Greetings, forex friends! It’s the first week of the month, which means we’ve got another NFP report coming our way this Friday at 12:30 pm GMT. There’s therefore a good chance that the Greenback may get a volatility infusion.

And as usual, I’ve got another edition of my Event Preview to help y’all get up to speed on what happened last time and what we can expect this time around.

What happened last time?

- Feb. non-farm payrolls: +313K vs. +200K expected

- Jan. non-farm payrolls: upgraded from +200K to +239K

- Dec. non-farm payrolls: upgraded from +160K to +175K

- Average hourly earnings m/m: +0.1% vs. +0.2% expected, +0.3% previous

- Jobless rate: steady at 4.1% vs. 4.0% expected

- Labor force participation rate: 63.0% vs. steady at 62.7%

Last time around, I noted in my Event Preview for the February NFP report that leading indicators were leaning more towards a slowdown in jobs growth. However, I pointed out that this goes against historical trends. Moreover, I highlighted that there’s a historical tendency for jobs growth to come in better-than-expected. But at the same time, there’s also a historical tendency for wage growth to disappoint.

Well, the February NFP report later revealed that historical tendencies won out over the leading indicators.

As for specifics, non-farm payrolls increased by 313K, much more than the expected 200K increase.

Even better, the reading for January was upgraded from +200K to +239K. Better still, December’s reading was also upgraded from +160K to +175K. All those upgrades mean that 54K more jobs were created than originally estimated, which is great.

Despite the stronger jobs growth, the jobless rate held steady at 4.1% instead of improving to 4.0% as expected. No worries, though, since the labor force participation rate jumped from 62.7% to a five-month high of 63.0%.

And since the jobless rate didn’t budge, then that means that the U.S. economy was able to absorb the influx of new and returning workers, which is also great.

So far, so good, right? Unfortunately, historical tendencies also held true with regard to wage growth since average hourly earnings only grew by 0.1% month-on-month, slowing down from January’s +0.3% and missing the consensus for a 0.2% increase. Year-on-year, this translates to a 2.6% increase, which is a three-month low.

To sum up, non-farm payrolls surprised to the upside, which is why the the Greenback’s knee-jerk reaction was to jump higher.

However, I also mentioned in my previous Event Preview that newly-minted Fed Chair Powell said that he wants to see more wage increases, so I warned y’all that traders will likely have their eyes on wage growth. And since wage growth failed to impress, that induced sellers to attack, sending the Greenback lower on most pairs after the initial reaction.

Overlay of USD Pairs: 15-Minute Forex Chart

What can we expect this time?

- Non-farm payrolls: +190K vs. +313K previous

- Jobless rate: 4.0% vs. 4.1% previous

- Average hourly earnings m/m: 0.3% expected vs. 0.1% previous

For this Friday’s NFP report, the consensus among economists is that the U.S. economy generated around 190K non-farm jobs in March, which is a slower rate of job creation compared to the impressive 313K jobs generated back in February.

Anyhow, most economists think that this is enough to push the jobless rate lower from 4.1% to 4.0%. As for wage growth, the consensus is that wage growth picked up the pace in March since it’s expected to come in at +0.3% (+0.1% previous).

So, what do the leading labor indicators have to say?

- Markit’s manufacturing PMI report noted that “The rate of job creation remained strong, albeit dipping to a four-month low.” Markit also reported that input price inflation “accelerated to the fastest since November 2012.” However, the main driver was higher raw material costs due to the tariffs.

- ISM’s manufacturing PMI report corroborates Markit’s findings since the employment sub-index deteriorated from 59.7 to 57.3. Like Markit, ISM also reported higher input prices, which ISM also attributed to higher raw material prices.

- Markit’s services PMI report found that “Service providers registered a strong rate of job creation that was the fastest since August 2017.” Moreover, input prices increase and “A number of survey respondents stated that the increase in input prices stemmed from higher fuel and wage costs.”

- ISM’s non-manufacturing PMI report supports Markit’s findings since it employment sub-index improved from 55.0 to 56.6. Also, the prices sub-index slightly improved from 61.0 to 61.5. ISM was silent on what drove the higher reading, though.

- The ADP report revealed that private non-farm payrolls increased by 241K in March, beating expectations for a 208K increase but is slightly slower compared to the previous month’s 246K increase.

The leading labor indicators are mixed once again since the manufacturing sector reported weaker jobs growth while the non-manufacturing sector saw faster jobs growth.

The non-manufacturing sector is the main jobs generator in the U.S. economy, though, so jobs growth likely accelerated, which is contrary to the consensus that jobs growth slowed down.

Interestingly enough, the ADP report is actually the odd one out since it reported weaker jobs growth in the service sector and stronger jobs growth in the manufacturing sector, which contradict both the Markit and ISM PMI reports.

Another interesting bit is that Markit noted that higher input prices in the service sector was partially driven by higher wages, which is in-line with the consensus that wage growth picked up the pace.

What about historical tendencies? do they offer any clues?

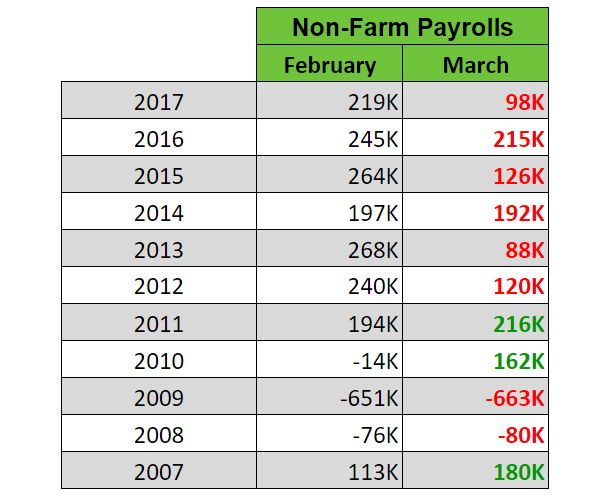

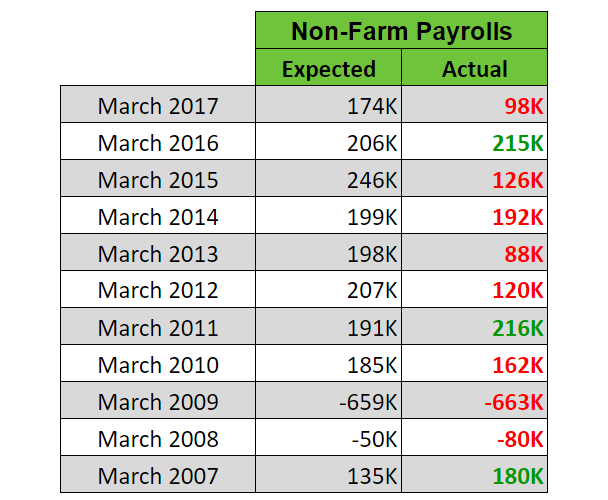

Well, historical trends apparently support the consensus that jobs growth in March slowed down.

Even so, economists still tend to be too optimistic with their guesstimates, resulting in more downside surprises.

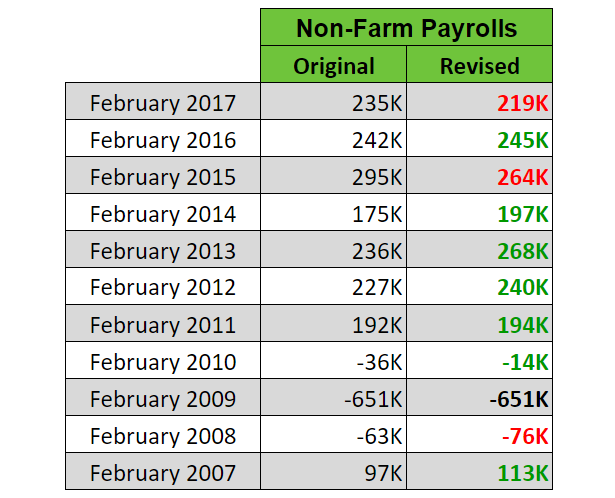

On a happier note, the February reading usually gets an upgrade.

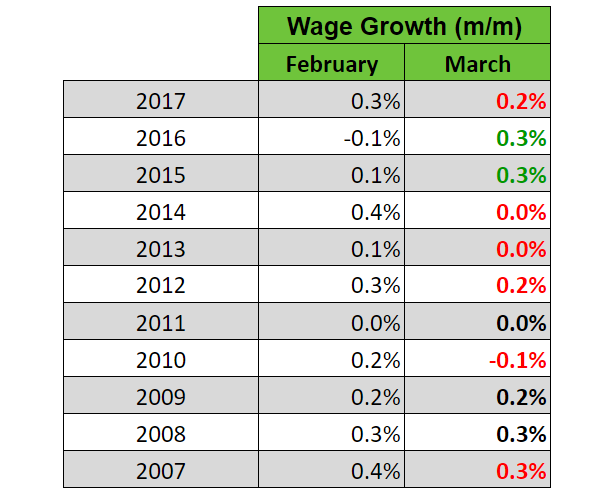

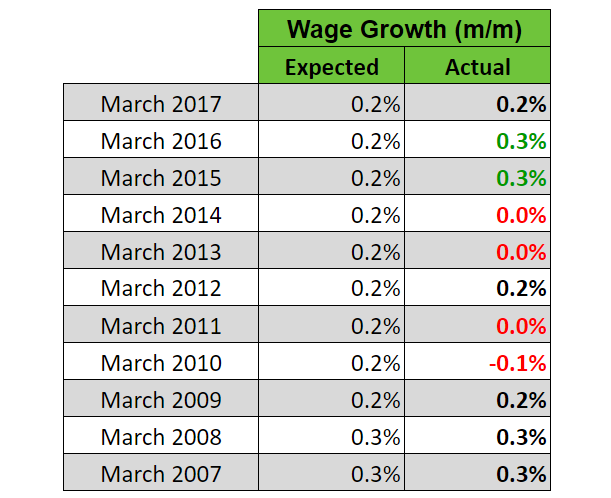

As for wage growth, that tends to slow between the months of February and March, which goes against the consensus that jobs growth accelerated.

There’s are no clear historical tendencies when it comes to how economists fare with their guesstimates, though.

To summarize, the leading labor indicators are mixed but lean more towards faster jobs growth in the service sector, which likely points to stronger overall jobs growth in March.

That’s not in-line with the consensus that jobs growth slowed, though.

Still, the ADP report does seem to support the consensus since it reported weaker jobs growth in the service sector and weaker (yet solid) jobs growth overall.

Also, Markit reported stronger wage growth in the service sector. And that likely means stronger wage growth as well, which is in-line with the consensus view.

Historical tendencies, meanwhile, seem to support the consensus for weaker jobs growth. Moreover, historical data also show that economists tend to overshoot their guesstimates, resulting in more downside suprises.

And that skews probability more towards a downside surprise, at least with regard to jobs growth.

As for wage growth, there’s no clear historical tendency for that.

As always, just keep in mind that we’re playing with probabilities here, so there’s no guarantee that we’ll get a downside surprise for jobs growth.

At any rate, just keep in mind that traders usually have their sights on jobs growth, with a better-than-expected reading usually triggering a Greenback rally while a miss usually causes the Greenback to tank.

However, make sure to also keep an eye on wage growth since that will likely dictate follow-through buying or selling. And last month’s selling pressure after the initial knee-jerk reaction is an example of this.

Also, just keep an eye and ear out for trade-related news since the Greenback’s price action has recently been affected by the trade tensions between the U.S. and China.

Okay, that’s about it. Oh, if news trading ain’t your thing or if high volatility makes you uncomfortable, then remember that you always have the option to sit on the sidelines and wait for things to settle down.