Large players eased their bearish bias on the Greenback for the sixth consecutive week, with the value of net short positions on the Greenback falling from $3.37 billion to a four-month low of $1.92 billion during the week ending on November 7, according to calculations done by Reuters.

And the latest Commitments of Traders (COT) forex positioning report from the CFTC reveals that the positioning activity continued to broadly favor the Greenback. Although the euro was able to finally recover some lost ground after getting pushed back for three consecutive weeks.

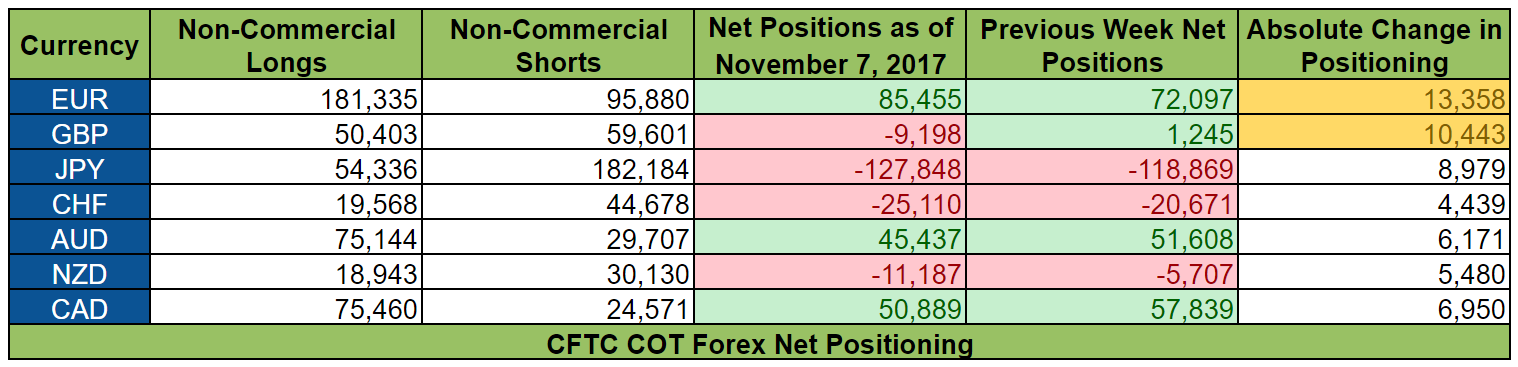

Oh, please keep in mind that the numbers below show the net positioning of non-commercial forex traders against the U.S. dollar.

And if you’re feeling overwhelmed by all these figures, you might need to review our School of Pipsology lesson on How to Gauge Market Sentiment Using the COT Report in order to learn how to pinpoint potential forex market reversals.

And here is how positioning activity played out during the week ending on November 7, 2017.

Net short positions on the Greenback fell yet again, and positioning activity was broadly in favor of the Greenback, which means that sentiment on the Greenback continued to improve.

And net bearish bias on the Greenback likely eased further because the latest FOMC statement was viewed as still favorable for a December rate hike since the Fed maintained its forward guidance that “The Committee expects that economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate.”

Other than that, it’s also highly likely that positioning activity in favor of the Greenback reflects expectations that the U.S. will be able to implement tax reforms soon.

However, the most recent COT report does not yet reflect how large players reacted to the revelation that the U.S. Senate’s version of the tax plan was different compared to the House’s version of the tax plan since the Senate wants to reduce corporate taxes from 35% to 20% starting in 2019, which is a year later than the House’s version of the tax plan.

Anyhow, here are the major events, reports, and other catalysts for the other currencies:

EUR

Sentiment on the euro finally improved after deteriorating for three consecutive weeks. And looking closer, positioning activity was rather bullish since euro bulls reinforced their positions while euro bears trimmed theirs.

Sentiment on the euro likely improved because of fading worries related to Catalonia’s bid for independence.

Other than that, the Euro Zone’s October HICP may have also helped to improve sentiment on the euro because while the headline reading came in at 1.4% year-on-year, missing expectations for a 1.5% rise, HICP is still hitting the ECB’s preferred measures for core inflation, with HICP less energy coming in at 1.2% year-on-year in-line with the ECB’s 2017 forecast of 1.2%.

GBP

Overall sentiment on the pound deteriorated rather substantially. However, a closer look at positioning activity shows that both bulls and bears were actually trimming their positions. The culling of 15,079 long contracts on the pound overwhelmed the reduction of 4,636 short contracts, though.

Positioning activity very likely shows pound bulls getting spooked and pound bears covering their shorts in the wake of the the most recent BOE statement.

After all, the BOE did hike for the first time in a decade, as expected. But the BOE’s forward guidance was also not very promising since the BOE was worried about the negative effects of Brexit and only saw “two additional 25 basis point increases in Bank Rate over the three-year forecast period.”

JPY

The yen took another step back against the Greenback, thanks largely to the buildup of fresh yen shorts.

The BOJ ,maintained its current monetary policy during the latest BOJ statement, which likely highlighted the diverging monetary policy between the Fed and the SNB.

Other than that, appetite for risk was also the dominant sentiment at the time, which may have dampened demand for the safe-haven yen.

Also, the Japanese Lower House re-elected Shinzo Abe as Prime Minister, which likely raised expectations that Abenomics will continue, which again highlights the monetary policy divergence between the Fed and the BOJ.

CHF

Sentiment on the Swissy deteriorated for the eighth consecutive week! As usual, the monetary policy divergence between the Fed and the SNB may have been a factor. However, appetite for risk was also the dominant sentiment at the time, which also likely soured sentiment on the safe-haven Swissy.

AUD

Large players favored the Greenback over the Aussie even more during the week ending on November 7, which marks the sixth week of deteriorating sentiment on the Aussie.

Aussie bulls and Aussie bears were paring their respective positions, though. It just so happens that more Aussie bulls were calling it quits.

The reduction in Aussie longs likely shows bulls running away after Australia’s retail trade turnover showed no growth during the September period (0.4% expected, -0.5% previous), which translated to a year-on-year reading of 2.0%, which is a record low not seen since October 2008.

Aussie longs may have also been disappointed with the latest RBA monetary policy decision since the RBA implied that it had a neutral stance while repeating its warning that “An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.”

As for the reduction in Aussie shorts, that likely reflects profit-taking by Aussie shorts in the wake of Australia’s retail sales report, especially since gold prices surged because of heightened geopolitical risks on November 6.

NZD

Positioning activity on the Kiwi was rather bearish since Kiwi bulls trimmed their bets while Kiwi bears added to theirs.

Large players were likely expecting the RBNZ to sound more dovish during the November 8 RBNZ Statement. Of course, we now know that the remained upbeat and even upgraded its CPI forecasts, which is why the RBNZ also upgraded its forecast for the OCR to show a rate hike by Q2 2019, which is a quarter earlier than originally forecasts.

Moreover, the RBNZ even forecasted a second hike by Q3 2020. Although the RBNZ did say that it’s upgraded forecasts hinge on the Kiwi’s exchange rate staying at current level.

Do note, however, that the latest COT report does not show how large speculators reacted to the RBNZ statement.

CAD

Net bullish bias on the Loonie deteriorated further as Loonie longs reduced their positions further.

The reduction in Loonie longs very likely shows another round of unwinding by Loonie bulls after the BOC statement since BOC governor Stephen Poloz blatantly stated that the BOC now has a neutral monetary policy bias when he said during the BOC Presser that “There’s nothing automatic, no predetermined path for interest rates.”

Poloz would later reiterate the BOC’s more neutral stance when he testified before the House of Commons Standing Committee on Finance that “We are at a crucial spot in the economic cycle, and significant uncertainties are clouding the way forward,” which is why the BOC “will be cautious in making future adjustments to our policy rate.”

Got any other conclusions you can draw from this latest COT Report? Feel free to share your thoughts in the comments section or if you’re looking for further discussion, community member ForExchange has a lively thread called Trading based on Market Sentiment in the forums awaiting your participation.