Thursday’s session turned on a sharply weaker U.S. June jobs report that undershot forecasts by a wide margin, sending the dollar to the bottom of the major-currency table and lifting gold roughly 2%. The soft print also cooled the rate-hike pricing that had built up under new Fed Chair Kevin Warsh. Equities chopped either side of flat as an overnight rotation out of AI-infrastructure names faded through the day, while oil firmed despite signs of easing Middle East supply risk.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- U.S. and Iranian negotiators wrapped indirect technical talks in Doha, with Qatar’s foreign ministry reporting positive progress on issues tied to the Islamabad memorandum of understanding and both sides agreeing to keep talking.

- Australia Balance of Trade for May 2026: -3.02B (2.5B forecast; 1.79B previous)

- Swiss Inflation Rate for June 2026: 0.5% y/y (0.6% y/y forecast; 0.6% y/y previous); 0.0% m/m (0.2% m/m forecast; 0.2% m/m previous)

- U.S. Total Vehicle Sales for June 2026: 16.5M (16.1M previous)

- Euro area Unemployment Rate for May 2026: 6.2% (6.3% forecast; 6.3% previous)

- U.S. Initial Jobless Claims for June 27, 2026: 215.0k (210.0k forecast; 215.0k previous)

- U.S. U-6 Unemployment Rate for June 2026: 7.9% (8.1% forecast; 8.1% previous)

-

U.S. Nonfarm Payrolls for June 2026: 57.0k (110.0k forecast; 172.0k previous)

- U.S. Average Hourly Earnings for June 2026: 3.5% y/y (3.4% y/y forecast; 3.4% y/y previous)

- U.S. Unemployment Rate for June 2026: 4.2% (4.3% forecast; 4.3% previous)

- Canada S&P Global Manufacturing PMI for June 2026: 53.0 (53.4 forecast; 52.9 previous)

- U.S. Factory Orders for May 2026: -1.3% m/m (-1.7% m/m forecast; 4.8% m/m previous)

Promoted: Capitalize on NFP Volatility

When a massive U.S. jobs miss sends the dollar tumbling and gold spiking, having the right read on the market is only the first step—you also need the capital to truly take advantage of the move.While new firms come and go with the volatility, The5ers has spent the last 10 years perfecting a funding model that works for the trader. It’s why over 1.6 million traders worldwide trust them to provide the capital and scaling needed to turn market analysis into meaningful professional growth.

Learn more about The5ers Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

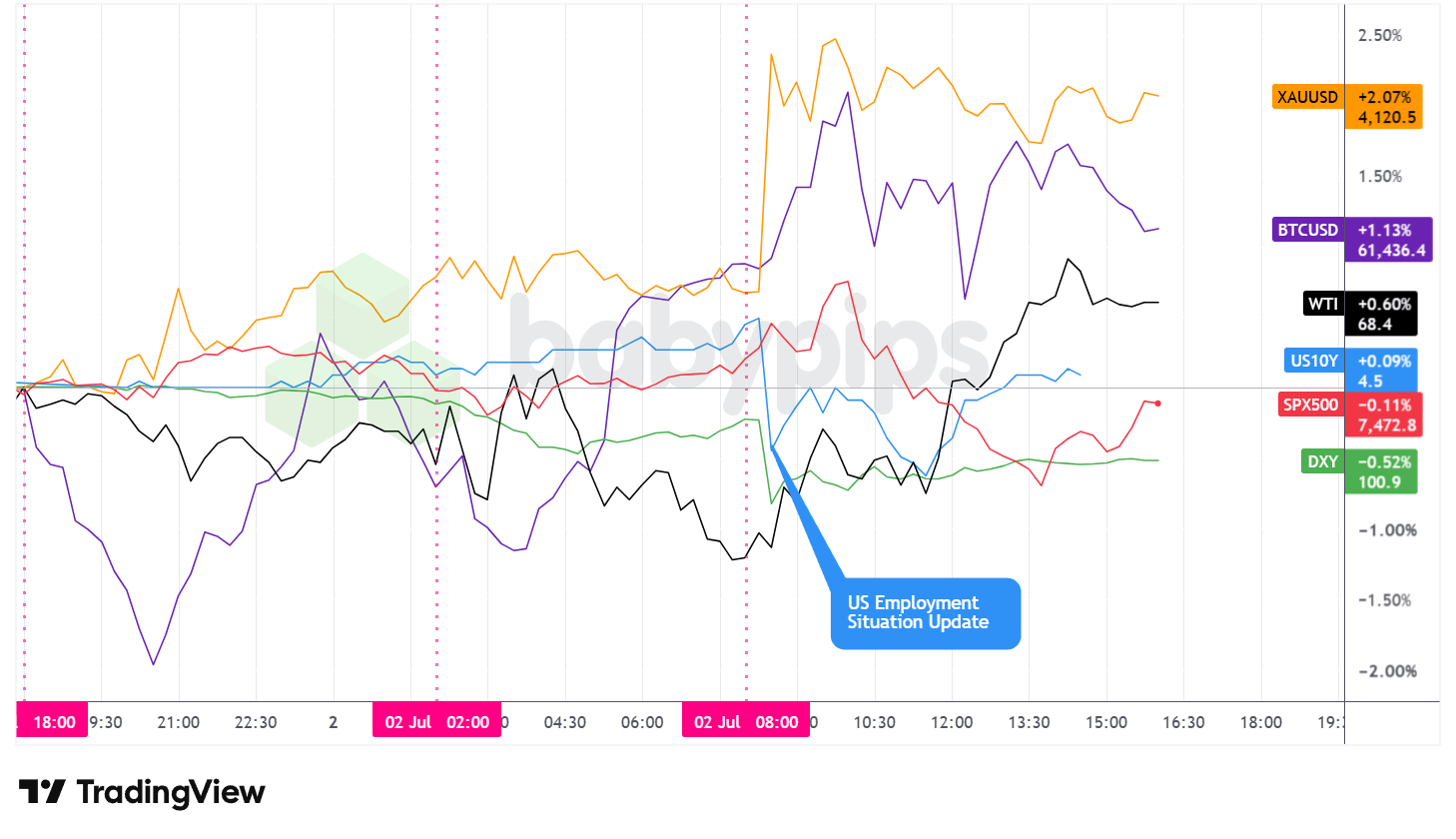

Broad Market Price Action:

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Thursday delivered a textbook weak-payrolls reaction, though the follow-through faded as the session wore on. Because of the holiday-shortened week, the jobs report landed Thursday rather than its usual Friday slot, and the U.S. bond market closed early ahead of Friday’s Independence Day closure.

Gold posted the day’s strongest gain, climbing roughly 2.07% to trade around $4,120 per ounce. The metal traded quietly through the Asian and London sessions before spiking on the 8:30 a.m. ET release to a peak near $4,144, then easing back into the afternoon. The move lined up with the softer jobs print, a weaker dollar, and receding rate-hike odds, all of which tend to support the metal. For the medium term, it’s worth noting that a recent OMFIF survey found central banks themselves expect gold to trade in a $5,000 to $6,000 range over the next twelve months.

The S&P 500 finished close to unchanged, easing roughly 0.11% to around 7,473. Price action was choppy in both directions. The index popped toward 7,541 in the hour after the data as traders welcomed the softer labor read, then reversed and slid to a session low near 7,427 around midday before rebounding into the close. It’s possible that the payroll slowdown undercuts the recent narrative of a re-strengthening labor market while reinforcing that the Fed faces little pressure to tighten.

Bitcoin rose about 1.13% to trade near $61,436. After an early Asia session dip, it climbed through the London session and early U.S. session to a peak around $62,147 by mid-morning U.S., then drifted lower for the rest of the session, roughly tracking the fade in equities. There were no notable crypto news to point to on the day, likely pointing to falling rate hike fears/U.S. dollar weakness and improving risk sentiment as the driver on the day.

WTI crude firmed around 0.60% to settle near $68.40, a move that ran counter to the day’s Asian-session narrative. Oil drifted to a low around $67.00 through the overnight and early London hours, then rallied steadily through the U.S. session to a peak near $68.72 before easing slightly. The gain came despite the constructive tone from the Doha talks, and with no single obvious catalyst, the afternoon strength possibly reflected short covering, USD weakness and broader positioning rather than a fresh supply story.

The U.S. 10-year Treasury yield finished little changed, hovering around 4.44%. Yields had firmed overnight toward 4.46%, dropped to about 4.43% on the jobs release, then recovered through the afternoon to close near their pre-data levels. The muted net move suggested that traders may have balanced the weaker growth signal against still-elevated wage growth.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Most trading mistakes aren’t technical—they’re psychological. In the classic “Trading in the Zone” by Mark Douglas (⭐ 4.7★ | 10,000+ reviews on Amazon), you’ll learn how to master the probabilistic thinking and emotional discipline mentioned in today’s article. If you struggle with hesitation or breaking your rules, this is your manual for consistent execution.

Click on the link to learn more about “Trading in the Zone” by Mark Douglas!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

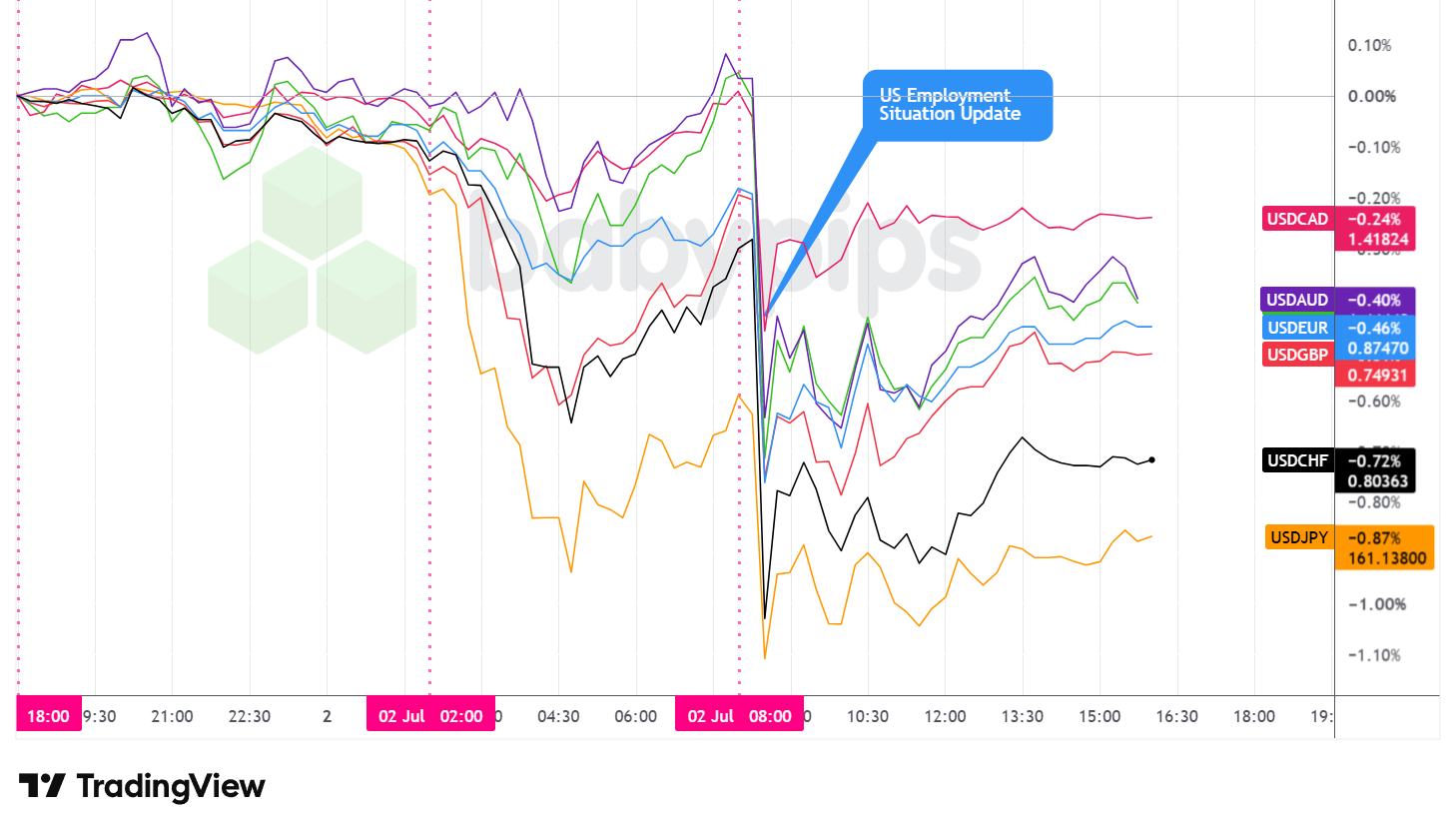

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar ended Thursday as the worst-performing major currency on a daily basis, slipping to roughly a two-week low against its peers. The weak jobs report drove the bulk of the decline, cooling the rate-hike pricing that Warsh’s hawkish June stance had built up and pulling the greenback lower across the board.

From the Thursday Asian open through the London open, the dollar saw low volatility and traded mostly sideways with an arguably net bearish bias. No regional catalyst pushed it in a clear direction during those hours, and it’s likely traders were sitting on the sidelines waiting for the U.S. jobs update.

After the London open, the dollar took on a stronger bearish lean into mid-morning London before rebounding heading into the U.S. session. The London hours also brought a sharp, brief move in the yen, with USD/JPY dropping around 100 pips before quickly rebounding. With the yen sitting near multi-decade lows, it’s possible that move was intervention action or a rate check by Tokyo, though the more likely read may simply be nervous positioning ahead of the thin liquidity expected around the holiday.

After the U.S. session opened, the dollar fell against the major currencies, correlating with the latest U.S. employment data. It stabilized quickly after the drop, traded sideways, then rebounded slightly into the afternoon and steadied into the close. The dollar’s steepest losses came against the yen and the Swiss franc, while it held up best against the Canadian dollar, which lagged as oil’s rally offered only limited support.

Promoted: Day traders & Scalpers have better odds of making great decisions if they see market catalysts right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- New Zealand ANZ Roy Morgan Consumer Confidence for June 2026 at 10:00 pm GMT

- Australia S&P Global Services PMI Final for June 2026 at 11:00 pm GMT

- Japan S&P Global Services PMI Final for June 2026 at 12:30 am GMT

- China RatingDog Services PMI for June 2026 at 1:45 am GMT

- Germany S&P Global Services PMI Final for June 2026 at 7:55 am GMT

- Euro area S&P Global Services PMI Final for June 2026 at 8:00 am GMT

- European Central Bank President Lagarde Speech at 8:00 am GMT

- U.K. S&P Global Services PMI Final for June 2026 at 8:30 am GMT

- Germany New Car Registrations for June 2026 at 10:00 am GMT

- Bank of England Governor Bailey Speech at 3:00 pm GMT

- U.S. Markets Closed for U.S. Independence Day

With U.S. markets shut for the U.S. Independence Day holiday, liquidity is likely to run thin and price action can turn erratic on light volume, so position sizing matters more than usual.

The calendar leans on final services PMIs across Asia and Europe, which rarely move markets far from their flash readings but can still sharpen the growth picture. Traders will listen to Lagarde and Bailey for any tone shift after this week’s Sintra panel, particularly on how each central bank now frames the path for rates without leaning on forward guidance.

Stay frosty out there, forex friends!

When weak economic data hits the market, the initial reaction seems straightforward: bad news, weaker currency. But what actually drove Thursday’s dollar selloff wasn’t just the weak jobs print itself, it was how far the number missed expectations. Premium members can read our lesson:

📖 Market Expectations: Why Good News Can Tank a Currency

Reading this helps you understand why currencies move on deviations from expectations, not the headline number itself, and how to interpret market reactions instead of being confused by them.

And if you’re not a Premium subscriber yet, now’s a good time to join.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just what the headlines say, but how market expectations shape currency moves before and after the data lands.