According to calculations done by Reuters, the value of net short positions on the U.S. dollar was raised slightly from $10.28 billion to $10.98 billion during the week ending on September 5. This is the biggest net short position on the Greenback since January 2013.

However, the latest Commitments of Traders forex positioning report from the CFTC shows that the Greenback was able to push back against most of the other currencies. It just so happens that the euro was able to take a rather large chunk of ground from the Greenback, which was enough to push net positioning on the Greenback deeper into bearish territory.

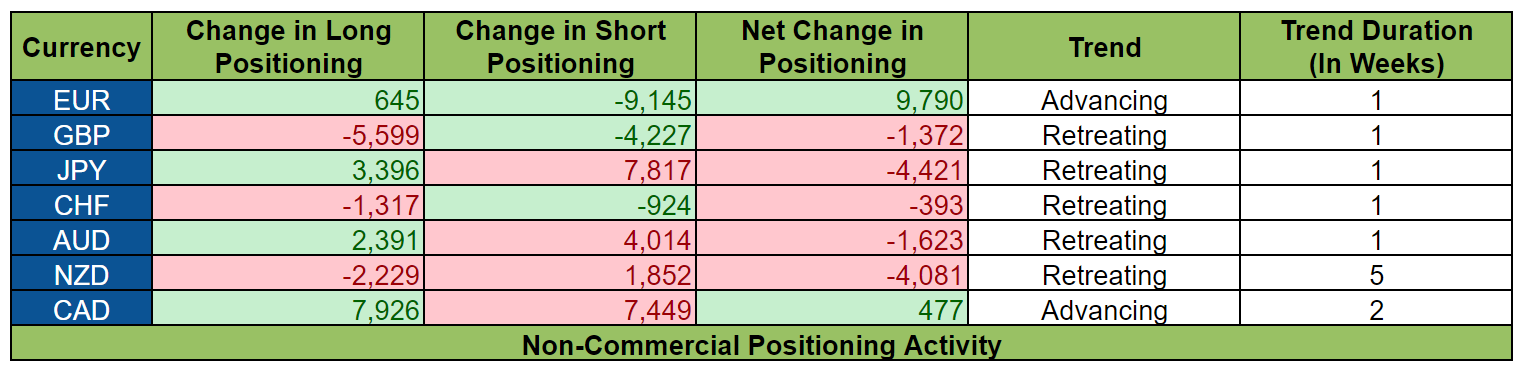

Oh, please keep in mind that the numbers below show the net positioning of non-commercial forex traders against the U.S. dollar.

And if you’re feeling overwhelmed by all these figures, you might need to review our School of Pipsology lesson on How to Gauge Market Sentiment Using the COT Report in order to learn how to pinpoint potential forex market reversals.

And here is how positioning activity played out during the week ending on September 5, 2017.

As you can see above and as mentioned earlier, positioning activity shows that the Greenback was actually able to advance against most of its peers. However, the Greenback’s loss of ground to the euro was enough to ensure that net positioning on the Greenback became even more bearish. It would therefore probably be safe to say that overall sentiment on the Greenback likely improved during this period.

It would also be probably safe to say that positioning activity on the euro was driven more by catalysts for the euro itself, rather than by souring sentiment on the Greenback.

With that said, catalysts for the Greenback during the week ending on September 5 were mixed since we’ve got bullish catalysts like the CB consumer confidence index jumping from 120.7 to 122.9, which is the second highest reading since 2000, as well as the second estimate for U.S. Q2 GDP getting revised higher from +2.6% quarter-on-quarter annualized to +3.0%, which is the strongest growth rate in nine quarters.

Most of the positive catalysts came during the early half, though. Catalysts during the later half of the week ending on September 5 were noticeable more bearish for the Greenback, such as the disappointing August NFP report (156K vs. 180K expected) and dovish rhetoric from U.S. Fed Governor Lael Brainard, as well as news about the damage done by Hurricane Harvey.

Speaking of Hurricane Harvey, the most recent COT report does not yet fully reflect how positioning activity played out when it became apparent that Hurricane Irma would follow after Hurricane Harvey.

And we now know that the expected damage from Hurricane Irma was one of the major reasons for the Greenback’s weakness during the September 4 to 8 trading week.

Okay, here are the major events, reports, and other catalysts for the other currencies:

EUR

Net bullish positioning on the euro improved, thanks largely to the large reduction in euro shorts, although the slight increase in euro longs also helped.

Interestingly enough, Reuters released a report at the time that cited “three sources familiar with discussions” at the ECB, and who claimed that “The exchange rate has become a bigger issue. It is now less favorable for an exit and a stronger argument for a muddle-through option,” adding that “The huge appreciation in the euro is already causing monetary tightening and is equivalent to an increase in interest rates.”

Bloomberg would release a similar report later, citing “unnamed “euro-area officials familiar with the matter.”

And yet large players used that as an opportunity to unwind some of their bearish positions on the euro ahead of the ECB statement, which likely implies that large players were expecting the ECB to give hints on when it plans to starts tightening monetary policy.

Also ECB Governing Council Member Ewald Nowotny did say during a press conference that he “would not over-interpret or dramatise [that] development,” when talking about the euro’s recent strength, which was likely taken as a sign by large players that the ECB wouldn’t try to talk down the euro’s strength too much during the ECB statement.

And while the most recent COT report does not yet show how market players reacted to the ECB statement, we now know that the ECB maintained its current monetary policy but ECB President Draghi said during the presser that “Probably the bulk of these decisions will be taken in October.”

Moreover, Draghi didn’t really try to talk down the euro very hard, saying only that ““Following the recent appreciation of the euro, financial conditions unquestionably tightened in the euro area. But they remain broadly supportive of the non-financial companies and enterprises.”

GBP

Sentiment on the pound continued to sour. However, a closer look at positioning activity shows that bulls and bears were actually slashing their bets on the pound. It just so happens that more pound bulls were abandoning ship than bears.

The reduction in pound shorts likely shows profit-taking by pound bears since on a trade-weighted basis, the pound has become one of the most undervalued currencies in the world, according to some analysts.

As for the reduction in pound longs, that likely reflects souring sentiment on the pound due to Brexit-related jitters because of the lack of progress in the latest round of Brexit talks, as well as political drama related to the vote on the E.U. Withdrawal Bill in the U.K. Parliament.

JPY

After six consecutive weeks, the yen’s advance against the Greenback finally ended. Although positioning activity on the yen wasn’t completely bearish since both yen bulls and yen bears were actually reinforcing their respective positions. The shorts just got more reinforcements than the bulls.

As to why both bulls and bears added to their bets, the increase in yen longs was likely due to the intense risk-off vibes at the time.

The increase in yen shorts, meanwhile, was likely due to the fact that the source of all that risk aversion was the news that North Korea fired a ballistic missile that flew over Japan’s northern island of Hokkaido, which isn’t really all that great for Japan or the yen.

CHF

As has been the case for the past few weeks, net positioning on the Swissy was still only very minimal. More Swissy bulls trimmed their positions than bears, though, despite the risk-off vibes. There are no catalysts for this weird positioning activity but it’s possible that some Swissy bulls were taking profits off the table just in case the SNB decides to intervene.

AUD

The Aussie’s three-week advance against the Greenback came to an end as the influx of fresh Aussie shorts overwhelmed the increase in Aussie longs.

The increase in Aussie longs very likely reflects improving sentiment on the Aussie because of the iron ore rally at the time, as well as the RBA’s upbeat outlook on the economy during the latest RBA statement.

Meanwhile, the increase in Aussie shorts likely shows demand in favor of the Greenback at the expense of the Aussie because of the intense risk-off vibes at the time, which isn’t really a favorable environment for the higher-yielding Aussie.

Also, it may show how large players reacted to the RBA’s usual attempt to try and talk down the Aussie during the latest RBA statement when it reiterated that “An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.”

NZD

Net bullish sentiment on the Kiwi deteriorated for the fifth consecutive week, as Kiwi bulls trimmed their bets while Kiwi shorts added to theirs.

Like the Aussie, the increase in Kiwi shorts likely reflects positioning in favor of the Greenback at the expense of the higher-yielding Kiwi, thanks to the prevalence of risk aversion at the time.

However, the increase in Kiwi shorts also likely reflects souring sentiment on the Kiwi due to RBNZ Governor Graeme Wheeler’s speech, wherein he said that “The appreciation in the exchange rate has been a headwind for the tradables sector and, by reducing already weak tradables inflation, made it more difficult to reach the Bank’s inflation goals.”

Given the above, Wheeler reiterated the RBNZ’s view on the Kiwi by saying that “A lower New Zealand dollar is needed to increase tradables inflation and help deliver more balanced growth.”

This jawboning from Wheeler is also the likely reason as to why Kiwi bulls got spooked and shed some of their positions.

CAD

Net change in positioning on the Loonie was only minimal. However, positioning activity shows that Loonie longs and Loonie shorts were actually adding to their bets.

This mixed positioning activity on the Loonie likely reflects speculative positioning ahead of the BOC statement, with some large players expecting a more hawkish tone while others were likely expecting the BOC to disappoint.

Of course, we now know that the BOC unexpectedly hiked yet again while hinting that it’s ready to hike some more if the Canadian economy continues to improve further.

The latest COT report does not yet reflect that, though.

Got any other conclusions you can draw from this latest COT Report? Feel free to share your thoughts in the comments section or if you’re looking for further discussion, community member ForExchange has a lively thread called Trading based on Market Sentiment in the forums awaiting your participation.