After six consecutive weeks of increases, large speculators finally trimmed the value of their net short positions on the U.S. dollar from $17.36 billion to $16.83 billion during the week ending on October 3, according to calculations done by Reuters.

And the latest Commitments of Traders (COT) forex positioning report from the CFTC shows that the Greenback took ground mainly from the yen and the Aussie. However, the COT report also shows that the pound continued to fight back against the Greenback.

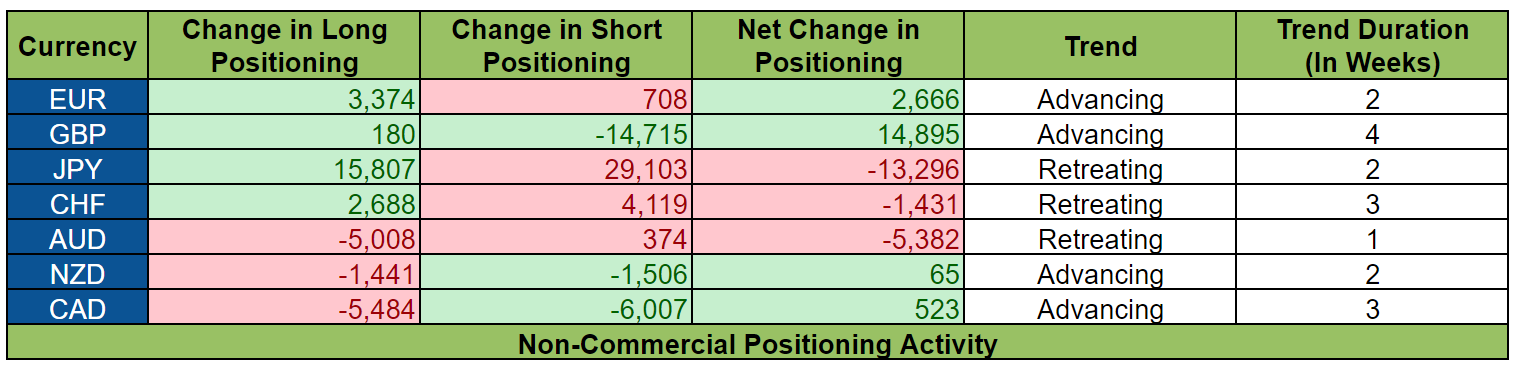

Oh, please keep in mind that the numbers below show the net positioning of non-commercial forex traders against the U.S. dollar.

And if you’re feeling overwhelmed by all these figures, you might need to review our School of Pipsology lesson on How to Gauge Market Sentiment Using the COT Report in order to learn how to pinpoint potential forex market reversals.

And here is how positioning activity played out during the week ending on October 3, 2017.

Sentiment on the Greenback improved for the first time after six weeks, likely because of higher odds for a rate hike, as well as renewed hopes that Trump’s tax plans will push through.

It’s also possible that the favorable positioning on the Greenback was due to preemptive positioning ahead of the NFP report because ISM’s latest manufacturing PMI report, which was released on Oct. 2, printed a better-than-expected reading of 60.8 (57.9 expected, 58.8 previous).

Do note, however, that positioning activity does not yet reflect how large players reacted to the September NFP report. And we now know that the non-farm payrolls fell by 33K instead of increasing by 85K. However, average hourly earning did grow by a faster-than-expected pace of +0.5% month-on-month (+0.3% expected) and the Greenback loved that.

Also, do note that positioning activity was not really broad-based since the Greenback gained mainly at the expense of the yen and the Aussie and the Swissy to a lesser extent. Meanwhile the other currencies fought back against the Greenback. Heck, the pound was even able to take a substantial chunk of ground against the Greenback.

This may have been due to dampened demand for the Greenback because of rumors that were making the rounds back on October 3 that Fed Governor Jerome Powell is supposedly the Trump administration’s pick to replace Yellen as Fed Chair.

You see, Powell is considered less hawkish compared to Kevis Warsh or any of the other candidates. So if Powell is chosen to be the next Fed Chair, then market players figured that there will probably fewer rate hikes in the future.

Anyhow, aside from dampened demand for the Greenback, the mixed positioning activity also heavily implies that catalysts for the other currencies helped to drive positioning activity.

And here are the major events, reports, and other catalysts for the other currencies:

EUR

Sentiment on the euro improved further, but only to a lesser degree compared to the previous week’s substantial shift in net positioning.

And looking at the details, net bullish positioning on the euro improved because of the increase in euro longs, which likely reflects optimism because the European Commission’s consumer and business survey for the month of September printed a 113.0 reading, which is the best reading since 2007.

Also, the Euro Zone’s September HICP likely helped to attract euro bulls because the headline reading of 1.5% is still within the ECB’s 2017 forecast, even though it missed the market’s expectations for a 1.6% rise.

There was a small net increase in euro shorts, though. And that likely reflects political uncertainty because of the Catalan independence referendum, although some of the large players may have been disappointed with the latest inflation report and decided to add their shorts.

GBP

The pound took another substantial chunk of ground from the Greenback.

However, a closer look at positioning activity shows that the pound gained at the Greenback’s expense mainly because of the significant reduction in pound shorts, rather than the influx of pound longs. In fact, the increase in pound longs was only very minimal.

The slashing of pound shorts very likely reflects profit-taking by pound bears because there weren’t really any major positive catalysts at the time, other than Brexit Secretary David Davis’ speech wherein Davis said that both the U.K. and the E.U. are “making decisive steps forward” and “have made considerable progress” in the fourth round of Brexit negotiations.

JPY

The yen took another massive hit from the Greenback, thanks to the influx of 29,102 fresh shorts contracts on the yen, which were able to overwhelm the 15,807 increase in yen longs.

The increase in yen shorts still likely reflects the growing monetary policy divergence between the Fed and the BOJ because the BOJ maintained its easing bias during the latest BOJ statement.

Also, the increase in yen shorts also reflects the increased political uncertainty in Japan after Japanese PM Shinzo Abe’s called for a snap election.

As for the increase in fresh yen longs, that was probably due to the risk-off vibes and falling bond yields at the time.

CHF

Positioning activity on the Swissy was similar to the yen’s in that both Swissy longs and Swissy shorts increased but the increase in fresh shorts was bigger than the increase in longs.

And like the yen, positioning activity on the Swissy, particularly the increase in Swissy shorts, likely reflects the monetary policy divergence between the SNB and the Fed since the SNB has made it clear time and time again that it has no plans to exit its loose monetary policy anytime soon.

The increase Swissy longs, meanwhile, was also probably due to the risk-off vibes at the time.

AUD

Net bullish positioning on the Aussie eased a bit because Aussie longs decided to trim some of their positions while Aussie bears added a bit to theirs.

The rather bearish positioning activity on the Aussie was very likely due to the broad-based commodities rout at the time.

Also, it’s likely that sentiment on the Aussie soured because the RBa maintained its current monetary policy and hinted that it’s in no hurry to start hiking during the latest RBA statement.

Moreover, the RBA tried to talk down the Aussie when it warned that: “The higher exchange rate is expected to contribute to continued subdued price pressures in the economy. It is also weighing on the outlook for output and employment. An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.”

NZD

Net positioning on the Kiwi was only very minimal. But a closer look at positiong activity shows that bulls and bears were both trimming their bets.

Like in the previous week, the reduction in Kiwi shorts likely shows profit-taking because of the political limbo in New Zealand in the wake of the 2017 general election since National got the most votes but failed to capture enough seats for a majority government and there’s even a chance that a Labour-Green coalition may come into power since New Zealand First won enough seats to put either National or a Labour-Green coalition into power.

The reduction in Kiwi longs, meanwhile, likely shows some Kiwi bulls getting spooked, also because of the results of the New Zealand election.

CAD

Net positioning on the Loonie was also rather minimal. And like the Kiwi, Loonie bears and Loonie bears were slashing their respective positions.

The reduction in Loonie longs likely shows Loonnie bulls getting spooked when Poloz disappointed the rate hike junkies when he said during his speech that “there is no predetermined path for interest rates from here. Monetary policy will be particularly data dependent in these circumstances and, as always, we could still be surprised in either direction.”

Also, Canada’s monthly GDP report was a disappointment because GDP growth was flat month-on-month in July (+0.1% expected, +0.3% previous).

The reduction in Loonie shorts, meanwhile, likely reflects profit-taking after deputy Governor Sylvain Leduc refrained from talking about the Loonie and monetary policy during his speech.

Got any other conclusions you can draw from this latest COT Report? Feel free to share your thoughts in the comments section or if you’re looking for further discussion, community member ForExchange has a lively thread called Trading based on Market Sentiment in the forums awaiting your participation.