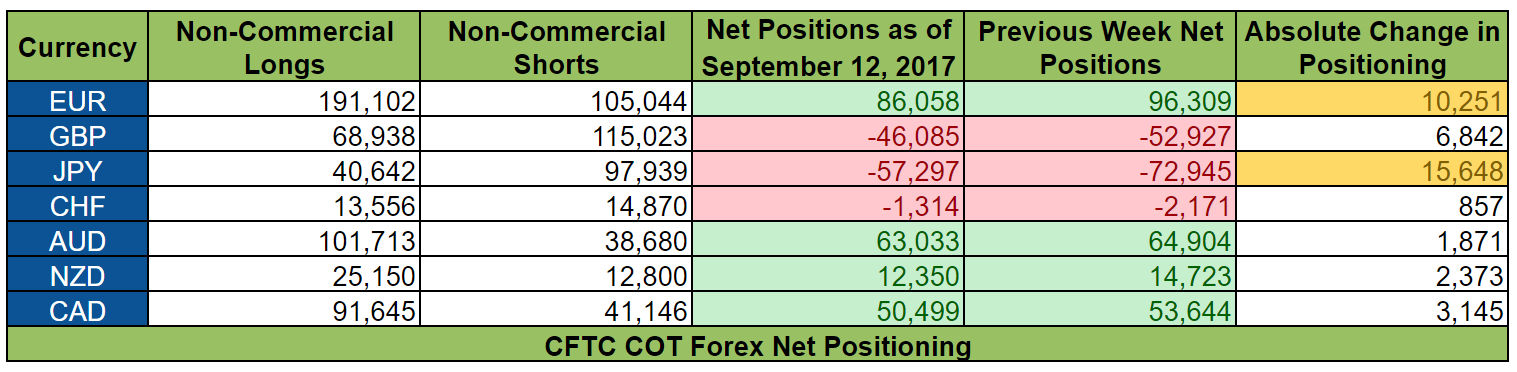

Large speculators boosted the value of their net short positions on the U.S. dollar from $10.98 billion to a 4-½-year high of $11.57 billion during the week ending on September 12, according to calculations done by Reuters.

And the latest Commitments of Traders (COT) forex positioning report from the CFTC shows that the Greenback lost ground mainly against the pound and the yen. However, the COT report also shows that positioning activity was mixed. In fact, the Greenback was actually able to push back against most currencies, particularly the euro.

Oh, please keep in mind that the numbers below show the net positioning of non-commercial forex traders against the U.S. dollar.

And if you’re feeling overwhelmed by all these figures, you might need to review our School of Pipsology lesson on How to Gauge Market Sentiment Using the COT Report in order to learn how to pinpoint potential forex market reversals.

And here is how positioning activity played out during the week ending on September 12, 2017.

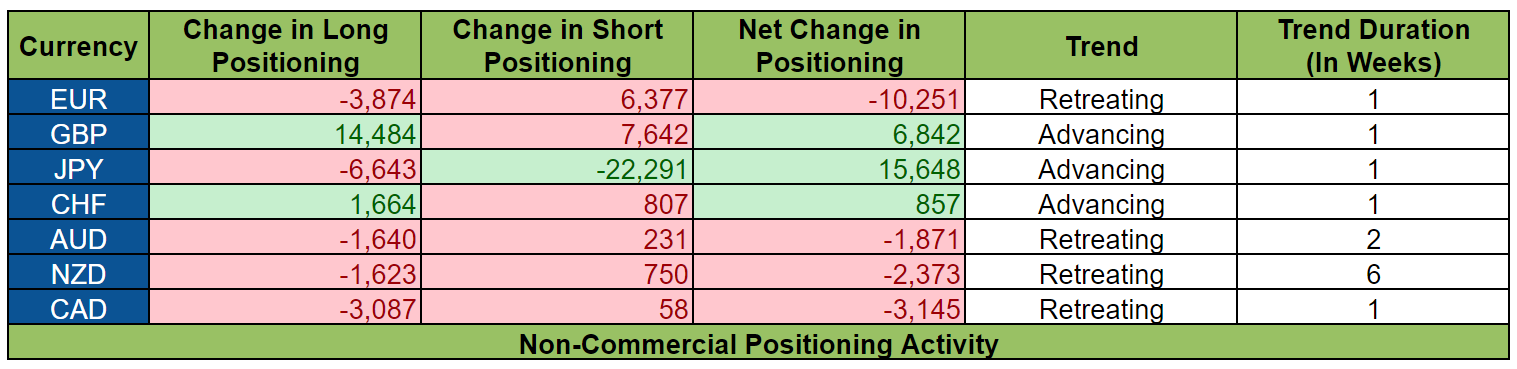

Positioning activity was mixed, so catalysts for the other currencies very likely had a role to play.

With that said, the week ending on September 12 was plagued mostly by worries over the possible damage that Hurricane Irma would bring.

Also there were Fed-related jitters after U.S. Fed Governor Lael Brainard reiterated her dovish stance and FOMC Vice Chair Fischer announced his resignation “for personal reasons.”

However, there were also positive developments. One such development was the agreement to extend the debt limit by three months, avoiding a government shutdown in the process.

Another is New York Fed President William Dudley’s CNBC interview since he calmed everyone’s fears about the damage from Hurricanes Harvey and Irma by saying that: “The long-run effect of these disasters unfortunately is it actually lifts economic activity because you have to rebuild all the things that have been damaged by the storms.”

Moreover, Hurricane Irma wasn’t as devastating as originally thought since it quickly deteriorated upon hitting the U.S. and was only a tropical depression by September 12.

Given this mixed bag of catalysts, it’s somewhat understandable that positioning activity on the Greenback would also be mixed, since catalysts for the other currencies likely had a bigger impact on positioning activity.

Okay, here are the major events, reports, and other catalysts for the other currencies:

EUR

After taking a large chunk of ground from the Greenback during the previous week, the euro took a step back while giving back more than it took since the net change in positioning during the week ending on September 12 was bigger.

Looking at positioning activity, it was rather bearish since euro bulls pared their bets while euro bears added to theirs.

And the major event during the week ending on September 12 was the ECB presser wherein ECB President Mario Draghi said that the ECB “should be ready to give the bulk or to take the bulk of these decisions in October” when referring to the ECB’s expected tightening move.

However, ECB Board Member Benoit Coeure gave a speech on September 11 and Coeure said that the ECB may decide to prolong its loose monetary policy to offset the further strengthening of the euro when he said that “policy will remain more accommodative for longer, thereby likely muting further the pass-through of any growth-driven exchange rate appreciation.”

Coeure also warned that “Exogenous shocks to the exchange rate, if persistent, can lead to an unwarranted tightening of financial conditions with undesirable consequences for the inflation outlook.”

Therefore, the reduction in euro longs likely reflects profit-taking by bulls while euro bears were likely enticed by Coeure’s dovish comments and jawboning on the euro.

GBP

The pound was able to take a sizable chunk of ground from the Greenback. However, a closer look at positioning activity shows that both pound bulls and pound bears were reinforcing their respective positions.

There were far more bulls, though, since pound longs increased by a whopping 14,484 contracts, which is almost double the 7,642 increase in short contracts.

Anyhow, positioning activity likely reflects preemptive positioning ahead of the BOE statement. There were far more longs, though, and that was likely due to a bunch of mostly positive economic reports, with the U.K.’s upbeat CPI report being the most likely drive since it revealed that CPI rose by +2.9%, which is better than the BOE staff forecast of +2.7%.

Of course, we now know that the BOE not only maintained its hawkish bias, the BOE also said that “some withdrawal of monetary stimulus is likely to be appropriate over the coming months,” which is a vague way of saying that a rate hike is coming soon.

The most recent COT report does not yet reflect that, though. Also, the COT report does not yet reflect how large players reacted when BOE MPC Member Vlieghe revealed in a speech that he was has joined the hawkish camp while hinting that the BOE is open to more than just one hike.

JPY

The yen was able to resume its advance against the Greenback, thanks to the massive culling of 22,291 short contracts on the yen, which was able to more than offset the slashing of 6,642 long yen contracts.

The slashing of yen shorts was very likely due to the intense risk-off vibes and falling bond yields at the time, thanks to worries related to Hurricane Irma.

As for the reduction in yen longs, that was likely due to profit-taking by yen bulls since worries related to Hurricane Irma were already fading by September 12.

CHF

As usual, net change in positioning on the Swissy was only minimal. But looking at positioning activity, we can see that there were more Swissy longs than shorts. And the increase in longs was likely due to expectations that the SNB won’t be too hard on the Swissy, given the euro’s recent appreciation against the Swissy.

And we now know that the SNB maintained its monetary policy but changed its assessment on the Swissy from “significantly overvalued” to “highly valued” although the SNB continued to threaten that it would remain active in the forex market to weaken the Swissy.

As for the increase in Swissy shorts, that probably shows speculation that the SNB would weaken the Swissy since the Swissy appreciated because of the risk-off vibes at the time.

AUD

The Aussie continued to lose ground to the Greenback. And positioning activity was quite bearish, too, since Aussie long pared their positions while Aussie shorts slightly added to theirs.

There were no major direct catalysts for the Aussie at the time, but it’s highly likely that the risk-off vibes and falling iron ore prices helped to sour sentiment on the higher-yielding Aussie.

NZD

Like the Aussie, net bullish sentiment on the Kiwi also deteriorated, which marks the sixth consecutive week of souring sentiment on the Kiwi.

And like the Aussie, sentiment on the higher-yielding Kiwi also likely deteriorated because of the prevalence of risk aversion at the time. Other than that, election jitters also likely helped to dampen demand for the Kiwi.

There was a Newshub poll released on September 12 which showed the National Party leading against Labour with a large enough margin that National could have a majority control. However, that didn’t seem to have a major impact on positioning activity.

CAD

Positioning activity on the Loonie was bearish, thanks largely to the slashing of 3,087 long contracts on the Loonie.

The reduction in Loonie longs likely shows some Loonie bulls getting spooked by the hard drop in oil prices on September 8 because of fears that Hurricane Irma would weaken demand.

The reduction in Loonie longs also very likely reflects profit-taking after the BOC unexpectedly hiked yet again, especially since Canada’s jobs report, which was released a couple of days after the rate hike, was not as impressive as it should be since since Canada lost 88.1K full-time jobs.

Got any other conclusions you can draw from this latest COT Report? Feel free to share your thoughts in the comments section or if you’re looking for further discussion, community member ForExchange has a lively thread called Trading based on Market Sentiment in the forums awaiting your participation.