The value of their net short positions on the U.S. dollar got reduced again during the week ending on October 10, falling from $16.83 billion to $15.42 billion, according to calculations done by Reuters.

And according to the latest Commitments of Traders (COT) forex positioning report from the CFTC, sentiment on the Greenback improved at the expense of most of its forex rivals, with the yen being particularly vulnerable.

However, the COT report also reveals that the Loonie and the euro continued to resist and were even able to take more ground from the Greenback.

Oh, please keep in mind that the numbers below show the net positioning of non-commercial forex traders against the U.S. dollar.

And if you’re feeling overwhelmed by all these figures, you might need to review our School of Pipsology lesson on How to Gauge Market Sentiment Using the COT Report in order to learn how to pinpoint potential forex market reversals.

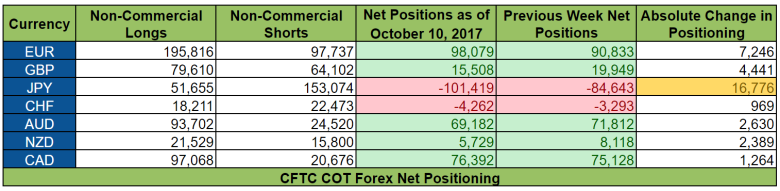

And here is how positioning activity played out during the week ending on October 10, 2017.

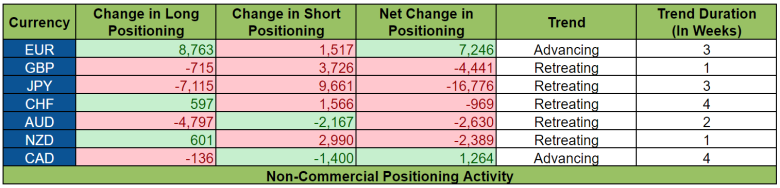

Sentiment on the Greenback improved further during the week ending on October 10. Unlike the previous week, however, positioning activity was more clear-cut since the Greenback took ground from most of its peers. In addition, most currencies saw an increase in short bets, which likely shows positioning in favor of the Greenback and against those currencies.

With that said, sentiment on the Greenback very likely improved because of the September NFP report, as well as leading labor indicators in the runup to the NFP report, since they were net positive.

The ADP report, for example, printed a 135K increase in private non-farm payrolls, which is more than the 131K consensus. Another is the employment sub-index for ISM’s non-manufacturing PMI report since that showed a slight increase from 56.2 to 56.8, which means that jobs growth accelerated a bit.

And while the NFP report itself revealed that the U.S. economy saw a net loss of 33K non-farm jobs instead of generating a net increase of 85K as expected, large players likely weren’t too concerned with jobs growth, though.

After all, the Fed already warned during the September FOMC statement that “payroll employment may be substantially affected in September” because of the hurricanes. Moreover, the Fed said that “such effects should unwind relatively quickly.”

As such, large players were likely already prepared for a disappointing reading for non-farm payrolls and so focus shifted to wage growth. And as it turns out, average hourly earnings grew by a faster-than-expected pace of +0.5% month-on-month (+0.3% expected).

Before we move on to the catalysts for the other currencies, do note that the latest COT report does not yet reflect how large players reacted to the latest FOMC meeting minutes since the minutes were interpreted as dovish overall and caused odds for a December rate hike to drop because the minutes revealed that “many” Fed officials were not sure if weak inflation is temporary, so they called for “some patience in removing policy accommodation.”

Anyhow, here are the major events, reports, and other catalysts for the other currencies:

EUR

Positioning on the euro became even more net bullish since the increase in fresh euro longs was able to easily overwhelm the increase in euro shorts.

The larger increase in euro bets was likely driven by easing concerns related Catalonia, as well as preemptive positioning ahead of the October 26 ECB statement on the expectations that the ECB will likely announce a taper to its asset purchases.

Other than that, demand for the euro was also likely stoked by net positive economic reports the Euro Zone and its major economies.

The Sentix investor confidence index for the Euro Zone as a whole, for instance, printed a 29.7 reading for the month of October, which is the strongest reading since July 2007.

Meanwhile, German industrial production surged by 2.6%, which is a much faster rate of expansion compared to the consensus for a 0.9% increase.

GBP

After four consecutive weeks of pushing back against the Greenback, the pound finally took a step back, thanks mainly to the influx of fresh pound shorts, although the slight reduction in pound longs also helped.

And the bearish positioning activity on the pound likely shows how large players reacted to U.K. Prime Minister Theresa May’s October 4 speech since she didn’t really give any concrete details on her Brexit plans.

Worse, her speech was viewed as eroding her authority and triggered speculation that she may receive a challenge in the near future, according to some market analysts.

JPY

Sentiment on the yen deteriorated substantially further, as yen bulls called it quits and fresh yen bears came out of the woods.

Japanese economic data that were released during the week ending on October 10 were actually mostly positive, so the rather bearish positioning on the yen was likely due to rise in bonds yields at the time, as well as another round of bearish positioning because of the monetary policy divergence between the Fed and the BOJ, given that the BOJ maintained its easing bias during the latest BOJ statement while the Fed has a hiking bias.

CHF

Net change in positioning on the Swissy was only minimal because the 1,566 increase in short contracts on the Swissy was partially offset by the 597 increase in long Swissy contracts.

The increase in Swissy shorts likely reflects positioning in favor of the Greenback against the Swissy because of Greenback demand. As for the smaller increase in Swissy longs, that was likely due to expectations that the Swissy will track the euro higher, given the positive correlation between the euro and the Swissy.

AUD

Net bullish positioning on the Aussie eased even further. However, a closer look at positioning activity reveals that both Aussie bulls and Aussie bears were trimming their respective bets. More Aussie bulls abandoned ship, though, which is why net bullish positioning on the Aussie fell during the week ending on October 10.

The reduction in Aussie shorts likely reflects profit-taking after the Aussie reacted negatively to Australia’s disappointing August retail sales report, which printed a 0.6% contraction (+0.3% expected), the hardest drop since March 2013.

Aside from that, Aussie bears also likely took some profits off the table after the Aussie tanked further as a reaction to RBA Harper’s October 6 comments that “The thing that is causing an issue for us [the RBA] is slow growth in wages, which is feeding into slow growth in household income … If you start to lose that momentum, that might be the basis of some sort of policy action,” which implies that the RBA is open to cutting rates if needed.

As for the slashing of Aussie longs, that likely reflects Aussie bulls getting spooked by the disappointing retail sales report and RBA Harper’s dovish comments.

NZD

The Kiwi retreated thanks primarily to the influx of fresh Kiwi shorts. And the increase in short Kiwi bets, in turn, likely reflects continued political uncertainty in New Zealand after the 2017 general election resulted in a hung Parliament. Although it’s also possible that the increase in Kiwi shorts shows disappointment because the most recent dairy auction resulted in the GDT index falling by 2.6%.

CAD

The Loonie took ground from the Greenback for the fourth consecutive week. Although a closer look at positioning activity shows that this was due mainly to the paring of Loonie shorts.

And the reduction in Loonie shorts likely shows some Loonie bears getting scared away because of Canada’s September jobs report since which showed that full-time employment jumped by 112K in September, which is the biggest monthly gain on record. In addition, wages grew by 1.66% month-on-month, which is the fastest increase since September 2014.

Got any other conclusions you can draw from this latest COT Report? Feel free to share your thoughts in the comments section or if you’re looking for further discussion, community member ForExchange has a lively thread called Trading based on Market Sentiment in the forums awaiting your participation.