The Bank of Japan raised its benchmark interest rate to 1.0% on June 16, 2026 — the highest level since 1995 — in a 7-1 vote that matched market expectations and marked Japan’s most decisive step yet away from decades of ultra-low borrowing costs. The 0.25 percentage point increase, which pushes the policy rate up from 0.75%, was driven by mounting inflation pressure tied to Middle East energy costs.

But the story has two major caveats: Governor Kazuo Ueda was absent, hospitalized with a liver cyst infection in an extraordinary first for modern BoJ history, and the recent U.S.-Iran peace memorandum has already started to ease oil prices — raising questions about whether the inflation that justified today’s hike will hold.

Bank of Japan June 2026 Rate Decision: Key Takeaways

- Rate raised to 1.0%: The Policy Board voted 7-1 to hike the short-term rate by 25 basis points (bps) — a basis point equals 0.01%, so 25 bps = 0.25% — from 0.75% to 1.0%, a level not seen since September 1995; board member Toichiro Asada was the lone dissenter, voting to hold rates steady

- Governor Ueda absent: Ueda was hospitalized for a hepatic cyst (a fluid-filled growth on the liver) infection and did not attend or vote; Deputy Governor Ryozo Himino chaired the meeting, while Deputy Governor Shinichi Uchida held the post-meeting press conference in Ueda’s place — the first BoJ policy decision held without the governor in recent history

- Wholesale inflation at 3-year high: Japan’s corporate goods price index (wholesale inflation) rose 6.3% year-on-year in May, the highest in three years, driven by energy costs from the Iran conflict

- CPI overshoot warning: The BoJ flagged that year-on-year consumer price index (CPI) inflation is likely to accelerate clearly above 2%, citing faster-than-expected pass-through of oil prices to everyday goods

- JGB taper paused from April 2027: The BoJ confirmed it will keep reducing monthly Japanese Government Bond (JGB) purchases by ¥200 billion per quarter through March 2027, then freeze monthly purchases at around ¥2 trillion ($12.5 billion) from April 2027 — hawk Naoki Tamura was the sole dissent on this, arguing for further cuts into 2028

- Yen barely moved: USD/JPY — the number of yen needed to buy one U.S. dollar — held above 160.00 after the decision; because the hike was fully priced in, markets had nothing new to react to

- Next hike in Q4 2026: A Reuters economist poll projects the BoJ’s next move to 1.25% in Q4 2026; Governor Ueda is expected to return for the July 30–31 meeting

What Did the Bank of Japan Decide at Its June 2026 Meeting?

The Bank of Japan’s nine-member Policy Board voted 7-1 to raise the overnight call rate — Japan’s key short-term rate, which guides what banks charge each other to borrow money overnight — from 0.75% to 1.0%. That brings Japan’s benchmark borrowing costs to their highest level since September 1995, 31 years ago. It was also the first rate hike since December 2025. The outcome was no surprise: a Reuters poll showed 94% of economists expected this exact move, and overnight index swaps — financial contracts used to price the probability of a rate change — gave it roughly a 96% chance heading into the meeting.

The lone dissenter on the rate decision was board member Toichiro Asada, who voted to keep rates at 0.75%, citing caution about the uncertain economic fallout from the ongoing Middle East situation. The bigger surprise was who wasn’t in the room. Governor Kazuo Ueda — who has led Japan’s historic shift away from negative interest rates since April 2023 — was absent after being hospitalized for a hepatic cyst infection. He submitted his views to the board in writing, but did not cast a vote. Deputy Governor Ryozo Himino chaired the two-day meeting, while Deputy Governor Shinichi Uchida held the post-meeting press conference. It was the first BoJ policy meeting held without the sitting governor in modern central bank history.

Why Did the BoJ Raise Rates? The Inflation Picture

The Bank of Japan has a price stability target of 2% inflation — it aims to keep consumer price growth at around that level in a stable, sustained way. For decades, Japan fought the opposite problem: deflation, or falling prices. But the balance has now shifted. Japan’s corporate goods price index, a measure of wholesale inflation that tracks what businesses pay for goods before those costs reach consumers, rose 6.3% year-on-year in May — a three-year high. The primary driver is the Iran war and its disruption to the Strait of Hormuz, a critical chokepoint that handles roughly 20% of the world’s oil and gas traffic.

Those energy costs are flowing through the economy faster than the BoJ expected. Deputy Governor Uchida stated at his press conference that “pass-through of rising oil prices has been progressing at a relatively faster pace, which could spread to increase in consumer prices across a wide range of items.” In plain terms: businesses are passing higher energy bills on to everyday shoppers, and CPI — the consumer price index, which tracks what households pay for goods and services — is set to climb clearly above the BoJ’s 2% target. With Japan’s real interest rates still negative (meaning the policy rate is still below inflation), the BoJ judged the time to act had arrived.

Promoted: Is Your Small Account Holding Your Strategy Back?

Trading $100 isn’t the same as trading $100k. Emotional discipline & trading flexibility is easier when you have the right backing. FTMO is a global prop firm with a 4.8★ rating on 40K+ reviews, serving traders since 2015! No time limits. Free trials. Up to $200K in Demo Capital.

Start a free trial with FTMO!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

What Is the JGB Taper Pause, and Why Does It Send Mixed Signals?

Alongside the rate hike, the BoJ announced a separate decision about its government bond buying. Since 2024, the BoJ has been gradually reducing how many Japanese Government Bonds (JGBs) — debt issued by the Japanese government to raise funds — it purchases each month. This process is called quantitative tightening, or QT. Reducing BoJ bond buying is meant to shrink its enormous balance sheet and let markets set prices more freely. The existing plan cuts monthly purchases by ¥200 billion each quarter, with the goal of reaching about ¥2 trillion per month by early 2027. That plan was confirmed unchanged on Tuesday.

What’s new is what happens after that. From April 2027, the BoJ will pause further reductions and hold monthly JGB purchases steady at around ¥2 trillion per month. Hawkish board member Naoki Tamura was the sole dissenter on this decision, arguing reductions should continue into 2028. The pause was partly driven by bond market stress: Japan’s 10-year JGB yield had climbed to 2.8% in May — its highest level in about 29 years — signaling that reduced BoJ buying was already straining liquidity. Some analysts called the pause a “dovish structural element” that partially offsets the hawkish rate hike. By fixing its bond buying floor at ¥2 trillion, the BoJ removes upward pressure on long-term yields — which could be read as a concession to the government’s borrowing costs rather than a purely independent policy stance.

What Did Deputy Governor Uchida Signal About Future Rate Hikes?

Uchida struck a deliberately neutral tone at his press conference — keeping the door open to more hikes while refusing to commit to any timing. He said the BoJ “will continue to raise the policy rate in response to developments in economic activity, prices, and financial conditions,” and confirmed that Japan’s real interest rates remain negative in the short- and medium-term zone. That language matters because it maintains the BoJ’s tightening bias — the signal that the direction of rates is still upward — without locking in a specific meeting for the next move.

The complication Uchida could not easily navigate was the U.S.-Iran peace memorandum. He acknowledged it directly, saying “Compared with our previous meeting in April, the U.S. and Iran have signed a memorandum. That is a welcome move” — but added that oil supply uncertainty remains. This matters because energy costs have been the BoJ’s clearest justification for tightening. Goldman Sachs has already cut its Q4 2026 Brent crude forecast to $80 per barrel from $90, signaling that markets are starting to price in cheaper oil as the Strait of Hormuz gradually reopens. If energy-driven inflation fades faster than the BoJ expects, the case for moving quickly to 1.25% weakens. For now, the July 30–31 meeting — when Ueda is expected to return — is the next real decision point for markets to focus on.

What Does the BoJ Rate Hike Mean for Japanese Yen (JPY) Traders?

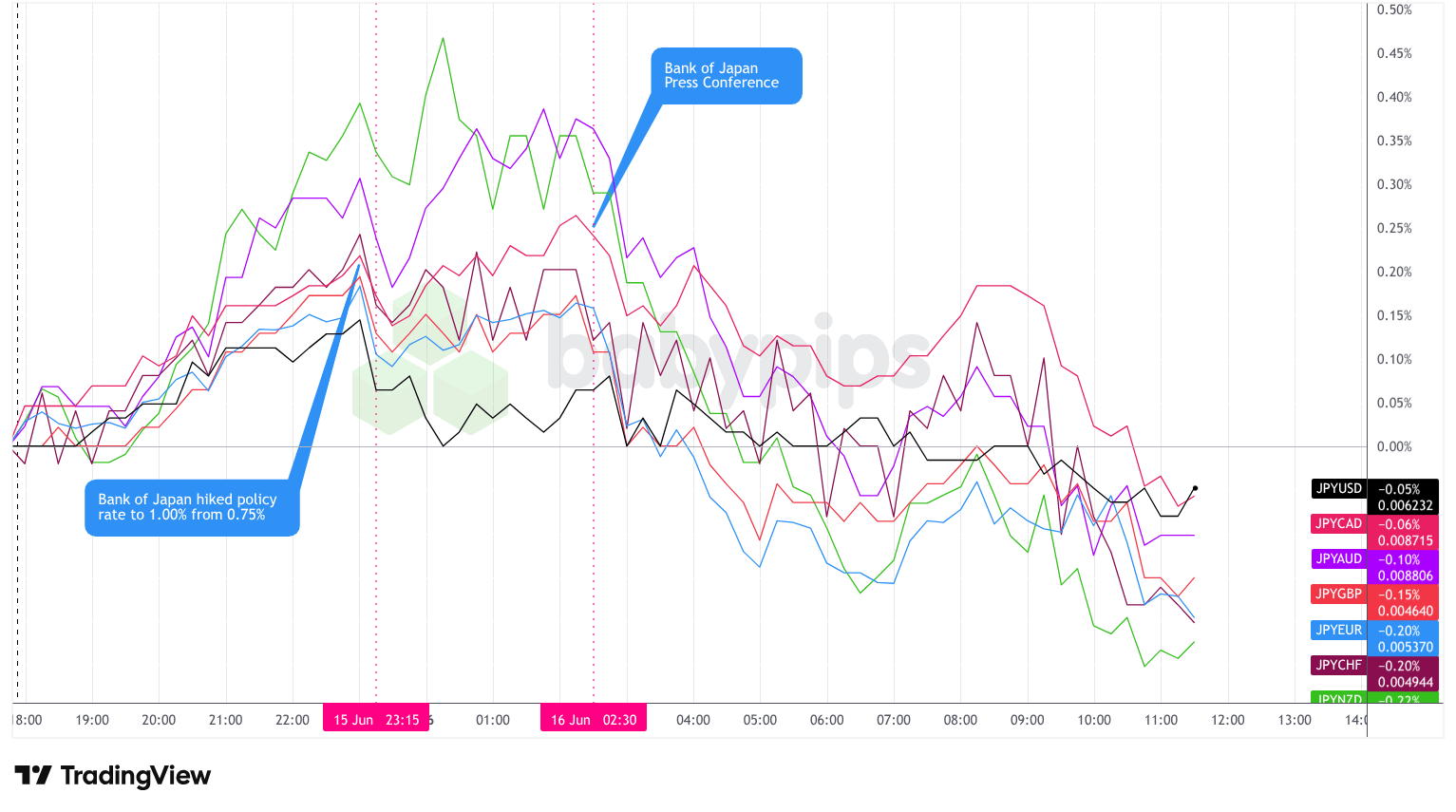

Overlay of JPY vs. Major Currencies – Chart Faster with TradingView

The yen’s reaction on Tuesday was notably muted. USD/JPY — which measures how many Japanese yen it takes to buy one U.S. dollar — held above 160.00 even after the decision. That’s not unusual: when a rate hike is almost fully priced in before the announcement, there is very little new information for markets to react to. In forex trading, it is said that markets “buy the rumor and sell the fact” — meaning by the time the event happens, the move has already occurred. The Nikkei 225 stock index rose 0.46% after the decision, and the 10-year JGB yield climbed 3 basis points to 2.615%, suggesting bond markets welcomed the taper pause as slightly yield-supportive for equities.

The bigger JPY story going forward hinges on three things. First, the pace of future BoJ hikes relative to the U.S. Federal Reserve — the interest rate differential between the two countries is what makes the yen carry trade attractive or not. A carry trade involves borrowing cheaply in a low-interest-rate currency like the yen and investing in higher-yielding assets elsewhere. Second, whether the Iran peace deal meaningfully reduces energy costs and softens the inflation case for further tightening. Third, Ueda’s return to the July meeting and whether he signals a more aggressive or cautious path. Until those questions are answered, USD/JPY is likely to remain in a holding pattern above 160.00.

Promoted: Profitable Trading Isn’t Reserved for Wall Street.

Most traders quietly wonder if consistent profitability is actually achievable for someone like them—or if it’s just a story people tell. Jack Schwager’s newest book, “Market Wizards: The Next Generation,” answers that question directly. The legendary author behind the original Market Wizards series interviews a new generation of successful traders—many self-taught—who built real wealth and income through the markets. Their common thread isn’t genius or insider access. It’s a deliberate process, disciplined risk management, and the conviction to take trading seriously as a pursuit worth mastering.

If that sounds like something worth exploring, this is a good place to start.

Get Market Wizards: The Next Generation on Amazon!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Frequently Asked Questions About the Bank of Japan’s June 2026 Rate Decision

What is the Bank of Japan’s interest rate after June 2026?

The Bank of Japan raised its key short-term policy rate to 1.0% on June 16, 2026. This is up 0.25 percentage points from the prior rate of 0.75%, and the highest the BoJ’s rate has been since September 1995. It was the central bank’s fourth rate hike since it ended negative interest rates in March 2024.

Why does the Bank of Japan’s rate decision matter for forex traders?

Interest rates are one of the most powerful drivers of currency values. When the BoJ raises rates, holding yen-denominated assets becomes more attractive — and the interest rate gap between Japan and countries like the U.S. narrows. That gap, known as the interest rate differential, determines whether the yen carry trade is profitable. Any meaningful shift in the differential can cause fast, large moves in USD/JPY and cross-yen pairs like EUR/JPY and GBP/JPY.

Why was Governor Ueda missing from the June 2026 BoJ meeting?

Governor Kazuo Ueda was hospitalized for a hepatic cyst infection — a condition involving a fluid-filled growth on the liver — and was unable to attend or vote. He submitted his views to the Policy Board in writing. Deputy Governor Ryozo Himino chaired the meeting, and Deputy Governor Shinichi Uchida held the post-meeting press conference. Ueda is expected to return for the next BoJ meeting on July 30–31, 2026.

What did the BoJ say about future rate hikes after June 2026?

Deputy Governor Uchida said the BoJ will “continue to raise the policy rate in response to developments in economic activity, prices, and financial conditions” — but gave no specific timing. A Reuters economist poll projects the next increase to 1.25% sometime in Q4 2026. The pace of future hikes depends heavily on how fast the Strait of Hormuz reopens and whether Iran-related energy price pressures ease or persist.

Why didn’t the yen strengthen more after the Bank of Japan rate hike?

Because the hike was almost fully priced in by markets beforehand — overnight index swaps gave it a 96% probability before the decision. When an outcome is that widely expected, there is no surprise for markets to react to. USD/JPY held above 160.00 after the announcement. For the yen to stage a stronger recovery, traders would need either a clear signal of faster-than-expected BoJ tightening, or a meaningful narrowing of the interest rate gap between Japan and the United States.

The BoJ’s 0.25% rate hike was fully expected by markets, so it barely moved the yen. This is exactly what happens when traders don’t understand how expectations work at central bank meetings. Premium members can read our lesson:

📖 How to Trade Central Bank Decisions Using Market Expectations

Reading this helps you understand why interest rate announcements often fail to move currencies the way traders expect, how to prepare for multiple decision scenarios before the event, and how to distinguish between noise and genuine policy surprises that actually move price.

And if you’re not a Premium subscriber yet, there’s no better time than now.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand how central bank decisions move currencies, how to read what’s already priced in versus what’s new, and how to build directional bias around central bank meetings without getting caught off-guard.