Thursday’s session delivered one of the more dramatic intraday reversals since the U.S.-Iran conflict began, with markets spending the morning in cautious, range-bound trade before a sharp pivot in the early North American afternoon. President Trump’s announcement that he was canceling planned strikes against Iran and that a peace agreement could be signed within days triggered a synchronized repricing that sent equities surging, crude oil tumbling to session lows in the mid-$80s, and the U.S. dollar broadly lower. Gold and Bitcoin joined the rally, even as a hotter-than-expected core producer price report from earlier in the session served as a reminder that underlying inflation pressures had not yet eased.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- U.S. forces launched a second consecutive night of strikes against Iran; CENTCOM confirmed operations targeting multiple sites at the direction of the Commander in Chief

- U.K. RICS House Price Balance for May 2026: -35.0% (-30.0% forecast; -34.0% previous)

- Japan BSI Large Manufacturing for Q2 2026: -1.8% q/q (4.0% q/q forecast; 3.8% q/q previous)

- Australia Consumer Inflation Expectations for June 2026: 5.5% (6.5% forecast; 5.6% previous)

- Euro area ECB Interest Rate Decision for June 11, 2026: 2.4% (2.4% forecast; 2.15% previous)

- Euro area Deposit Facility Rate for June 11, 2026: 2.25% (2.25% forecast; 2.0% previous)

- Euro area Marginal Lending Rate for June 11, 2026: 2.65% (2.65% forecast; 2.4% previous)

- Canada Building Permits for April 2026: -7.6% m/m (-5.0% m/m forecast; 10.3% m/m previous)

- Germany Current Account for April 2026: 13.8B (20.2B forecast; 23.6B previous)

- U.S. Initial Jobless Claims for June 6, 2026: 229.0k (219.0k forecast; 225.0k previous)

- U.S. PPI for May 2026: 6.5% y/y (6.8% y/y forecast; 6.0% y/y previous); 1.1% m/m (0.7% m/m forecast; 1.4% m/m previous)

- Iran declared the Strait of Hormuz closed to all vessels following the overnight U.S. attacks; CENTCOM disputed the announcement, stating commercial ships were continuing to transit the waterway

- President Trump canceled planned military strikes against Iran, posting that negotiations had been “brought to the highest level of Iranian leadership”; Trump later told reporters in the Oval Office that a deal signing could take place as soon as this weekend in Europe, with Vice President JD Vance in attendance

Have a solid trading strategy but lack the capital? FundedNext empowers disciplined traders by providing simulated trading accounts up to $200K.

Unlike other prop firms, FundedNext imposes no artificial time limits on challenges. You even earn a unique 15% profit share during your evaluation! Once funded, you keep up to a 95% profit split with guaranteed 24-hour payouts. Trade CFDs or Futures your way—even during major news events.

Join over 400K traders who have received $300M+ in payouts. Ready to back your edge?

Learn More About FundedNext! Limited time offer: Use code BPFN for discounts on both CFD & Futures plans! T&C apply. T&C apply.Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

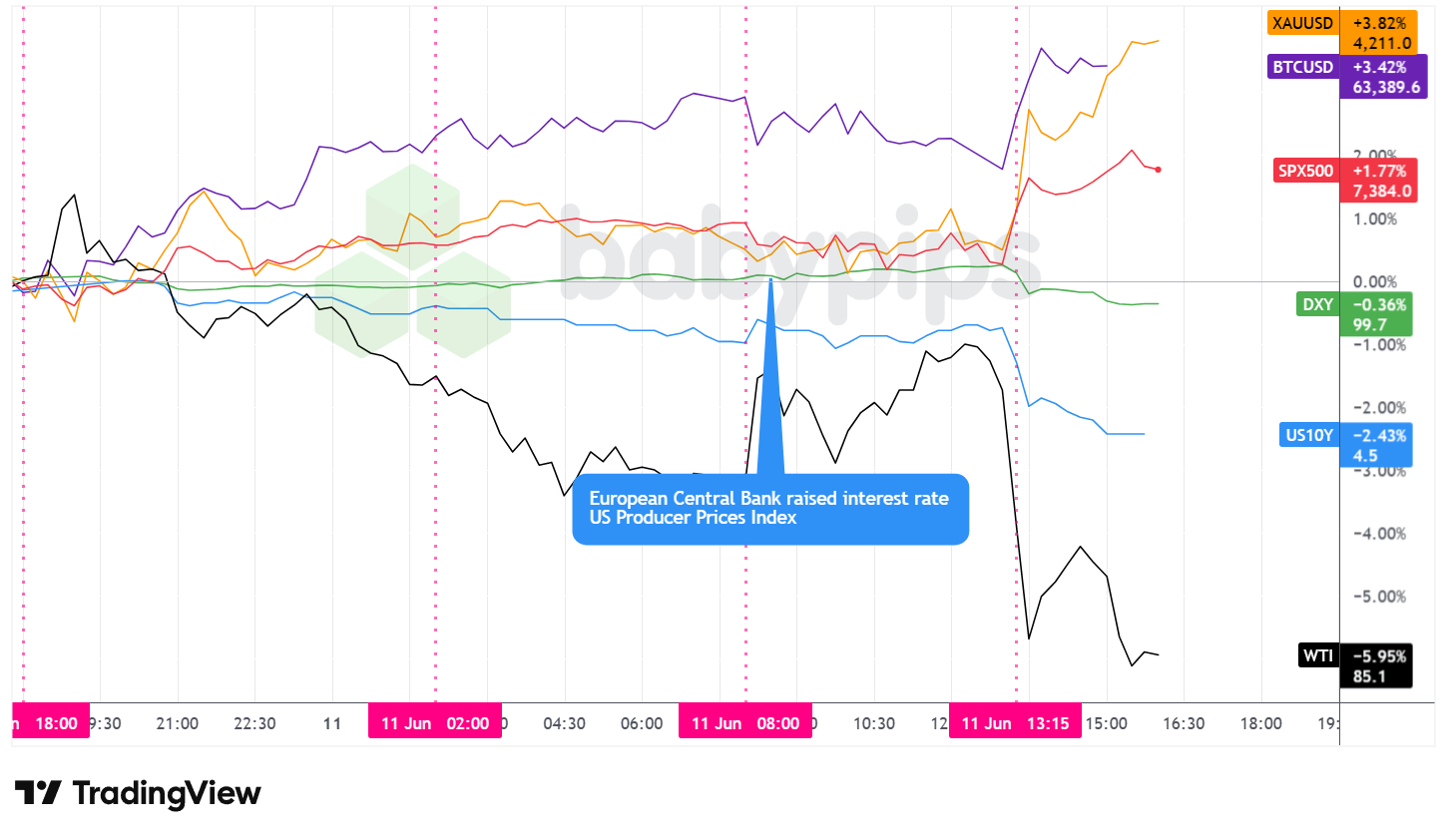

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Thursday unfolded in two clearly delineated phases. The first, spanning the Asian and most of the London session, was defined by cautious, contained trading across major asset classes. Markets absorbed the news of a second consecutive night of U.S. strikes against Iran, a development that had been partially telegraphed in advance by the administration and appeared largely priced in by the time trading was underway. The second phase arrived in the early afternoon in New York, when President Trump announced he was canceling planned additional strikes and signaling that a deal with Tehran may be within reach. That single development drove a sharp and broadly synchronized repricing across every major asset class.

WTI crude oil fell approximately 5.95% to close near $85.10, registering the session’s largest single-asset decline. Oil had already been trending lower through the Asian and London hours, possibly reflecting the degree to which the second wave of strikes had been anticipated. The sharper leg lower, from near $89 in the early New York session through the mid-$80s, correlated closely with Trump’s afternoon reversal. Iran had claimed the Strait of Hormuz was fully closed, a claim CENTCOM disputed by noting continued commercial transit, and markets ultimately appeared to anchor on Trump’s diplomatic signal rather than the contested closure claim when pricing direction.

The S&P 500 snapped a two-session losing streak, gaining approximately 1.77% to close near 7,384. The index had ranged relatively tightly through the Asian and London hours before a modest pullback in the early U.S. session, possibly reflecting some caution around the morning’s above-forecast core producer price data. The afternoon surge aligned with the Trump deal signal and was accompanied by notably strong gains in technology-adjacent shares. SpaceX’s completion of the largest IPO in history, raising $75 billion at $135 per share, likely added to positive sentiment within the technology space through the session.

Gold was arguably the day’s most notable performer relative to the session’s prevailing risk-on tone, rising approximately 3.82% to close near $4,211. The advance in the context of a broad equity rally and sharp oil decline may point to a combination of drivers: the U.S. dollar’s sharp broad-based decline likely boosted demand for the dollar-denominated metal from international buyers, while the persistently elevated core producer price reading reinforced concerns that inflationary pressures extend well beyond the energy sector. The fact that gold rallied alongside falling oil may also reflect that some participants remained skeptical about the finality of the Iran situation, given Tehran’s denial that any agreement text had been approved.

Bitcoin gained approximately 3.42% to close near $63,390. The cryptocurrency had trended higher through the Asian session before consolidating in the London and early U.S. hours. Its afternoon surge tracked the equity and gold rallies closely, consistent with its recent pattern of responding to broad shifts in risk appetite.

The 10-year U.S. Treasury yield declined approximately 2.43%, settling near 4.50%. The bond market’s move lower despite the morning’s above-forecast core producer price data suggests markets may have been looking ahead to a potential easing in energy-driven inflation should the Strait of Hormuz reopen following a deal. The core PPI beat had created some hawkish pressure earlier in the session, but the afternoon oil crash and the prospect of reduced supply disruptions appeared to dominate the bond market’s forward-looking calculus. The June 17 FOMC meeting remains close, and the afternoon’s yield decline may partly reflect some easing in near-term rate hike expectations.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Today’s wild intraday swings in oil and the rapid recovery in equities prove just how fast a geopolitical headline can flip the market. When price action reverses on a dime due to sudden comments from leaders, knowing the fundamentals isn’t enough—you need the psychological discipline to stick to your plan without panicking.

In “Unknown Market Wizards,” (⭐ 4.6★ | 1,400+ reviews on Amazon) Jack Schwager interviews under-the-radar trading pros to reveal what truly separates them from the pack: unbreakable mental resilience and rigid risk control. Learn how top traders stay clinical, manage their exposure, and execute flawlessly when the rest of the market is swept up in the emotion of geopolitical chaos.

Master Your Trading Mindset with Market Wizards!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

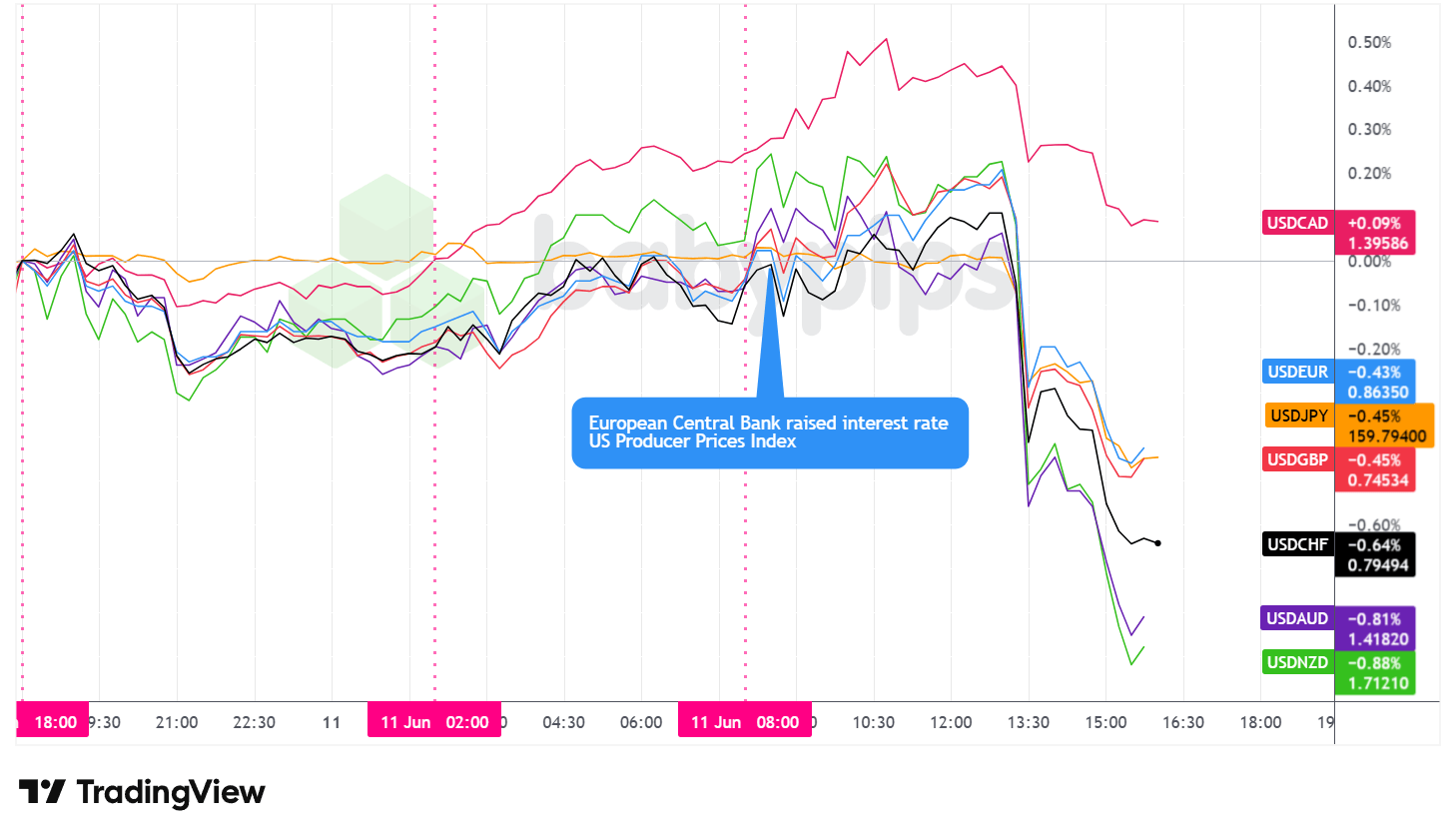

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar closed lower against nearly every major currency on Thursday, with only the Canadian dollar bucking the trend. The session’s definitive FX story was the afternoon reversal: a sharp, broad-based dollar selloff that erased the greenback’s measured gains from the London session and pushed most pairs to day’s extremes.

During the Asian session, the dollar traded with low volatility and largely sideways, carrying a modest net bearish bias throughout. No significant regional economic releases provided directional impulse, and the FX market’s posture mirrored the broader wait-and-see tone across asset classes as traders sized up the overnight escalation in U.S.-Iran hostilities.

From the London open, the dollar shifted into a gradual net upward drift against most of its major peers, building steadily through the European morning and into the early North American window. The move appeared consistent with a combination of positioning ahead of the day’s key scheduled risk events and residual safe-haven demand as the geopolitical situation remained unresolved. The European Central Bank delivered its widely expected rate hike at its June meeting, with the outcome landing fully in line with market forecasts. With no surprise element in the decision, the EUR response was limited, and the dollar maintained its composed advance through the London session.

The early U.S. session was shaped by the May producer price report, which presented a nuanced picture. The headline annual figure came in below forecast, while the monthly reading posted a significant beat. The core measure stripping food, energy, and trade services from the index accelerated to a multiyear high on an annual basis and posted its largest monthly gain in several years, well above expectations. The initial dollar reaction was indecisive, with the greenback holding most of its London gains in the immediate post-data window as markets appeared to weigh the mixed headline result against the stronger core reading.

The session’s defining FX move arrived in the early afternoon, when President Trump’s announcement of canceled strikes and a potentially imminent deal triggered a swift and broad-based dollar selloff. Risk appetite improved sharply, and safe-haven positioning in the USD unwound.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Today’s daily recap highlights a market driven geopolitical developments and shifts in Fed policy expectations. But as any pro will tell you, understanding market drivers can aren’t enough if the trader lacks the discipline to execute a solid plan on it.

In “Unknown Market Wizards,” (⭐ 4.6★ | 1,400+ reviews on Amazon) Jack Schwager interviews successful traders to reveal a common truth: their edge isn’t just knowledge or skills—it’s their psychological resilience and rigid risk control. Whether you’re navigating shifting geopolitical themes or top tier economic data, learn how the “wizards” stay clinical and execute when the rest of the market is emotional.

Master Your Trading Mindset with Market Wizards!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- New Zealand Business NZ PMI for May 2026 at 10:30 pm GMT

- New Zealand Visitor Arrivals for April 2026 at 10:45 pm GMT

- Japan Industrial Production MoM Final for April 2026 at 4:30 am GMT

- U.K. GDP for April 2026 at 6:00 am GMT

- U.K. Industrial & Manufacturing Production MoM for April 2026 at 6:00 am GMT

- U.K. Balance of Trade for April 2026 at 6:00 am GMT

- China Monetary Developments for May 2026

- Canada New Motor Vehicle Sales for April 2026 at 12:30 pm GMT

- U.S. Michigan Inflation Expectations Prel for June 2026 at 2:00 pm GMT

- U.S. University of Michigan Consumer Sentiment Index for June 2026 at 2:00 pm GMT

Friday’s early London window brings a cluster of U.K. April data led by the GDP print, arriving alongside industrial and manufacturing production figures. The reading will be assessed against the backdrop of ongoing Bank of England rate deliberations and Thursday’s miss in RICS house prices.

In the North American afternoon, the University of Michigan’s preliminary consumer sentiment index and inflation expectations survey carry elevated significance given Thursday’s above-forecast core producer price reading. Any sign that U.S. consumers are anchoring higher near-term price expectations ahead of the June 17 FOMC meeting could reintroduce hawkish rate repricing. Ongoing U.S.-Iran diplomatic developments remain the session’s wildcard, with Trump having flagged a potential deal signing as early as this weekend.

Stay frosty out there, forex friends!

Thursday’s dramatic intraday reversal shows what happens when geopolitical headlines shift safe-haven positioning in a matter of hours. Premium members can read our lesson:

📖 Geopolitical Risk, Trade Policy, and Safe Haven Flows

Reading this helps you understand how geopolitical announcements trigger immediate currency repricing, which safe-haven currencies to watch when risk sentiment shifts, and why the dollar doesn’t always move the way you’d expect when market mood changes.

And if you’re not a Premium subscriber yet, now’s a good time to sign up.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just what the headlines say, but how they move currencies, which safe havens traders rotate into, and why the same geopolitical event creates opposite effects on different currencies.