Oil prices fell sharply on Monday as US-Iran talks in Switzerland produced a 60-day roadmap toward a final deal and Iran resumed crude loadings from its Kharg Island terminal, removing much of the near-term supply risk premium from energy markets. Equity markets faced concentrated pressure from a significant decline in SpaceX shares and broad mega-cap technology weakness, leaving the S&P 500 little changed overall, while the US dollar closed the session as one of the top performing major currencies with gold and Bitcoin also advancing.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Following the lifting of the US Navy blockade, Iran has resumed loading crude from its Kharg island export terminal

- UK Prime Minister Keir Starmer announced his resignation on Monday, laying out a timeline for stepping down that could see Andy Burnham, the Mayor of Greater Manchester, installed as prime minister as soon as July 17.

- ECB President Christine Lagarde told the European Parliament’s ECON Committee that euro‑area inflation is high enough to require attention but not yet severe enough to unanchor expectations or generate harmful second‑round effects

-

Canada CPI Growth Rate for May 2026: 3.2% y/y (2.9% y/y forecast; 2.8% y/y previous); 1.0% m/m (0.6% m/m forecast; 0.4% m/m previous)

- Canada CPI Common for May 2026: 2.7% y/y (2.6% y/y forecast; 2.5% y/y previous)

- Canada CPI Trimmed-Mean for May 2026: 2.0% y/y (2.1% y/y forecast; 2.0% y/y previous)

- Canada Core Inflation Rate for May 2026: 2.2% y/y (2.2% y/y forecast; 2.1% y/y previous); 0.6% m/m (0.5% m/m forecast; 0.2% m/m previous)

- Canada CPI Median for May 2026: 2.1% y/y (2.2% y/y forecast; 2.1% y/y previous)

- Euro area Consumer Confidence Flash for June 2026: -17.7 (-17.0 forecast; -19.0 previous)

Promotion: If your confidence has grown in your market awareness & strategies, and you wanna take action, Maven Trading can help. They provide simulated funding challenges starting as low as $15, allowing you to trade major pairs with professional-sized capital. No time limits mean you can take swing plays on these market themes without the pressure of a ticking clock.

Learn More About Maven Trading Today! And for a limited time: Use code “ETERNAL” for 10% off Challenge fee!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

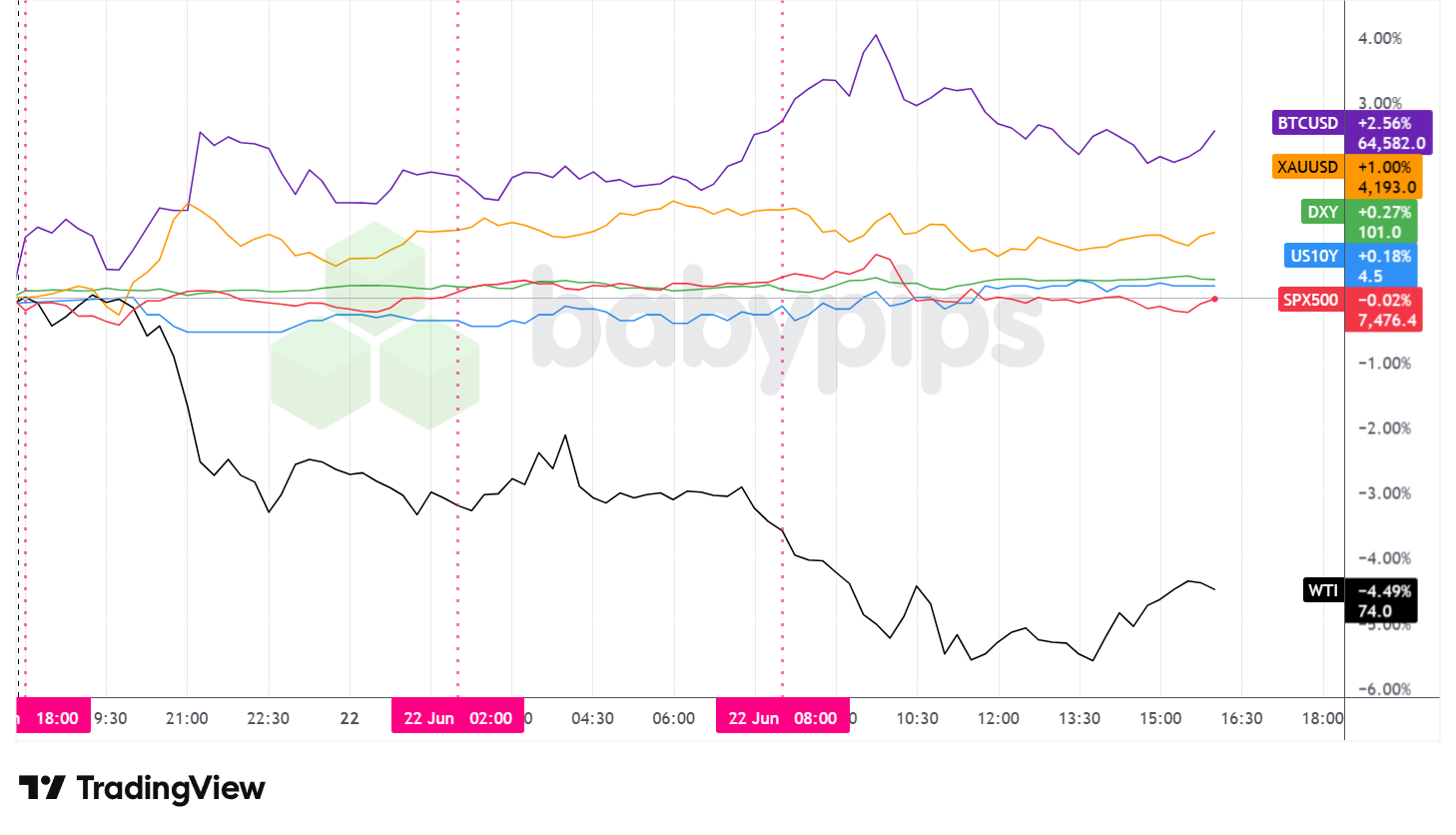

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Monday’s session produced a clear divergence between energy markets and the rest of the asset complex, with oil bearing the full force of diplomatic progress from Switzerland while equities faced a separate and more concentrated source of pressure from the technology sector.

WTI crude oil posted the session’s steepest loss, declining approximately 4.41% to close near $74.10 per barrel. The move lower tracked the evolving news flow from the US-Iran negotiations throughout the day, as the 60-day roadmap was announced, Iran resumed Kharg Island loadings, and Washington issued a license for Iranian oil sales. The prospect of Strait of Hormuz supply returning to global markets at scale appears to have driven the bulk of the decline.

The S&P 500 closed marginally lower, declining roughly 0.08% to approximately 7,472. The index reached intraday highs around the US open before reversing as technology shares came under significant pressure. A roughly 13% decline in SpaceX shares, tied to news of a large investment-grade bond issuance intended to fund the company’s AI infrastructure ambitions, alongside Alphabet’s losses following the announced departure of a prominent Google DeepMind executive, accounted for much of the pullback. Losses remained concentrated in higher-valuation technology names, which helped contain the overall index decline. Modestly rising Treasury yields through the US afternoon may have added a degree of headwind to rate-sensitive equity valuations.

Gold advanced approximately 0.94%, closing near $4,190.70. The precious metal traded in a range through the Asian and London sessions before easing modestly from intraday highs in the US afternoon, though it finished comfortably in positive territory. With no direct gold-specific catalyst apparent, the gain may have reflected a combination of ongoing safe-haven demand and residual uncertainty about the durability of the US-Iran framework, particularly in the absence of Israeli participation in the joint statement.

Bitcoin was the session’s top performer among the assets tracked on the overlay, rising approximately 2.27% to close near $64,400. The cryptocurrency’s advance appeared broadly disconnected from traditional market catalysts, though the improving geopolitical backdrop and its growing role as an alternative store of value during periods of macroeconomic and geopolitical uncertainty may have contributed.

US 10-year Treasury yields edged modestly higher, adding approximately 1 to 2 basis points to close near 4.50%. The contained bond market reaction suggested that neither the geopolitical progress nor the equity market volatility generated a decisive response from fixed income investors, with the modest yield rise possibly reflecting incremental risk repricing as the session developed.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Most trading mistakes aren’t technical—they’re psychological. In the classic “Trading in the Zone” by Mark Douglas (⭐ 4.7★ | 10,000+ reviews on Amazon), you’ll learn how to master the probabilistic thinking and emotional discipline mentioned in today’s article. If you struggle with hesitation or breaking your rules, this is your manual for consistent execution.

Click on the link to learn more about “Trading in the Zone” by Mark Douglas!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

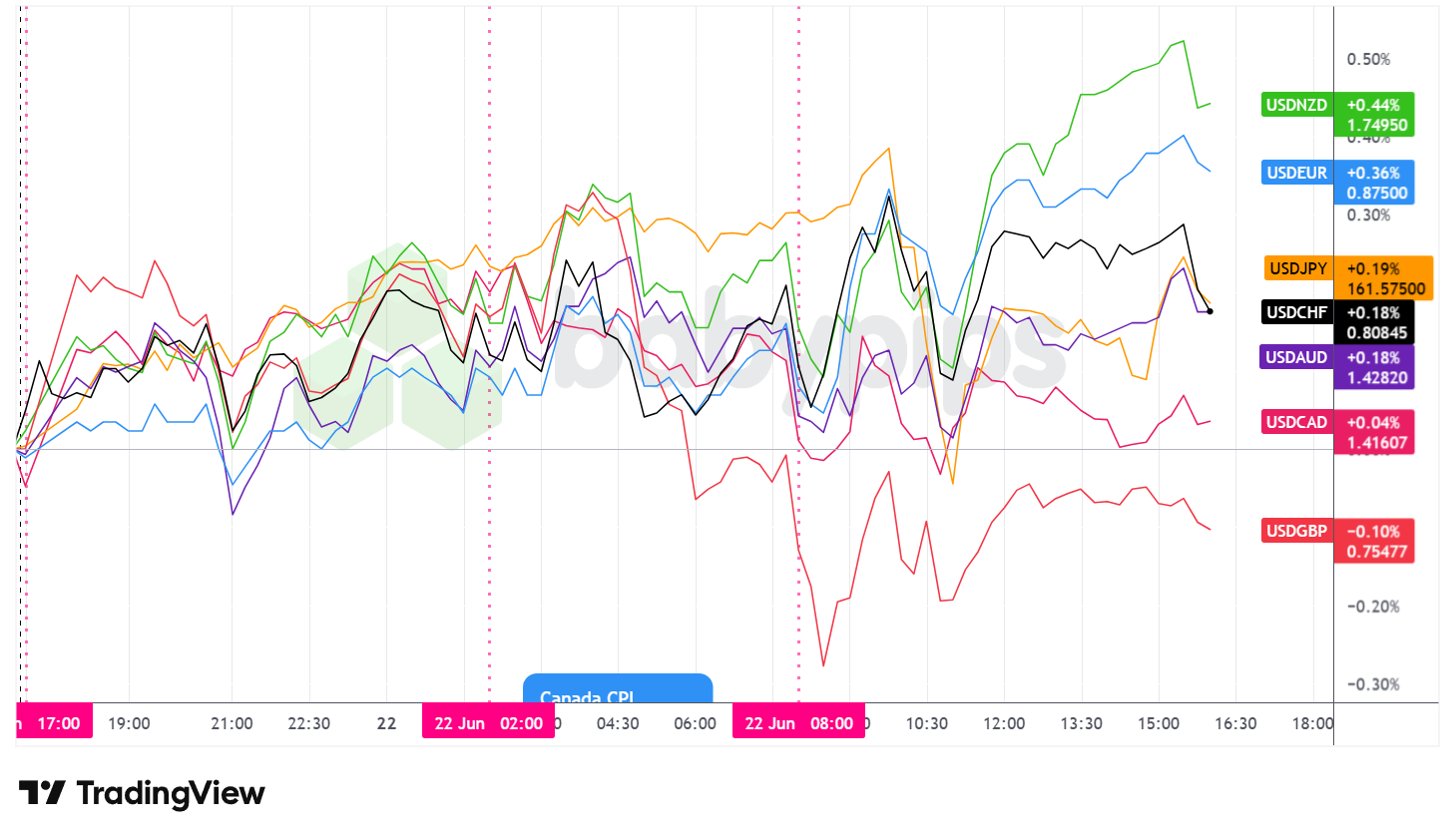

Overlay of USD vs. Majors – Chart Faster With TradingView

The US dollar traded net higher against the major currencies through most of Monday’s session, ultimately closing the day as the top performing major with one exception.

During the Asian session, the dollar traded net higher against the major currencies, with price action that remained choppy rather than cleanly directional as the day’s dominant narrative shifted between concern over Iran’s Strait of Hormuz closure announcement and subsequent improvement in the tone from the Swiss talks. The uncertainty surrounding the early-session geopolitical developments may have supported incremental safe-haven flows into the dollar through the first hours of the new trading week.

The London session brought a shift in momentum. After extending gains around the European open, the dollar stabilized and pulled back modestly against the major currencies through much of the morning. Sterling was the session’s key intra-day mover, recovering from earlier lows as Prime Minister Starmer’s resignation announcement and the clear path toward an uncontested Burnham succession removed a portion of the political uncertainty premium that had weighed on the pound. The broader dollar pullback during the London session may also have reflected improving sentiment as the Swiss joint statement emerged and oil prices continued lower in response to the unfolding diplomatic progress.

During the US session, the dollar traded choppily but maintained an arguably net bullish lean through the rest of the day. The equity market’s reversal from intraday highs, driven by SpaceX’s significant decline and broad technology sector weakness, may have shifted incremental capital flows in a more defensively oriented direction, providing underlying support for the greenback through the US afternoon.

At Monday’s close, the dollar posted net gains against most major currencies, with broadly uniform strength across the European and commodity-linked majors. Sterling was the notable exception, finishing marginally higher against the dollar on the day, likely supported by reduced political uncertainty tied to the Burnham succession and peaceful transfer of power.

Promoted: Day traders & Scalpers have better odds of making great decisions if they see market catalysts right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- Australia S&P Global Manufacturing & Services PMI Flash for June 2026 at 11:00 pm GMT

- Japan S&P Global Manufacturing & Services PMI Flash for June 2026 at 12:30 am GMT

- Swiss Current Account for March 31, 2026 at 7:00 am GMT

- Germany S&P Global Manufacturing & Services PMI Flash for June 2026 at 7:30 am GMT

- Euro area S&P Global Manufacturing & Services PMI Flash for June 2026 at 8:00 am GMT

- European Central Bank Lane Speech at 8:30 am GMT

- U.K. S&P Global Manufacturing & Services PMI Flash for June 2026 at 8:30 am GMT

- Bank of England Breeden Speech at 8:55 am GMT

- U.K. CBI Industrial Trends Orders for June 2026 at 10:00 am GMT

- ADP U.S. Employment Change Weekly for June 6, 2026 at 12:15 pm GMT

- Bank of Canada Governor Macklem Speech at 1:25 pm GMT

- U.S. S&P Global Manufacturing & Services PMI Flash for June 2026 at 1:45 pm GMT

- BoE Taylor Speech at 1:55 pm GMT

- Richmond Fed Manufacturing Index for June 2026 at 2:00 pm GMT

- U.S. Money Supply for May 2026 at 5:00 pm GMT

- Bank of England Dhingra Speech at 5:30 pm GMT

Tuesday’s calendar is headlined by a global sweep of flash PMI data spanning Australia, Japan, Germany, the euro area, the UK, and the US, offering the first read on June business conditions against the backdrop of the ongoing Strait of Hormuz situation.

The ECB Lane speech at 8:30 am GMT arrives with markets still processing Monday’s Parliamentary committee commentary from President Lagarde, and any further signal on the near-term rate path could drive euro-area currency and rate moves.

Multiple Bank of England speakers, including Breeden at 8:55 am GMT, Taylor at 1:55 pm GMT, and Dhingra at 5:30 pm GMT, take on added significance given the UK’s ongoing political transition and the need for policy clarity from the central bank.

Bank of Canada Governor Macklem speaks at 1:25 pm GMT following the above-forecast May inflation print, and any shift in his tone could be relevant for the direction of Canadian rate expectations.

The API crude oil inventory report at 8:30 pm GMT will be watched closely as markets continue to assess the supply implications of a potential Strait of Hormuz reopening following Monday’s Iran deal developments.

Stay frosty out there, forex friends!

When a geopolitical event shifts market risk appetite, currencies respond in complex patterns that aren’t always obvious from price action alone. Premium members can read our lesson:

📖 Risk-On / Risk-Off: How Global Mood Moves Currencies

Reading this helps you understand how risk appetite drives currency flows, which currencies benefit when traders embrace risk versus when they retreat to safety, and how to read the market’s appetite for risk before placing a trade.

And if you’re not a Premium subscriber yet, consider joining.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand the mechanics driving currency flows when market sentiment shifts, giving you the edge to anticipate moves before they happen.