Wall Street closed its strongest quarter in six years on Tuesday, with chipmakers leading a tech-driven advance that pushed the S&P 500 to fresh highs near 7,500. The dollar drifted mixed and arguably neutral to slightly net bearish against the majors, gaining ground only on the yen, while Bitcoin slid below $60,000 as confidence in one of crypto’s largest corporate buyers wobbled.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Japan’s Chief Cabinet Secretary Kihara and Finance Minister Katayama both signaled readiness to act

- Japan Unemployment Rate for May 2026: 2.5% (2.5% forecast; 2.5% previous)

- Japan Industrial Production Prel for May 2026: 0.5% m/m (0.3% m/m forecast; 0.5% m/m previous)

- New Zealand ANZ Business Confidence for June 2026: 36.6 (11.0 forecast; 10.0 previous)

- Australia Housing Credit for May 2026: 0.5% m/m (0.5% m/m forecast; 0.6% m/m previous)

- Australia Private Sector Credit for May 2026: 0.7% m/m (0.6% m/m forecast; 0.7% m/m previous); 8.2% y/y (8.0% y/y forecast; 8.0% y/y previous)

- China NBS Manufacturing PMI for June 2026: 50.3 (50.3 forecast; 50.0 previous)

- China NBS Non Manufacturing PMI for June 2026: 50.2 (50.5 forecast; 50.1 previous)

- Japan Housing Starts for May 2026: 33.9% y/y (30.0% y/y forecast; 11.4% y/y previous)

- Germany Import Prices for May 2026: 0.7% m/m (0.5% m/m forecast; 1.2% m/m previous)

- Germany Retail Sales for May 2026: 1.8% y/y (-0.4% y/y forecast; -0.3% y/y previous)

- U.K. GDP Growth Rate Final for Q1 2026: 0.9% y/y (1.1% y/y forecast; 1.0% y/y previous)

- Swiss KOF Leading Indicators for June 2026: 101.2 (99.0 forecast; 98.0 previous)

- Germany Unemployment Rate for June 2026: 6.3% (6.4% forecast; 6.3% previous)

- Germany Unemployment Change for June 2026: -1.0k (10.0k forecast; -12.0k previous)

- Germany CPI Growth Rate Prel for June 2026: 2.3% y/y (2.7% y/y forecast; 2.6% y/y previous)

- Canada GDP Prel for May 2026: 0.1% m/m (0.1% m/m forecast; 0.4% m/m previous)

- U.S. S&P/Case-Shiller Home Price for April 2026: 1.1% y/y (0.8% y/y forecast; 0.8% y/y previous)

- U.S. Chicago PMI for June 2026: 56.7 (61.0 forecast; 62.7 previous)

- U.S. JOLTs Job Openings for May 2026: 7.59M (7.4M forecast; 7.62M previous)

- U.S. CB Consumer Confidence for June 2026: 91.2 (94.0 forecast; 93.1 previous)

- U.S. Dallas Fed Services Index for June 2026: 2.9 (-4.0 forecast; -7.7 previous)

Promotion: Lux Trading Firm funds with real capital (up to $10M in buying power), refunds 1-step evaluation fees 100% after Stage 1. Highly competitive Instant funding plans & prediction market plans are available. Get a certified track record, and a potential salary for long-term focused, highly qualified performers.

Learn More at Lux Trading Firm

Disclosure: To help support our free daily content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

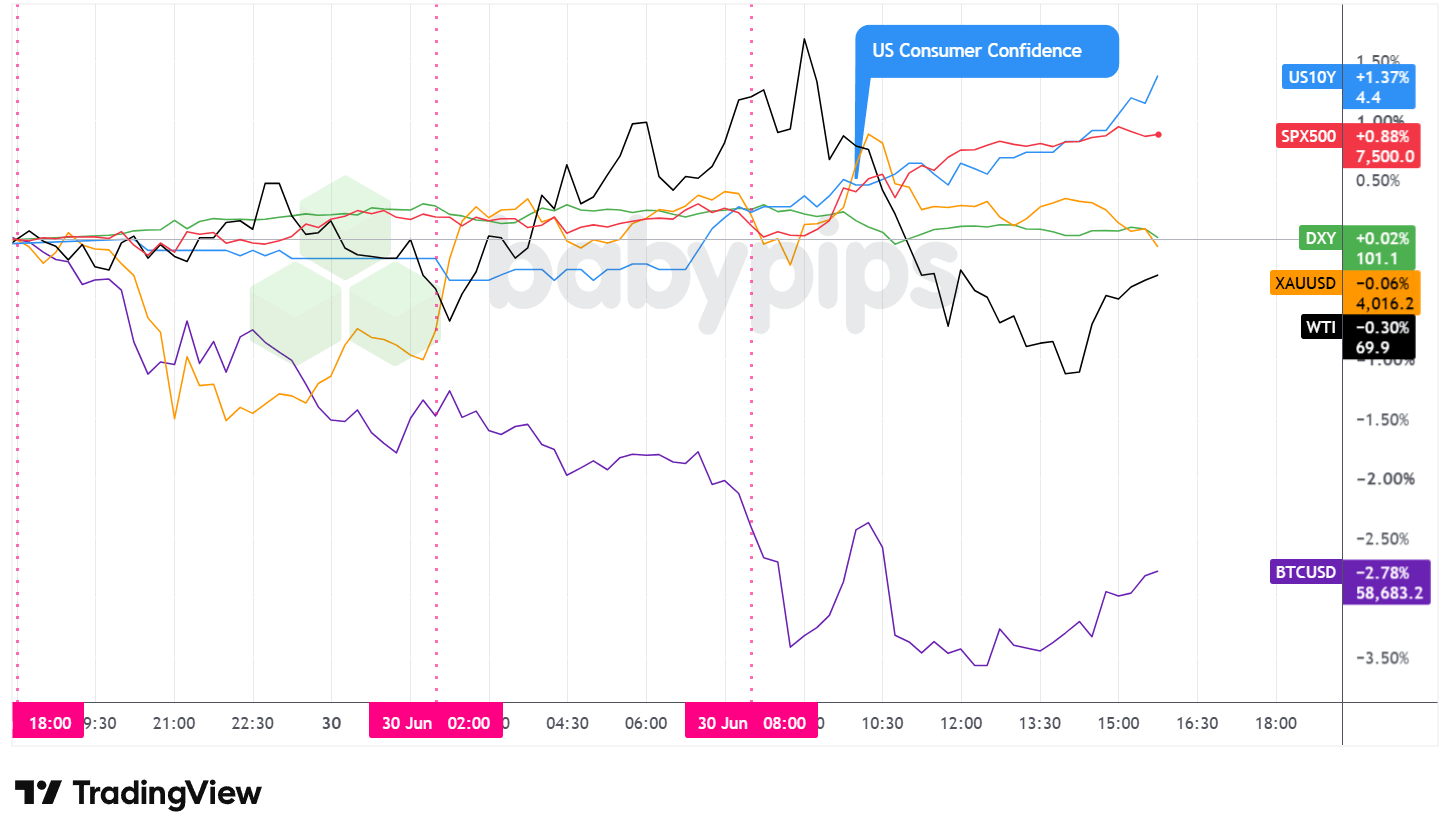

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Tuesday capped a quarter that added trillions to U.S. equity value, and risk appetite carried through the close.

The S&P 500 closed near 7,500, up roughly 0.88% on the day. The index chopped between about 7,420 and 7,460 overnight, dipped toward 7,433 into the early U.S. hours, then ran steadily higher from mid-morning to a peak around 7,508 near 3 PM ET before easing into the close. Resilient jobs and consumer data, combined with the semiconductor surge, possibly reinforced the bid.

WTI crude settled near $69.90, lower by approximately 0.30%. Oil traded around $70.20 through Asia, climbed to a session high near $71.38 around the U.S. open, then slid to a low around $69.09 in the early afternoon before recovering. The retreat may reflect easing supply-risk premium as Hormuz traffic normalized and U.S.-Iran talks advanced, though no single catalyst cleanly explains the intraday swing.

Gold finished near $4,016, down about 0.06%. The metal dropped under $3,942 overnight, recovered above $4,000, and spiked to roughly $4,063 around mid-morning before fading back toward $4,016. The late drift lower possibly reflected profit-taking as risk sentiment held firm and yields climbed.

Bitcoin underperformed, sliding around 2.78% to trade near $58,683. The token fell from roughly $60,400 to a low near $58,056 before clawing back some ground late in the session. The slide followed a reversal in sentiment toward Michael Saylor’s Strategy Inc., whose capital overhaul gave management more flexibility to sell Bitcoin rather than accumulate it relentlessly, raising doubts about a key source of demand. The technical aspect of Bitcoin price behavior has turned very negative recently, pointing to a break below the year’s lows.

The 10-year Treasury yield rose, ending near 4.40%, up roughly 1.37%. Yields traded sideways through Asia and London, then climbed through the U.S. session. Firm JOLTS openings and a strong Dallas Fed services reading possibly outweighed the softer consumer confidence print, supporting the move higher.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Most trading mistakes aren’t technical—they’re psychological. In the classic “Trading in the Zone” by Mark Douglas (⭐ 4.7★ | 10,000+ reviews on Amazon), you’ll learn how to master the probabilistic thinking and emotional discipline mentioned in today’s article. If you struggle with hesitation or breaking your rules, this is your manual for consistent execution.

Click on the link to learn more about “Trading in the Zone” by Mark Douglas!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

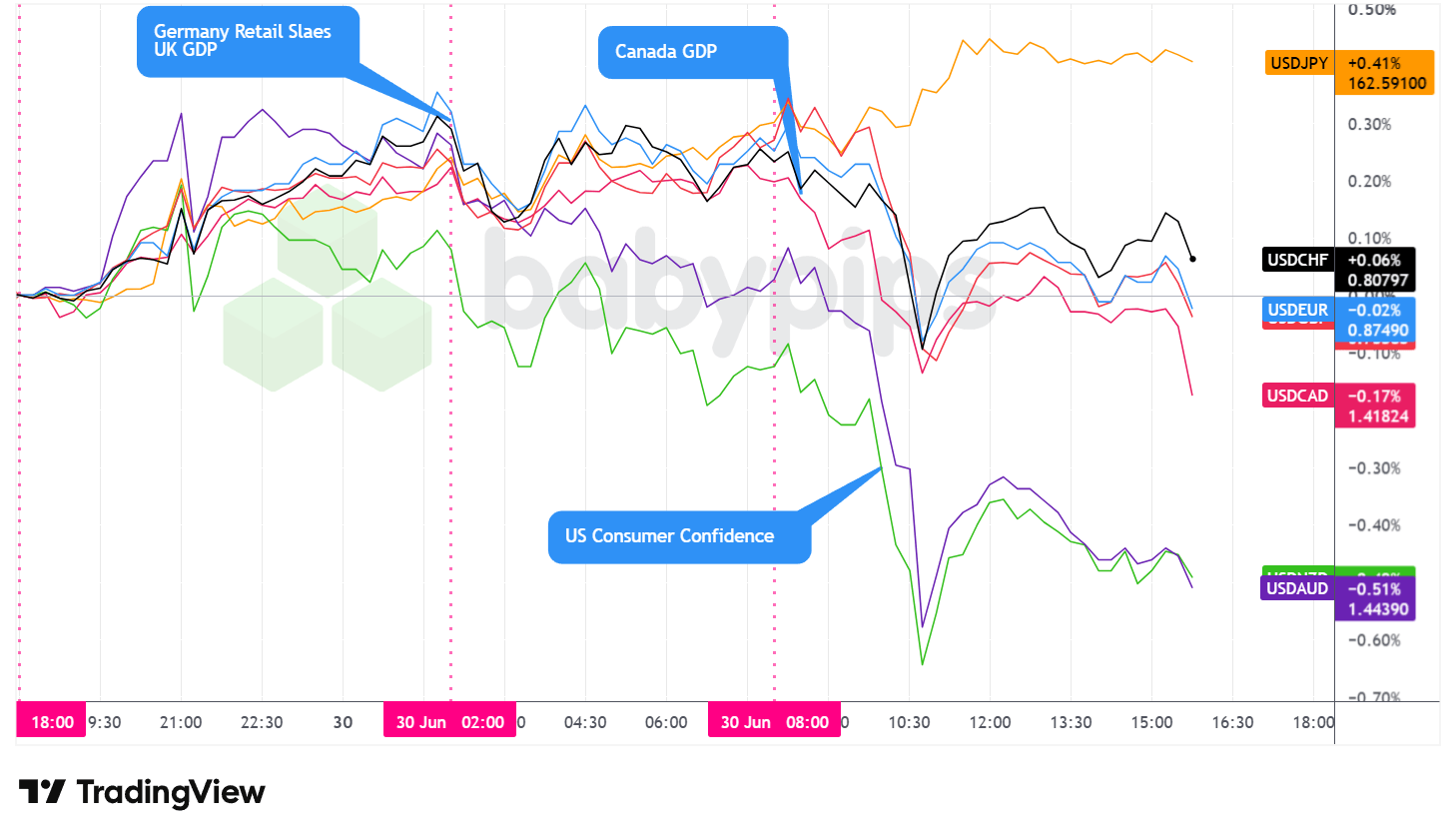

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar traded choppy and mixed through Tuesday, closing arguably neutral to net bearish against the majors. Its one clear win came against the yen, while the Australian and New Zealand dollars led the gainers on the other side.

During the Asian session, the dollar traded net higher against the majors. China’s official PMIs beat across the board, with manufacturing back in expansion and the composite improving, though the strength concentrated in tech-linked export sectors while domestic demand stayed soft. The yen drove the session’s standout move as USD/JPY broke above 162 despite intervention rhetoric from Japanese officials. Minutes from the RBA’s June meeting reaffirmed a tightening bias, with the board signaling willingness to raise the cash rate further if excess demand persists.

The London morning brought mixed trade, and the dollar arguably rebounded on net. Cooler inflation prints out of France and Germany dominated the European data slate, with German retail sales surprising sharply to the upside. ECB Governing Council member Primoz Dolenc, speaking at the forum in Sintra, said a wait-and-see approach until September could be appropriate if energy costs stay subdued, echoing colleagues who pointed toward a likely July pause after this month’s first hike since 2023. The softer inflation backdrop likely kept July hike odds low without sparking a decisive euro move.

After the U.S. session opened, the dollar fell against the majors, then stabilized around the London close before rebounding and trading choppy for the rest of the day. The CB Consumer Confidence miss landed around mid-morning and coincided with the dollar’s sharpest leg lower against the Aussie and Kiwi, though firmer JOLTS and Dallas Fed services data possibly helped the greenback find a floor. Canada’s GDP print came in soft, beating forecasts at the headline for April but slowing from the prior month in the preliminary May read.

At Tuesday’s close, the dollar sat mixed against the majors, arguably neutral to net bearish overall, holding gains on the yen while ceding ground to the commodity currencies.

Promoted: Keep Your Automated Edge Running 24/7.

Your algorithmic strategy shouldn’t rely on your home Wi-Fi. In high-volatility events, execution speed and uptime are what separate a winning backtest from a live market success. ForexVPS provides ultra-low latency, dedicated trading servers that keep your algos executing trades around the clock without interruption. Stop letting connectivity issues erode your edge.

Explore VPS plans at ForexVPS!

Disclosure: To help support our free daily content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- U.S. API Crude Oil Stock Change for June 26, 2026 at 8:30 pm GMT

- Australia AIG Manufacturing Index for June 2026 at 11:00 pm GMT

- Japan Tankan Large Manufacturers Index for June 30, 2026 at 11:50 pm GMT

- ECB Forum on Central Banking

- Japan S&P Global Manufacturing PMI Final for June 2026 at 12:30 am GMT

- Australia Building Permits Prel for May 2026 at 1:30 am GMT

- China RatingDog Manufacturing PMI for June 2026 at 1:45 am GMT

- Japan Consumer Confidence for June 2026 at 5:00 am GMT

- U.K. Nationwide Housing Prices for June 2026 at 6:00 am GMT

- Australia Commodity Prices for June 2026 at 6:30 am GMT

- Swiss Retail Sales for May 2026 at 6:30 am GMT

- Swiss procure.ch Manufacturing PMI for June 2026 at 7:30 am GMT

- S&P Global Manufacturing PMIs Final for June 2026 at various times

- Euro area CPI Growth Rate Flash for June 2026 at 9:00 am GMT

- U.S. Challenger Job Cuts for June 2026 at 9:30 am GMT

- Euro area ECB Lane Speech at 10:15 am GMT

- U.S. MBA 30-Year Mortgage Rate & Applications for June 26, 2026 at 11:00 am GMT

- U.S. Fed Chair Warsh Speech at 11:00 am GMT

- U.S. ADP National Employment Report for June 2026 at 12:15 pm GMT

- Bank of Canada Governor Macklem Speech at 1:00 pm GMT

- European Central Bank President Lagarde Speech at 1:00 pm GMT

- BoE Gov Bailey Speech at 1:00 pm GMT

- Fed Chair Warsh Speech at 1:00 pm GMT

- ECB President Lagarde Speech at 2:00 pm GMT

- U.S. ISM Manufacturing PMI for June 2026 at 2:00 pm GMT

Wednesday’s calendar leans heavily on the labor market and central bank speakers. The euro-area flash CPI lands first and will test the easing trend that France and Germany flagged on Tuesday, with a soft print likely cementing expectations for an ECB pause in July. In the U.S. session, the ADP employment report and ISM Manufacturing PMI offer a read on momentum ahead of Friday’s nonfarm payrolls, while back-to-back appearances from Lagarde, Bailey, Macklem and Fed Chair Warsh give traders plenty of scope for headline-driven volatility.

Stay frosty out there, forex friends!

When equities surge but the dollar stumbles, commodity currencies like the Aussie and Kiwi tell you what’s really happening beneath the surface. Premium members can read our lesson:

📖 Beta Currencies: First to Rally, First to Crack

Reading this helps you understand why commodity currencies rally hardest when risk appetite is strong, how they function as real-time gauges of market mood, and what that tells you about the broader risk environment affecting your trades.

And if you’re not a Premium subscriber yet, consider joining to unlock lessons like this whenever you need them.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just what your chart is showing, but the deeper market dynamics and intermarket relationships driving the move