Australia’s labour market delivered a sharp negative surprise in April, with employment falling for the first time since November and the unemployment rate climbing to its highest level since late 2021.

The miss against expectations raised doubts about near-term RBA tightening and sent the Australian dollar broadly lower.

Key Takeaways

- Employment fell 18,600 (m/m) in April to 14,737,400, badly missing forecasts for a gain of around 15,000 and reversing March’s upwardly revised rise of 23,300

- The unemployment rate rose 0.2ppt to 4.5%, the highest since November 2021, against forecasts for a steady 4.3%

- Full-time employment declined 10,700 to 10,160,900, while part-time employment fell 7,900 to 4,576,500

- The participation rate eased 0.1ppt to 66.7%, while hours worked rose 0.8% (m/m) despite the fall in headcount

- Markets cut the implied probability of a June RBA hike to 10% from 20%, and trimmed August pricing from 60% to 40%

Link to official ABS Labour Market Survey (April 2026)

The report likely captures some early effects of the RBA’s three straight interest rate hikes this year, which lifted the cash rate to 4.35%.

With inflation still above target at 4.6% in March, the central bank remains stuck between cooling jobs data and stubborn price pressures.

Markets quickly pared rate hike expectations after the release, pricing only a 10% chance of a June hike, down from 20% earlier. August hike odds also slipped from 60% to 40%.

Market Reactions

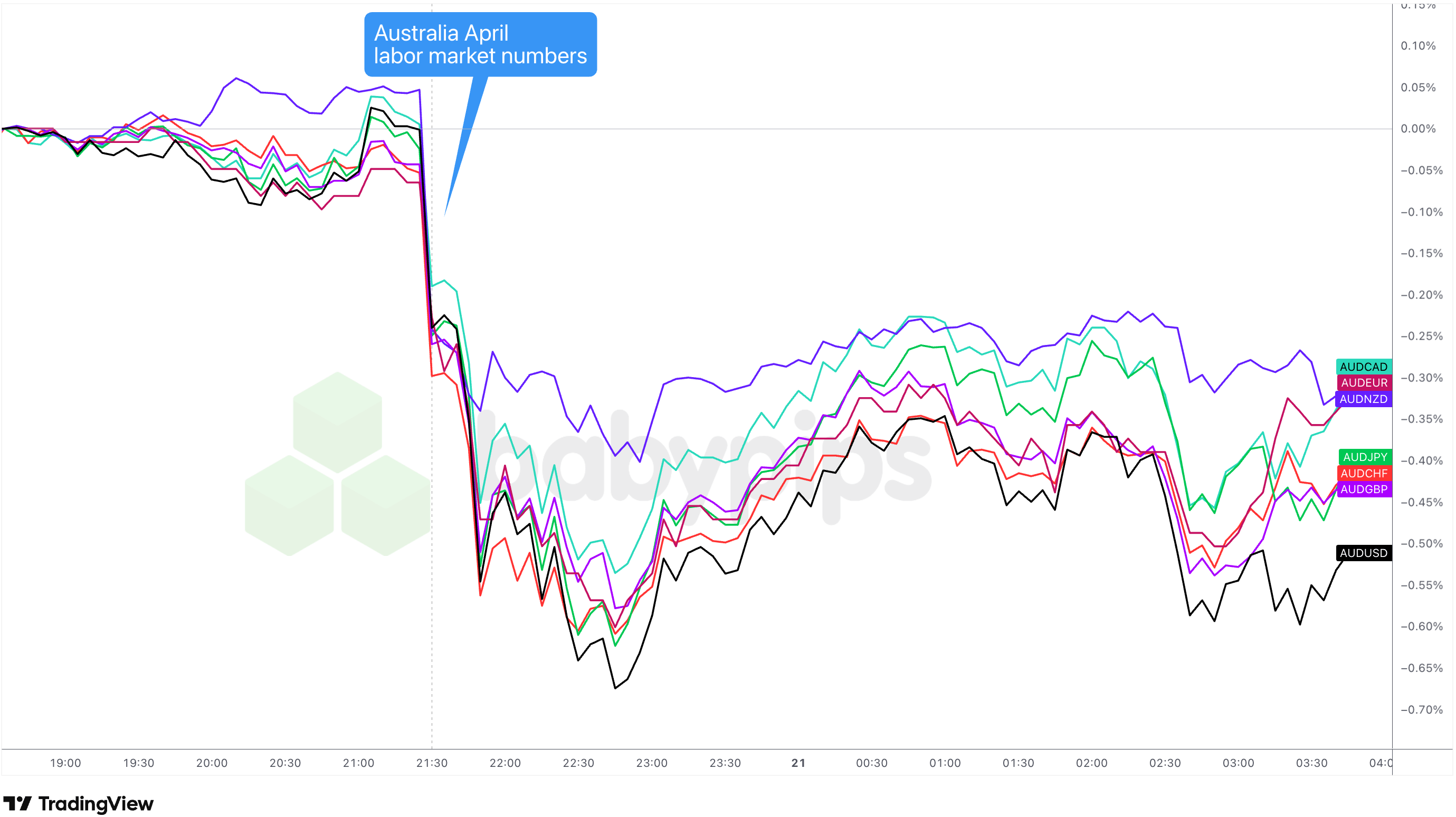

Australian Dollar vs. Major Currencies: 5-min

AUD vs. Major Currencies 5-min Forex Chart by TradingView

The move was made worse by flash May PMI data released around the same time, which showed services slipping into contraction at 47.7 and manufacturing cooling to 50.3. Together, the reports painted a pretty clear picture of an economy losing steam on more than one front.

AUD/USD took the steepest fall, plunging to a session low near -0.65% within minutes of the release, while the other crosses bottomed somewhat higher in the -0.55% range before a choppy and uneven recovery began to take shape just before the European session open.

Most AUD pairs managed to bounce off their intraday lows after the London open, but the recovery was uneven. AUD/JPY, AUD/CHF, and AUD/GBP remained the weakest of the bunch, still down around 0.38% to 0.45%.

The next major test for the Australian dollar is the June RBA meeting, where the case for a pause has been substantially strengthened, though with inflation still running well above target amid the ongoing Iran-driven energy shock, the outlook beyond June remains far from settled.

Beyond that, attention shifts to whether the May flash PMIs — which showed manufacturing easing to 50.3 and services slipping into contraction at 47.7 — mark the start of a broader slowdown, or whether war-driven inflation forces the central bank back into tightening mode regardless.

Australia’s April jobs miss has traders repricing the RBA’s rate path, and if you’re not familiar with how the RBA operates and what drives the Australian dollar, the reaction can be hard to follow. Premium members can read our lesson:

Reading this helps you understand how the RBA sets monetary policy, which economic indicators matter most for AUD, and why a labour market miss like this one can shift rate expectations so quickly.

And if you’re not a Premium subscriber yet, now’s a good time to sign up.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just what the AUD is doing, but the RBA policy dynamics and economic data driving every move.