The U.S. advance Q1 2026 GDP missed expectations at 2.0% while core PCE inflation surged to 3.2% annually, a combination that sent the dollar sharply lower across the board and reinforced the case for the Fed to stay on hold.

Key Takeaways

- Q1 2026 Real GDP rose 2.0% annualized (q/q), up from 0.5% in Q4 2025 but below consensus expectations at 2.2%.

- Imports surged 21.4%, subtracting roughly 1.3 percentage points from GDP on a likely front-running of tariffs as businesses rushed to bring goods into the country ahead of further levies.

- Non-residential fixed investment surged 10.4%, led by a 17.2% jump in equipment spending and a 13.0% rise in intellectual property products, reflecting the ongoing AI investment boom.

- Real consumer spending grew 1.6%, down from 1.9% in Q4, with services leading the way while goods spending slowed.

- The core PCE measure rose 4.3% versus 2.7% in Q4; Monthly core PCE rose 0.3% in March (down from 0.4% in February) in line with forecasts but well above the Fed’s target

- Personal spending jumped 0.9% in March, right in line with consensus, supported by strong motor vehicle (+2.4%) and food purchases. Real spending rose a more modest 0.2% after adjusting for inflation.

- Personal income rose 0.6%: This was an above-expectations gain and bodes well for Q2 consumer spending — though real disposable income ticked down 0.1% after accounting for the inflation spike.

On one hand, the surge in March core PCE could be partly explained by front-loading behavior ahead of tariff escalation and war-related uncertainty, with gasoline prices jumping sharply and goods inflation doubling, rather than persistent domestic demand-driven price pressure.

On the other hand, the declining savings rate and resilient consumer spending suggest that households are not yet pulling back meaningfully, even as real wages are being eroded by inflation.

However, it’s worth noting that the personal saving rate fell to 3.6% in March from 3.9% in February and 4.5% in January, suggesting that consumers may be burning through their buffers to maintain spending levels amid rising prices.

Link to official U.S. Personal Income and Outlays (March 2026)

Meanwhile, the surge in imports that weighed on Q1 GDP is widely expected to reverse as businesses adjust to the new tariff regime, which could see growth rebound in Q2. But if inflation remains elevated as those import distortions unwind, the Fed faces a genuine bind: growth recovering while price pressures persist would argue strongly for rates staying higher for longer.

Promoted: Day traders & Scalpers have better odds of making great decisions if they see market catalysts right away, including comments from government officials like situation we saw today in Japan. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

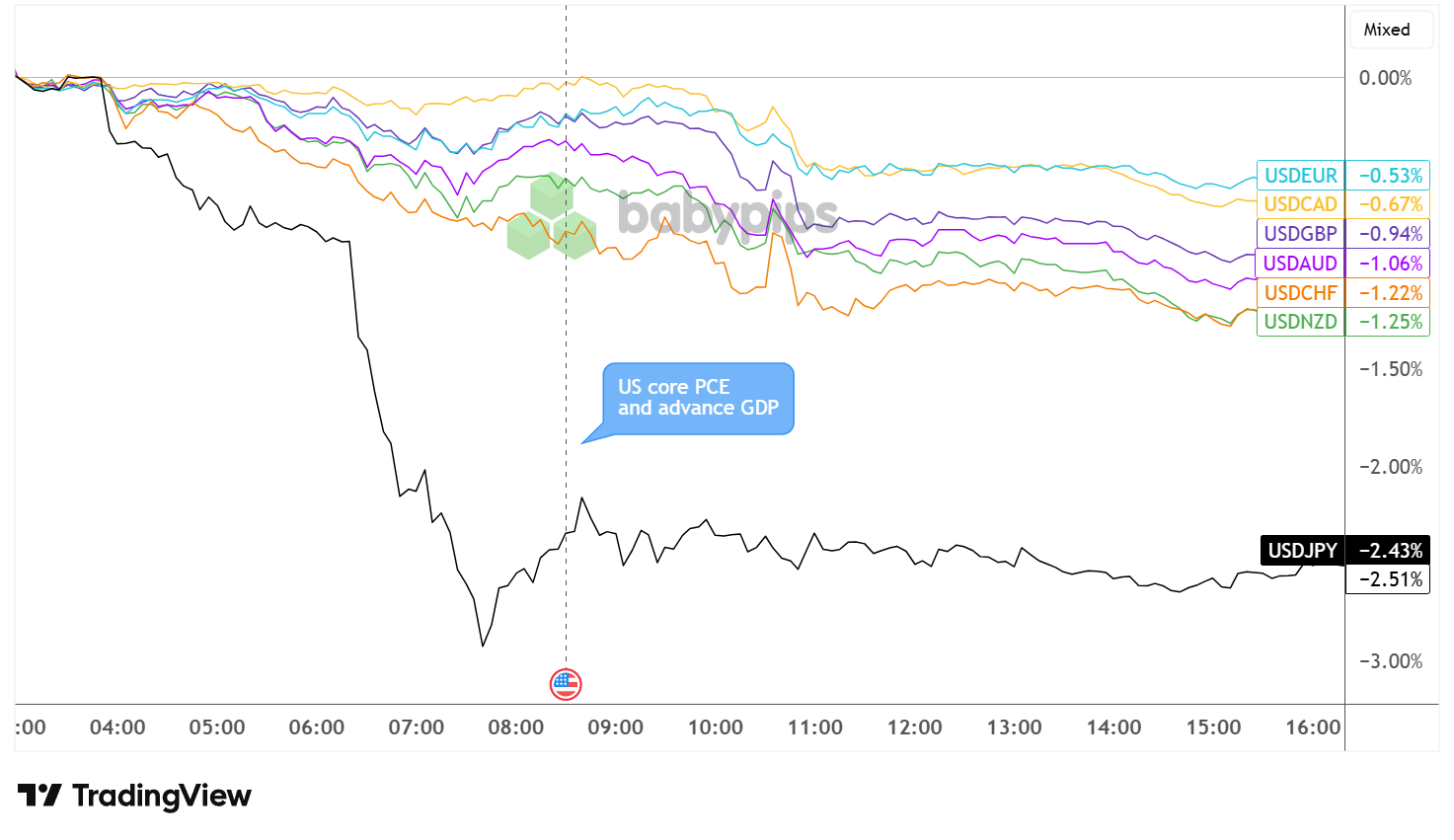

Market Reaction

U.S. Dollar vs. Major Currencies: 5-min Overlay

USD vs. Major Currencies 5-min Forex Chart Faster with TradingView

The U.S. dollar, which had already been edging lower leading up to the core PCE and advance GDP release, had a net bearish reaction to the numbers.

With the exception of USD/JPY, which had been in the middle of a pullback from a steep decline on JPY intervention threats, the majority of dollar pairs continued their southbound trajectory after the U.S. reports reinforced stagflation fears.

The Greenback sustained its declines as the New York session progressed, likely as traders cemented expectations of the Fed sitting on its hands for much longer, deepening its losses to JPY (2.51%), NZD (-1.25%), and CHF (-1.22%) by session’s end. USD appeared to limit its declines against EUR (-0.53%) and CAD (-0.67%) as consolidation took place towards the close.

Promoted: Capitalize on USD Volatility Without Risking Your Own Funds.

The U.S. dollar took some hits as the combination of higher core PCE inflationary pressures and a downbeat quarterly GDP highlighted stagflationary pressures. When the macroeconomic data shifts this fast, trading the volatility requires deep focus—and enough capital to make your edge count.

If you have the right fundamental bias but a restrictive personal account size, Funded Trading Plus can help. They offer evaluation packages starting at just $89.00. Prove your skills with simple, fair rules, and you can double your account every 10% up to $2,500,000.

Learn more about Funded Trading Plus!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.