Sterling was able to pocket a few gains against some of its peers last week, and a few major releases from the U.K. could determine whether it could keep winning or not.

U.K. manufacturing production (Apr. 11, 9:30 am GMT)

The U.K. will print a batch of medium-tier reports around the middle of the week, chief of which might be the manufacturing and industrial production figures.

The former could show a slightly stronger gain of 0.2% versus the earlier 0.1% uptick while the latter might see a slower 0.5% increase compared to the previous 1.3% rise.

Along with this, the goods trade balance will be printed and this could show a smaller deficit of 11.9 billion GBP from the earlier 12.3 billion GBP shortfall, likely reflecting stronger export activity.

Another speech by BOE Guv’nah Carney (Apr. 12, 8:00 pm GMT)

A bit of profit-taking on GBP shorts was seen leading up to head honcho Carney’s speech last week, so we might see the same behavior this time around.

In his earlier testimony, Carney threw the focus on financial stability and climate risk while his upcoming one could have more emphasis on policy.

Overall risk sentiment

Apart from those, the trade spat between China and the U.S. could still impact risk-taking, which suggests that the pound could be sensitive to risk-related flows of its counterparts.

Specifically, watch out for their next steps after announcing their tariff plans. If one of them decides to push the button and actually implement them, or if they find even more products to tax, then we’ll probably see risk appetite dip, which could leave the pound stronger against commodity currencies but weaker versus safe-havens.

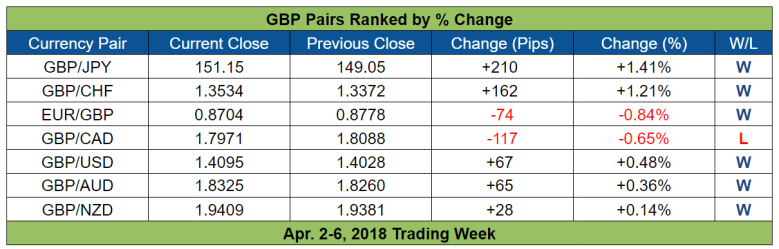

Last Week’s Price Review

The pound overtook the Aussie, the Kiwi, and the Greenback and is currently the second top-performing currency of the week (as of 2 pm GMT), which is a reversal of fortune since the pound was the second weakest currency last week.

Overlay of GBP Pairs: 1-Hour Forex Chart

The pound started the trading week on a somewhat strong footing. There weren’t really any positive catalysts at the time, but short-covering after last week’s sell-off is one possible reason.

The pound’s price action then became more mixed before encountering buyers ahead of the U.K.’s manufacturing PMI report.

And as mentioned in Tuesday’s London session recap, the headline reading managed to beat expectations (55.1 vs. 54.7 expected, 55.0 previous) but Markit’s overall commentary was rather downbeat, which is likely why sellers eventually begin to win out. Well, either that or those bulls who opened preemptive positions were taking some profits off the table.

Anyhow, dip demand was notable so the pound’s losses were limited and pound pairs even began to tilt to the upside (except against CAD and NZD).

The pound then steadied ahead of the U.K.’s construction PMI report. And when that failed to meet expectations (47.0 vs. 50.9 expected, 51.4 previous), the pound found itself reeling across the board.

However, dip demand was once again notable, limiting the pound’s losses on most pair. This may have been due to the fact that the weaker construction PMI reading was because of “unusually bad weather conditions” and that “firms anticipate a rebound in activity during the months ahead.”

However, it’s also possible that overall Greenback weakness was keeping the Sterling supported. Well, that’s what some market analysts think anyway.

Anyhow, the pound apparently became vulnerable to opposing currency price action by the time Wednesday’s U.S. session rolled around since price action on the pound became a mixed mess.

Some semblance of uniformity later returned when sellers began to kick the pound lower after the U.K.’s services PMI reading came in at 51.7 (54.0 expected, 54.5 previous), which is a 20-month low.

The pound-bashing finally ended during Thursday’s U.S. session. No clear reason why, however. Although short-covering ahead of Carney’s Friday speech and the NFP report is a possibility.

Speaking of the NFP report, that was rather disappointing for the Greenback. And as the overlay of GBP pairs clearly shows, it was the pound that was the main beneficiary of the Greenback’s weakness since the pound zoomed higher across the board in the wake of the NFP report.

Incidentally (not really), it’s the pound’s bullish reaction to the NFP report that allowed the pound to overpower the Aussie, the Kiwi, and the Greenback.