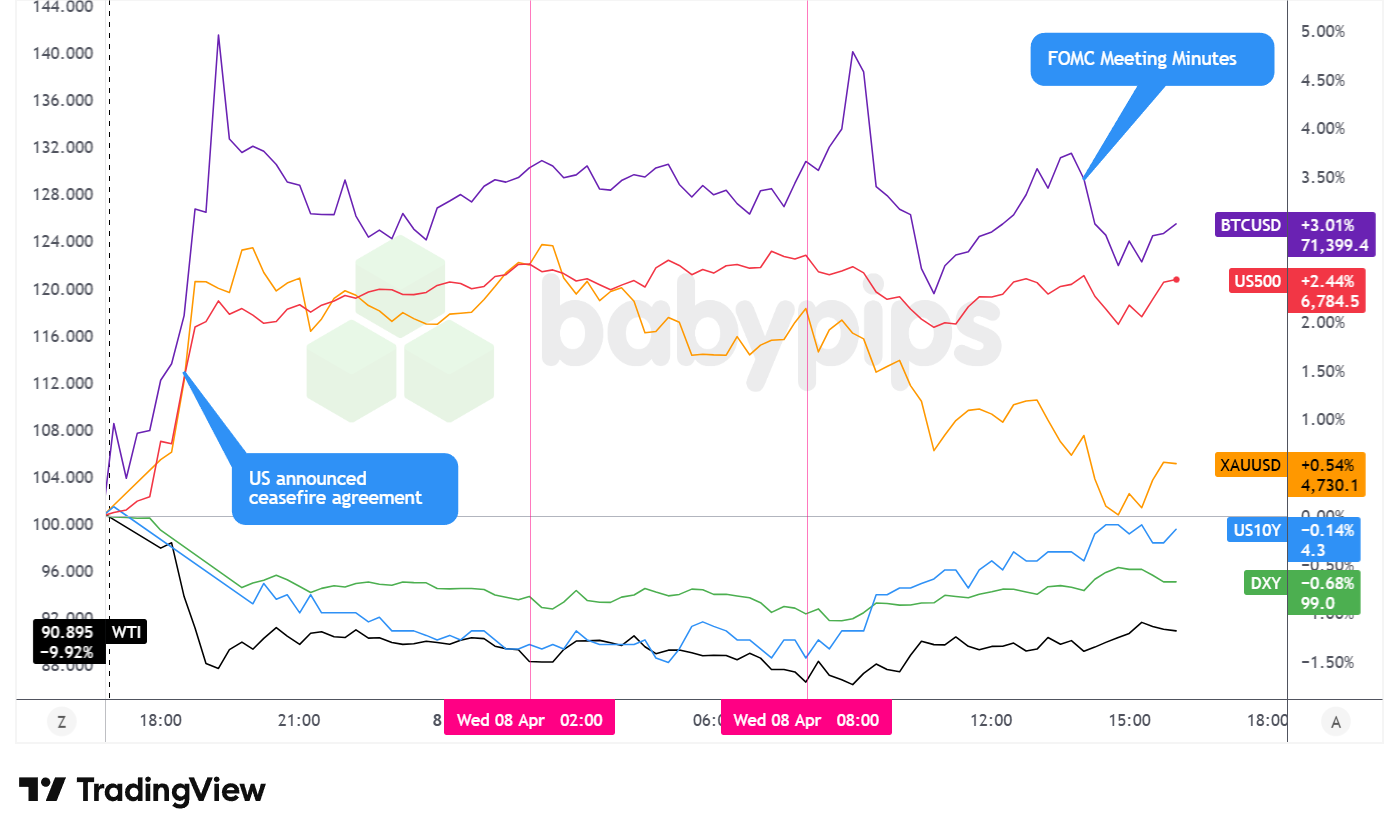

Broad Market Price Action:

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Wednesday’s session delivered a textbook risk-on surge as markets embraced the ceasefire announcement between the US and Iran, with investors prioritizing the immediate de-escalation signal over the substantial uncertainties surrounding implementation.

US equities rallied sharply, with the S&P 500 advancing 2.44% to close around 6,784.5, nearly erasing March’s losses. The index surged immediately following President Trump’s ceasefire announcement late Tuesday, with the rally extending through the Wednesday session despite intermittent volatility. Technology shares led the advance, while defensive sectors lagged, reflecting a clear rotation into cyclical risk assets. The move appeared to correlate primarily with reduced tail-risk premium from the Middle East conflict, though significant questions remained about the durability of the truce given conflicting statements from US, Iranian, and Israeli officials.

WTI crude oil suffered a historic decline, plummeting 9.92% to close around 90.895 per barrel after falling as much as 17% intraday. The dramatic selloff began immediately after Trump’s ceasefire announcement and accelerated through the Asian and London sessions. However, the move appeared to reflect optimism about eventual Strait of Hormuz reopening rather than immediate supply relief, as unconfirmed reports later suggested Iran may limit passage to just 10-15 vessels per day during the ceasefire period. If accurate, this would represent minimal improvement from current flow levels and leave roughly 800 stranded vessels in the Gulf with limited near-term exit options. Oil pared some losses during the US afternoon, possibly as traders reassessed the gap between ceasefire rhetoric and logistical reality, or off reports of ceasefire violations.

Gold climbed 0.54% to settle near 4,730.1, rallying alongside risk assets in an unusual simultaneous advance. The precious metal strengthened quickly through the Asian session before consolidating and pulling back during London and US trade. The move likely reflected a combination of factors including safe-haven demand persisting amid regional uncertainty, inflationary concerns from elevated oil prices despite Wednesday’s decline, and positioning ahead of upcoming US inflation data.

Bitcoin surged 3.01% to trade around 71,399.4, extending recent gains as the cryptocurrency benefited from the broad risk rally. The advance appeared to correlate with improved risk sentiment and declining safe-haven dollar demand, though Bitcoin’s outperformance relative to traditional equities suggested crypto-specific momentum may have also contributed.

Treasury yields fell 0.14% to approximately 4.3 on the 10-year note, with the decline likely reflecting a combination of safe-haven unwinding and expectations that lower oil prices could ease inflation pressures and preserve space for Fed rate cuts. The FOMC minutes released at 2:00 pm ET showed most officials worried a protracted war could hurt the labor market and warrant lower rates, while many policymakers highlighted upside inflation risks.

Promoted: Your Edge Is Already Proven. Skip the Evaluation.

If you’ve been journaling your results and the data is there, why spend weeks re-proving it to a prop firm? Tradeify’s Lightning accounts offer instant funding — no evaluation phase, no waiting, just capital. Trade the setups you’ve already mastered, with the account size they deserve.

Get Instant Funding with Tradeify!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

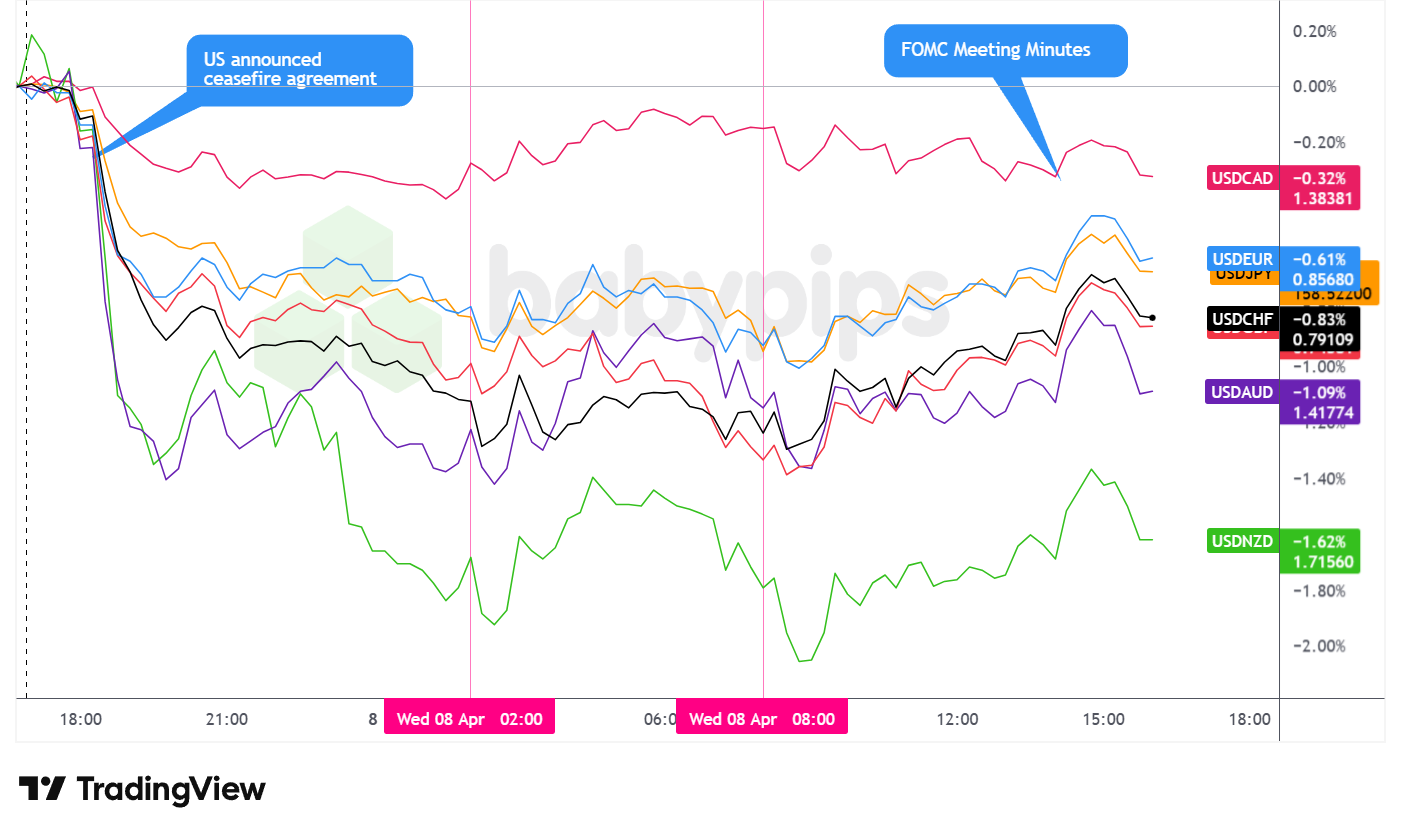

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The US dollar traded with pronounced volatility Wednesday, ultimately closing as the weakest major currency as safe-haven demand evaporated following the US-Iran ceasefire announcement.

During the Asian session, the dollar fell against the major currencies. The greenback weakened sharply in the immediate aftermath of Trump’s late-Tuesday ceasefire announcement, with the selling pressure extending through Asian trading hours. Markets appeared to price out war premium from the dollar, with the move likely reflecting reduced tail-risk scenarios and expectations that lower oil prices could preserve Fed rate-cutting flexibility. The Reserve Bank of New Zealand’s decision to hold rates at 2.25% as expected provided limited volatility to the kiwi, with Governor Breman acknowledging the oil shock has lifted inflation risks while weak growth tempers the response.

The London session brought choppy trading as the dollar rebounded and then pulled back against the major currencies. European data came in mostly in line with expectations, with eurozone PPI declining 0.7% month-over-month as forecast and retail sales falling 0.2% versus expectations of -0.1%. Germany’s factory orders provided a rare positive surprise, rising 0.9% versus the -11.1% prior decline, though this failed to generate sustained euro strength. UK construction PMI and housing data disappointed, yet sterling held relatively firm, possibly reflecting market focus on the broader geopolitical de-escalation rather than domestic fundamentals. The dollar’s choppy behavior likely reflected conflicting signals as traders weighed the ceasefire optimism against emerging questions about implementation details and reports that Israel’s Lebanon operations would continue.

After the US session opened, the dollar dipped and then rebounded against the major currencies, but pulled back just ahead of the Wednesday close. The FOMC minutes release at 2:00 pm ET showed divided views among policymakers, with some emphasizing inflation risks while others focused on labor market vulnerabilities, though the overall tone suggested the Fed would look through temporary oil-driven price spikes if the conflict de-escalates. The dollar’s late-session weakness possibly reflected profit-taking on safe-haven positions as traders reassessed the balance of risks.

Upcoming Potential Catalysts on the Economic Calendar

- Japan Consumer Confidence for March 2026 at 5:00 am GMT

- Germany Balance of Trade for February 2026 at 6:00 am GMT

- Germany Industrial Production for February 2026 at 6:00 am GMT

- Japan Machine Tool Orders for March 2026 at 6:00 am GMT

- U.K. BBA Mortgage Rate for March 2026 at 9:00 am GMT

- U.S. Initial Jobless Claims for April 4, 2026 at 12:30 pm GMT

- U.S. GDP Growth Rate Final for December 31, 2025 at 12:30 pm GMT

- U.S. Core PCE Price Index for February 2026 at 12:30 pm GMT

- U.S. Wholesale Inventories for February 2026 at 2:00 pm GMT

- U.S. Fed Balance Sheet for April 8, 2026 at 8:30 pm GMT

Thursday’s calendar features US inflation data that could influence Federal Reserve rate cut expectations following Wednesday’s massive oil price decline, with the Core PCE Price Index representing the Fed’s preferred inflation gauge. Initial jobless claims will provide insight into whether the oil shock and geopolitical uncertainty are beginning to affect labor market conditions, while the final Q4 GDP revision offers a retrospective view of economic momentum before the Middle East conflict escalated.

German industrial production data may shed light on whether Europe’s manufacturing sector is stabilizing or continuing to struggle, with particular attention on any impact from supply chain disruptions related to Middle East tensions. The combination of inflation and labor market data during the US session could generate significant volatility if the figures suggest the Fed faces a more difficult trade-off between price stability and employment objectives than currently priced by markets.

Markets remain highly sensitive to any fresh developments on the US-Iran ceasefire implementation, particularly regarding Strait of Hormuz vessel passage and whether unconfirmed reports of 10-15 ship daily limits prove accurate, as this would suggest minimal near-term relief for the roughly 800 vessels currently stranded in the Gulf.

Stay frosty out there, forex friends!

Promoted: How Do Professionals Trade Geopolitical News?

You’ve seen the retail reaction to the ceasefire announcement—now see the institutional one. Brent Donnelly’s “The Art of Currency Trading” (⭐ 4.7★ | 500+ reviews on Amazon) bridges the gap between the news headlines you read and the execution on your screen. It’s a practical, “no-fluff” guide to how professional FX desks navigate the exact type of geopolitical volatility described in today’s recap.

Learn more about “The Art of Currency Trading” at Amazon

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.