The U.S. economy added just 57,000 jobs in June, badly missing forecasts near 110,000.

On its own, that would be enough to shake up rate expectations. But the report arrived one day after Fed Chair Kevin Warsh, in his international debut at the ECB’s Sintra forum, sidestepped questions about a July hike, and it followed a softer manufacturing report earlier the same week.

Together, the three events reshape how traders should think about the next several months of Fed policy.

What Did June’s Jobs Report Actually Show?

Nonfarm payrolls (NFP), the Bureau of Labor Statistics’ monthly count of jobs added outside farming and a few other excluded categories, rose by just 57,000 in June against a consensus near 110,000.

Thing is, the prior two months got revised down by a combined 74,000 jobs. April’s initial gain was cut by 31,000 to 148,000, and May’s was trimmed by 43,000 to 129,000. Revisions happen because early prints rely on incomplete survey responses, and the BLS updates them as more data comes in. A weak headline stacked on top of two downgraded months makes it harder to argue this was a one-off blip.

Leisure and hospitality shed roughly 61,000 positions, a surprising drop given the World Cup was running through the U.S. that month. Health care and professional services kept adding jobs, but not enough to offset the losses elsewhere.

Why Did the Unemployment Rate Fall on Such a Weak Report?

Despite the miss, the unemployment rate dropped to 4.2% from 4.3%. Unfortunately, it’s NOT a hiring story.

To count as unemployed, a person has to be actively looking for work, not just without a job. The labor force participation rate fell 0.3 percentage points to 61.5%, meaning a meaningful chunk of the drop came from people leaving the labor force altogether rather than finding jobs.

A falling jobless rate paired with a shrinking labor force generally reads as a caution sign, since it can point to discouraged workers stepping back rather than an economy generating enough demand to absorb them.

What Did the Rest of This Week’s Data Show?

The jobs report didn’t land in isolation. Two days earlier, the ISM Manufacturing PMI cooled to 53.3 in June from 54.0 in May, missing expectations even as it held on to a sixth straight month of factory-sector growth.

Its Employment Index ticked up to 49.7 from 48.6, but stayed below the 50 mark that separates growth from contraction, meaning manufacturers were still cutting more positions than they added. Its Prices Index dropped sharply to 73.0 from 82.1, the steepest monthly decline since July 2022, a sign that some of the cost pressure manufacturers have been passing along may finally be easing.Wage data told a similar story of cooling. Average hourly earnings rose 0.3% for the month and 3.5% year over year, both in line with expectations. Moderate wage growth tends to be welcome news for the Fed, since rapid wage gains can push businesses to raise prices to cover labor costs, a dynamic known as a wage-price spiral.

The catch is that headline CPI ran at 4.2% year over year in May, with headline PCE, the Fed’s preferred gauge, near 4.1%.

Against that backdrop, 3.5% wage growth likely means real wages, pay adjusted for purchasing power, are still losing ground to the cost of living even as the paycheck number ticks up.

What Does This Mean for the Fed’s July and September Decisions?

The Fed has held its target interest rate at 3.50% to 3.75% since a unanimous decision on June 17, with the next meeting on July 29. Heading into the jobs report, futures markets had priced roughly a 30% chance of a hike at that meeting. After the data, that probability collapsed to about 22%, with a hold now the overwhelming favorite at 78%.

September odds cooled, too: the market implied probability of a September rate hike dropped to nearly 50% from roughly 64% the previous day.

This marks a reversal from the spring, when a run of stronger-than-expected prints had pushed the Dollar Index to a roughly 14-month high and shifted the conversation toward hikes rather than cuts.

Warsh himself gave little away at Sintra, saying inflation remains too high while declining to signal his next move, part of a broader shift among major central bankers away from pre-announcing rate paths. That likely means each new data release, including this one, carries more weight in isolation than it would have under the old playbook.

Promotion: Jobs Missed. Dollar Moved. Did Your Trade Plan Keep Up?

The June jobs report shook up Fed bets and sent the dollar lower. TradeZella’s new AI trading partner can help you review your trades, spot patterns, and build a better game plan for the next move.

Start Your Trading Journey with Tradezella & use code “PIPS20” for 20% off your first purchase!

Disclosure: To help support our free daily content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

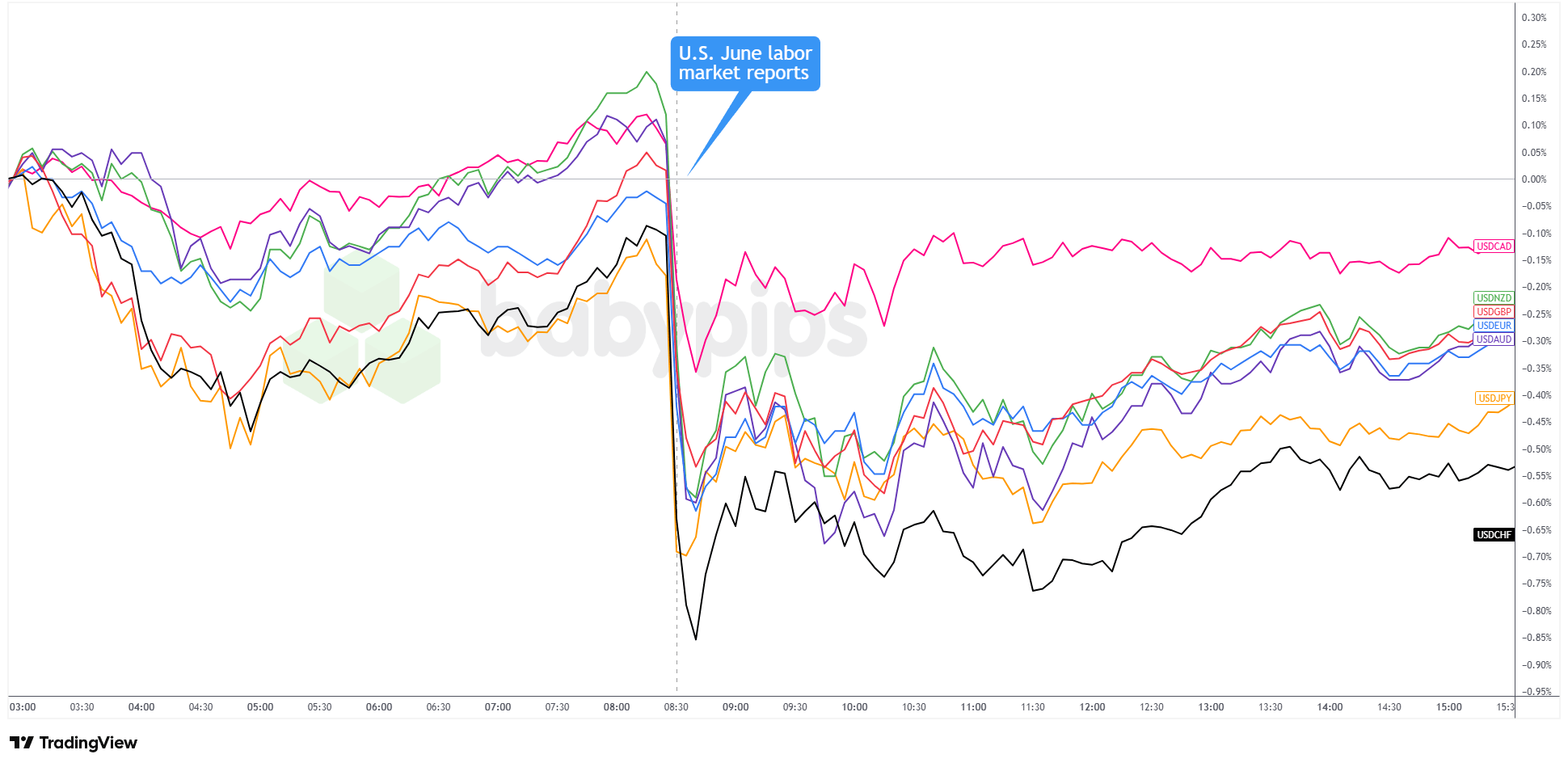

How Did the Dollar React to the Release?

USD 5-minute Forex – Chart Faster with TradingView

The U.S. dollar was already on the back foot through Asia and early London trading, though it did manage to trim some of those earlier losses before the report came out.

But once the data hit at 8:30 a.m. ET, dollar sellers jumped right back in. The Greenback took another quick leg lower against the majors, with the yen and Swiss franc seeing the strongest moves. The Canadian dollar barely moved by comparison, likely because oil’s rally that morning gave the loonie a little extra help.

That first drop didn’t completely hold, though. The dollar clawed back part of the move over the next half hour, then spent the rest of the session in a lower range. It still ended weaker across the board, but not nearly as ugly as the first reaction made it look.

What Should Traders Watch Next?

A single soft report rarely settles anything, especially with core CPI still running at 2.9% and well above the Fed’s 2% target. Views on the Fed’s next move remain split, with some expecting an extended hold and others still not ruling out a hike if inflation reaccelerates.

The June CPI report lands July 14, the last major inflation read before the Fed’s July 28-29 meeting, and the July jobs report follows on August 7, setting up the real test for the September decision.

June’s jobs report missed consensus by nearly half, and making sense of the dollar’s reaction means understanding how rate expectations get priced in before the data ever lands. Premium members can read our lesson:

Market Expectations: Why Good News Can Tank a Currency

Reading this helps you understand how deviation from market expectations drives currency moves, why a falling unemployment rate couldn’t support the dollar on a weak payrolls number, and how to read economic data releases the way the market actually reads them.

And if you’re not a Premium subscriber yet, now’s a good time to sign up.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just what the data shows, but why the gap between the actual number and the consensus is what actually moves currencies.