“Such a power [of issuing paper currency], in whomsoever vested, is an intolerable evil. All variations in the value of the circulating medium are mischievous: they disturb existing contracts and expectations, and the liability to such changes renders every pecuniary engagement of long date entirely precarious…Not to add, that issuers may have, and in the case of a government paper, always have, a direct interest in lowering the value of the currency, because it is the medium in which their own debts are computed.” – John Stuart Mill

The Fabulous Shrinking Renminbi…

Over the last several years, many writers and assorted cranks, those with little understanding of the global financial system in its current form, have warned “soon [whatever nebulous timeframe that may be] the Chinese currency will replace the US dollar.” Back in early 2000’s we considered such a warning as either total hogwash, or at the least a bit of hyperbole. In fact, back in late 2010 we penned a report for our subscribers titled: “The Chinese yuan will soon replace the US dollar as world reserve currency: Not in this lifetime!” More on that shortly.

I would like to first summarize a recent article in the International Economy magazine, Summer 2017 edition, titled: “Bye, Bye Renminbi,” written by Benn Steil and Emma Smith. It is enlightening for those still concerned the Chinese currency will “soon” replace the US dollar as the world reserve currency.

Though many believed the globalization of the yuan was “remorseless and unstoppable,” the facts on the ground have proven this expectation wrong.

- As of August 2015, renminbi (RMB) used in international payments globally accounted for 2.8 percent of the total, making it the fourth most used currency in the world. Today, the yuan represents only 1.6 percent of total international payments, making it the seventh most used currency.

- Whereas 35 percent of China’s cross-border trade was settled in RMB in 2015 (most of the remainder in US dollars), that share has fallen to about 12 percent today.

- According to Steil and Smith, there are four reasons for this change of fortune for the yuan:

-

First, the dollar value of the RMB rose nearly every year from 2005-2013—by 36.7

percent in total—it has since fallen steadily, discouraging speculators.- The RMB’s fall against the US dollar reflects the slowing of China’s debtfueled economic growth and the accumulation of default risk.

- Chinese residents and companies are seeking new ways to move money out to the country (as the Chinese government is making it increasingly harder to do so by blocking mergers and acquisitions of companies abroad and making capital repatriation more difficult for foreign investors).

- The second reason, and this goes to the Mundellian Trilemma, is Chinese authorities are faced with the prospect of choosing currency flexibility or short-term economic stability. They have chosen stability.

- And the third reason: China has exhausted its export potential. From 1980 to 2015, China’s share of world of world exports grew from 1 percent to 14 percent, respectively; its share has since fallen to 13.3 percent.

- And finally, the reversal of globalization itself.

- Capital flows—in the form of equity and bond purchases, foreign direct investment, and lending, fell by over two-thirds, from $11.9 trillion to $3.3 trillion, between 2007 and 2015. Trade barriers are up. Discriminatory measures are spreading faster than liberalizing policies. Merchandise trade contracted 10 percent between 2011 and 2015; the largest drop over a four year period since WWII. China is therefore not only losing export market share, but is doing so in a shrinking global market. As a consequence, the dollar value of China’s exports ahs fallen by 9.1 percent since its peak in early 2015.

- Thus, the world has little reason to little reason to continue accumulating RMB.

Below is our Executive Summary to our report, “The Chinese yuan will soon replace the US dollar as world reserve currency: Not in this lifetime!” and linked for your review. Granted, the new science of longevity could throw a monkey wrench into our little forecast:

Executive Summary:

- We don’t see any conceivable way the Chinese currency will replace the dollar within the next 30 years.

- In fact, there is a rising probability China may not even be a key global competitor by 2030.

- A look at global monetary standards past suggest that the existing order isn’t as bad as we

think - There is virtually no chance we will see a gold or commodity-based standard again unless we

see a drastic change with our political culture. - The US dollar may have put in a major bottom based on the action in interest rates and our wave charts since implementation of Fed QE2 began.

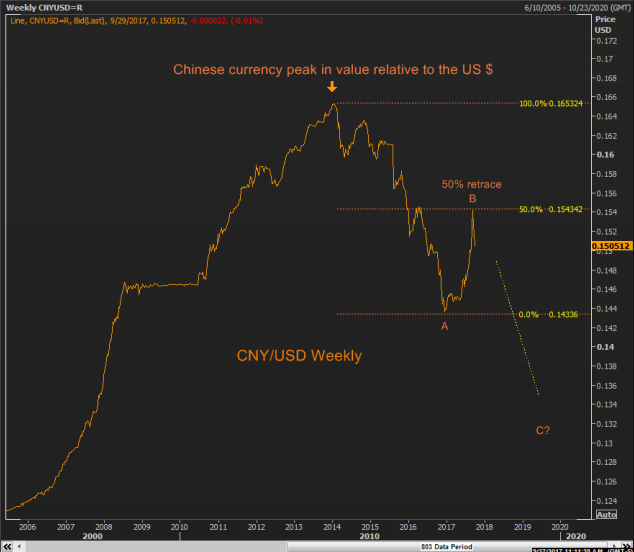

CNY (Chinese RMB) vs. US $ Weekly: Short anyone? CNY/USD hit resistance at key 50% retracement—0.1543—and is working lower.

-

First, the dollar value of the RMB rose nearly every year from 2005-2013—by 36.7