Markets whipsawed Thursday as Iran peace deal optimism that had built overnight gave way to renewed skepticism about an imminent Strait of Hormuz resolution, dragging the S&P 500 back from record territory and sending crude oil on a sharp intraday swing. The U.S. dollar recovered from early softness to close as the best-performing major currency on the session, while rising Treasury yields and hawkish commentary from Minneapolis Fed President Kashkari reinforced a cautious tone heading into Friday’s nonfarm payrolls report.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Australia Balance of Trade for March 2026: -1.84B (4.0B forecast; 5.69B previous)

- Germany Factory Orders for March 2026: 5.0% m/m (1.1% m/m forecast; 0.9% m/m previous)

- Swiss Unemployment Rate for April 2026: 3.0% (3.1% forecast; 3.1% previous)

- Euro area Retail Sales for March 2026: 1.2% y/y (1.1% y/y forecast; 1.7% y/y previous)

- U.S. Challenger Job Cuts for April 2026: 83.39k (56.0k forecast; 60.62k previous)

- U.S. Initial Jobless Claims for May 2, 2026: 200.0k (205.0k forecast; 189.0k previous)

- U.S. Unit Labour Costs Prel for Q1 2026: 2.3% q/q (3.0% q/q forecast; 4.4% q/q previous)

- U.S. Nonfarm Productivity Prel for Q1 2026: 0.8% q/q (2.0% q/q forecast; 1.8% q/q previous)

- U.S. Construction Spending for March 2026: 0.6% m/m (0.4% m/m forecast; -0.3% m/m previous)

- U.S. Consumer Inflation Expectations for April 2026: 3.6% (3.6% forecast; 3.4% previous)

- On Thursday, the U.S. military said Iran attacked three U.S. warships

- The U.S. awaits Iran’s response to their deal proposal to end the war and reopen the Strait of Hormuz

Promoted: Day traders & Scalpers have better odds of making great decisions if they see market catalysts right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

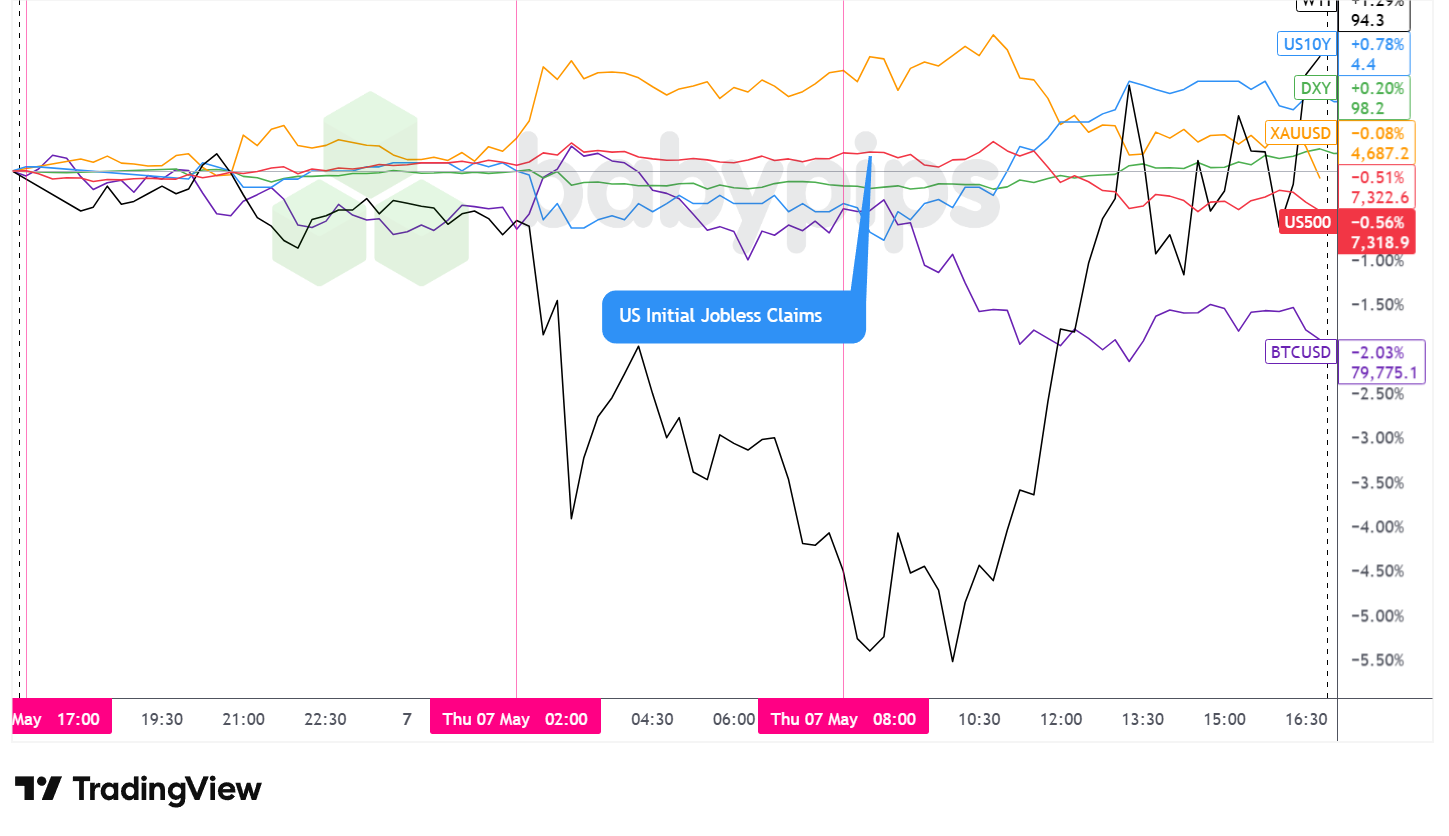

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Thursday’s broad market session was defined by a tension between the risk-on momentum that had built through the Asian hours and a sharp mid-session reversal as doubts resurfaced about whether a U.S.-Iran agreement to reopen the Strait of Hormuz was genuinely imminent. The earlier optimism had sent Japanese equities to record highs and supported commodity-linked currencies overnight, but sentiment shifted considerably as the U.S. afternoon session unfolded.

WTI crude oil was the session’s most volatile asset, with price action that closely tracked the arc of geopolitical sentiment. Prices fell sharply from around $92-93 at the London open, briefly dropping below $90 before the U.S. open, before recovering to near $94 in the early U.S. session. Oil settled near $92.68, roughly unchanged on the day (-0.28%). Late in the session, there were reports of several explosions heard near a port city in southern Iran, and Iranian state television claimed the U.S. military had attacked an Iranian oil tanker. Those late-breaking reports appeared to introduce a fresh round of volatility.

The S&P 500 pulled back 0.25% to close near 7,342, retreating from recent record territory. The index held near 7,380 through much of the Asian session and extended to a peak near 7,385 around 10:30 AM ET before reversing sharply, with losses reaching a low near 7,320. The selloff appeared to coincide with the broad reassessment of deal timeline expectations, as well as the upward move in Treasury yields that developed through the afternoon.

Gold closed up 0.44% near $4,711, one of the session’s better-performing assets. The metal rallied sharply at the London open, clearing $4,750 before consolidating. It pushed to a session high near $4,765 around 10:30-11:00 AM ET before pulling back alongside broader markets, briefly touching support near $4,689 before recovering. Gold’s resilience relative to equities and Bitcoin may have reflected its occasional role as a geopolitical hedge in the current environment, though no specific catalyst for the late-session fall was found, likely attributing it to a rebound in the Greenback.

Bitcoin declined 1.56% to close near $80,159. The cryptocurrency spiked briefly to near $81,750 around the London open before steadily giving back gains through the remainder of the session, dropping to lows near $79,460 around 1:00-2:00 PM ET before partially stabilizing. Bitcoin’s decline was steeper than equities and appeared to track the broader deterioration in risk appetite through the U.S. afternoon.

The U.S. 10-year Treasury yield rose approximately 4 basis points (+0.90%) to close near 4.389%, having traded in a narrow range of roughly 4.33-4.34% through the Asian and London sessions before climbing steadily from the U.S. open. The yield briefly reached a session high near 4.405%, with the move coinciding in part with Minneapolis Fed President Kashkari’s remarks warning that a prolonged Strait of Hormuz closure could force the Fed toward a rate hike. Kashkari, who was among the dissenters at last week’s Fed meeting over forward guidance language, reiterated that he is “very cautious” about the inflation outlook and that elevated inflation cannot be allowed to become the new normal.

Promoted: Is Your Small Account Holding Your Strategy Back?

Trading $100 isn’t the same as trading $100k. Emotional discipline is easier when you have the right backing. Join the world’s leading prop firm with 40k+ 5-star reviews on Trustpilot. Get the capital you deserve.

Learn more about FTMO!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar closed as the best-performing major currency on the session, recovering from earlier softness through a sustained U.S. afternoon rally that extended into the close.

During the Asian session, the dollar traded choppy and mostly sideways with an arguably bearish lean. The session backdrop was dominated by Japan’s Nikkei surging more than 4% on its return from Golden Week, China’s yuan reaching multi-year highs against the dollar, and commodity-linked currencies like AUD and NZD holding near recent tops on easing Middle East fears and the equity bull run on Wednesday. The absence of significant U.S.-specific catalysts likely left the dollar without directional momentum, and the broadly risk-on regional tone appeared to limit its appeal.

After the London open, the U.S. dollar fell against major currencies on a net basis, though the move was relatively contained. The greenback quickly stabilized and traded mostly sideways through the remainder of the European session. European data releases were mixed: German factory orders surprised to the upside, though the jump could have been partly attributed to pre-conflict stockpiling rather than organic demand growth, limiting the positive signal. Construction activity in both Germany and the UK deteriorated sharply. On the monetary policy front, ECB’s Nagel flagged the possibility of rate hikes if the outlook fails to improve markedly, while Villeroy tempered that signal by cautioning against speculating on the specific timing. The dollar’s stabilization despite mixed European signals suggested that broader geopolitical sentiment rather than any single data release was the primary driver during those hours.

After the U.S. session opened, the dollar continued to chop sideways initially before beginning a sustained rally against all major currencies tracked on the overlay chart. Minneapolis Fed President Kashkari’s hawkish remarks on rates, delivered at an event in Marquette, Michigan, and the broader resurgence of Iran deal uncertainty both possibly contributed to greenback support through the afternoon. Fed’s Collins offered a more dovish counterpoint, reiterating her expectation for rate cuts down the road, though her comments did not appear to materially interrupt the dollar’s momentum. Rising U.S. Treasury yields through the afternoon may have provided an additional tailwind for the currency.

Promotion: When the Market Swings, Are You Reacting or Executing?

Monday delivered a “geopolitical shock regime” that saw market volatility rise like a rocketship! Unforeseen market reactions are where even the best technical setups fail, a lot of times due to emotional execution.

In “Positive Trading Psychology,” renowned psychologist Brett Steenbarger reveals in his newest book that the secret to navigating such volatility isn’t “fixing” your flaws—it’s doubling down on your innate character strengths. Learn how to stay clinical while the rest of the market is emotional, turning Monday’s “ticking time bomb” into your professional edge.

Learn more about “Positive Trading Psychology: Turning personal strengths into trading strengths” on Amazon!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- Japan Average Cash Earnings for March 2026 at 11:30 pm GMT

- Japan S&P Global Services PMI Final for April 2026 at 12:30 am GMT

- Germany Balance of Trade for March 2026 at 6:00 am GMT

- Germany Industrial Production for March 2026 at 6:00 am GMT

- U.K. Halifax House Price Index for April 2026 at 6:00 am GMT

- Swiss Consumer Confidence for April 2026 at 7:00 am GMT

- Euro area ECB President Lagarde Speech at 7:00 am GMT

- Euro area ECB de Guindos Speech at 7:05 am GMT

- U.K. BBA Mortgage Rate for April 2026 at 9:00 am GMT

- U.S. Fed Cook Speech at 9:45 am GMT

- Euro area ECB Cipollone Speech at 12:00 pm GMT

- Canada Employment Situation Update for April 2026 at 12:30 pm GMT

- U.S. Manufacturing Payrolls for April 2026 at 12:30 pm GMT

- U.S. Employment Situation Update for April 2026 at 12:30 pm GMT

- University of Michigan Consumer Sentiment Index for May 2026 at 2:00 pm GMT

- U.S. Wholesale Inventories for March 2026 at 2:00 pm GMT

- Euro area ECB Schnabel Speech at 4:00 pm GMT

- U.S. Fed Goolsbee Speech at 11:30 pm GMT

- U.S. Fed Daly Speech at 11:30 pm GMT

- U.S. Fed Waller Speech at 11:30 pm GMT

- U.S. Fed Bowman Speech at 11:30 pm GMT

Friday’s session presents two major U.S. data releases that could move markets in potentially conflicting directions. The April non-farm payrolls report is expected to show the first back-to-back monthly increases in payrolls in almost a year, and Thursday’s initial jobless claims data offered a broadly supportive labor market backdrop, with layoffs remaining muted despite a slight rebound from near multi-decade lows. A social media post from President Trump teasing a strong jobs reading has added to pre-data speculation, though that commentary remains unverified.

Alongside the jobs data, the University of Michigan Consumer Sentiment report will be closely watched for signals on how households are absorbing the ongoing energy price shock and geopolitical uncertainty tied to the Iran conflict. With inflation already running persistently above the Fed’s target and Kashkari warning Thursday that an extended Strait of Hormuz closure could push the next rate move higher, a deterioration in consumer confidence or a jump in inflation expectations within the survey could amplify the hawkish policy narrative.

Markets will likely be sensitive to whether the two reports tell a consistent story: a strong labor market paired with weakening sentiment and elevated inflation expectations could prove a particularly difficult combination for risk assets to navigate heading into the weekend.

Finally, the Canadian employment update will likely be a big driver of volatility for the Canadian dollar, making the Loonie one of the top assets to watch for very short-term trading opportunities before the weekend.

Stay frosty out there, forex friends!

This recap shows how a geopolitical catalyst and Fed commentary can whipsaw markets across multiple timeframes and asset classes within a single session. Most traders react to the headlines, but the ones who profit understand the layers of price action beneath them.

📖 From Data to Price Action: What Happens When Big News Hits

Reading this helps you understand what actually happens in the FX market the moment major news hits, why initial algorithmic spikes differ from secondary analytical moves, and which common traps catch unprepared traders when volatility accelerates.

And if you’re not a Premium subscriber yet, consider signing up to deepen your understanding of how news and catalysts move markets.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just which way price moved, but why it moved that way, how to read the layers beneath each price swing, and what to do when unexpected catalysts create trading opportunities or risks.