Peace deal optimism between the U.S. and Iran defined Wednesday’s session, sending WTI crude oil down more than 7%, lifting U.S. equities to fresh all-time highs, and pushing the dollar broadly lower against major currencies. Reports of a potential framework agreement to gradually reopen the Strait of Hormuz, alongside a coordinated shift in tone from senior Washington officials, powered one of the more decisive risk-on moves seen since the conflict began in late February.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

-

New Zealand Employment Change for Q1 2026: 0.2% q/q (0.3% q/q forecast; 0.5% q/q previous)

- New Zealand Unemployment Rate for Q1 2026: 5.3% (5.3% forecast; 5.4% previous)

- Australia AIG Manufacturing Index for April 2026: -27.9 (-30.0 forecast; -27.9 previous)

- China RatingDog Services PMI for April 2026: 52.6 (52.5 forecast; 52.1 previous)

- Axios reported, and was subsequently confirmed by a Pakistani diplomatic source cited by Reuters, that the U.S. and Iran are nearing a framework agreement that would gradually reopen the Strait of Hormuz and lift the American naval blockade on Iranian ports

- Euro area S&P Global Services PMI Final for April 2026: 47.6 (47.4 forecast; 50.2 previous)

- Germany S&P Global Services PMI Final for April 2026: 46.9 (46.9 forecast; 50.9 previous)

- U.K. S&P Global Services PMI Final for April 2026: 52.7 (52.0 forecast; 50.5 previous)

- Euro area PPI for March 2026: 2.1% y/y (1.6% y/y forecast; -3.0% y/y previous); 3.4% m/m (3.0% m/m forecast; -0.7% m/m previous)

- U.S. MBA 30-Year Mortgage Rate for May 1, 2026: 6.45% (6.37% previous)

- U.S. ADP National Employment Report for April 2026: 109.0k (70.0k forecast; 62.0k previous)

- Canada Ivey PMI s.a for April 2026: 57.7 (50.0 forecast; 49.7 previous)

- U.S. EIA Crude Oil Stocks Change for May 1, 2026: -2.31M (-6.23M previous)

- President Trump posted on social media that the U.S. will end its military campaign and lift the Hormuz blockade “assuming Iran agrees to give what has been agreed to,” adding “if they don’t agree, the bombing starts.”

- Trump also confirmed that Project Freedom, the U.S. mission to escort commercial vessels through the Strait of Hormuz, has been paused as a confidence-building measure while deal talks continue.

- Fed Bank of Chicago President Austan Goolsbee warned against reflexively cutting interest rates in anticipation of AI-driven productivity gains, noting that pre-emptive easing tied to expected future growth can push up inflation rather than ease it.

Promoted: Day traders & Scalpers have better odds of making great decisions if they see market catalysts right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

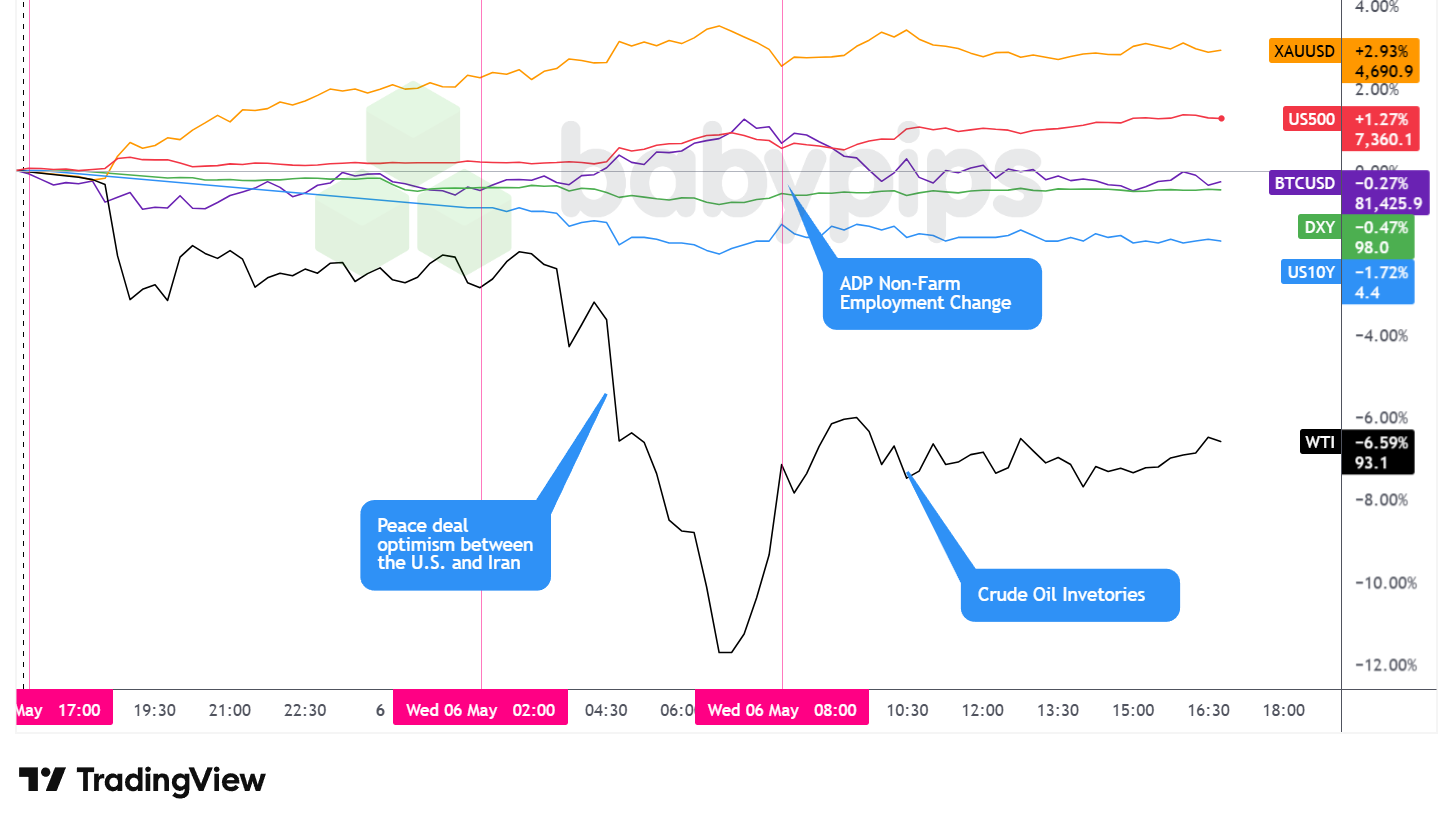

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Wednesday’s session was defined almost entirely by geopolitical relief. The combination of coordinated de-escalatory signals from senior U.S. officials and circulating reports of an Iran deal framework sent the geopolitical risk premium in oil prices sharply lower, while risk assets broadly surged. The session was further supported by an AMD-led chipmaker rally following Tuesday’s after-hours earnings beat and a significantly stronger-than-expected ADP employment print.

WTI crude oil was the session’s most dramatic mover, falling 7.05% to close near $92.50 per barrel. Oil had already begun retreating during Tuesday’s late session on de-escalatory comments from Defense Secretary Hegseth, Secretary of State Rubio, and Joint Chiefs Chairman General Caine, and selling accelerated sharply during the London session as the Axios report on a potential framework agreement circulated. WTI touched a low near $87 intraday before recovering sharply after the U.S. market open, stabilizing in a $92-$93 range through the afternoon as the broad contours of the deal remained uncertain. The magnitude of the decline likely reflects the significant risk premium that had built into crude prices since U.S.-led strikes on Iran in late February.

Gold surged 3.17% to close at $4,695.00. The precious metal climbed steadily from the Asia session open, advancing through both the London and early U.S. sessions before paring slightly into the close. Gold’s simultaneous advance alongside equities and falling oil may reflect a combination of broad dollar weakness and some residual uncertainty about whether the proposed framework will hold, with its dual role as a dollar hedge and a geopolitical barometer possibly both contributing to the session’s gains.

The S&P 500 advanced 1.24% to close at 7,361.7, reaching fresh all-time highs during the session. Price action was subdued during the Asian overnight hours before accelerating sharply higher around the early London session as Iran deal headlines spread and U.S. equity futures built on overnight gains. AMD-led chipmaker strength following a strong earnings beat provided an additional equity-specific tailwind. The index briefly touched a session high near 7,369 in the early afternoon before settling slightly lower into the close.

The 10-year Treasury yield declined approximately 6 basis points to close around 4.357%. The move likely reflected reduced expectations for Fed tightening as lower oil prices eased near-term inflation risk, with Bloomberg noting that “bets on Federal Reserve rate hikes receded” alongside falling crude. Fed officials Goolsbee and Musalem both spoke during the session, each flagging inflation as the more prominent risk, but neither appeared to materially shift market pricing on the day given the dominance of the geopolitical narrative.

Bitcoin closed fractionally higher, up 0.18% to $81,538.80, after a notable intraday round-trip. The cryptocurrency rallied from roughly $81,000 to a peak near $82,811 during the London session, possibly riding the broader risk-on momentum, before surrendering most of those gains through the U.S. afternoon. Bitcoin’s muted net performance relative to equities and gold suggested it did not participate fully in the risk-on theme for the day.

Promoted: Capitalize on Geopolitical Volatility Without Risking Your Own Funds.

Rising odds of an end to conflict in the Middle East sent oil falling on the session. When the macroeconomic data shifts this fast, trading the volatility requires deep focus—and enough capital to make your edge count.

If you have the right fundamental bias but a restrictive personal account size, Funded Trading Plus can help. They offer evaluation packages starting at just $89.00, with static drawdowns, news trading, and weekend holding allowed!

Learn more about Funded Trading Plus!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

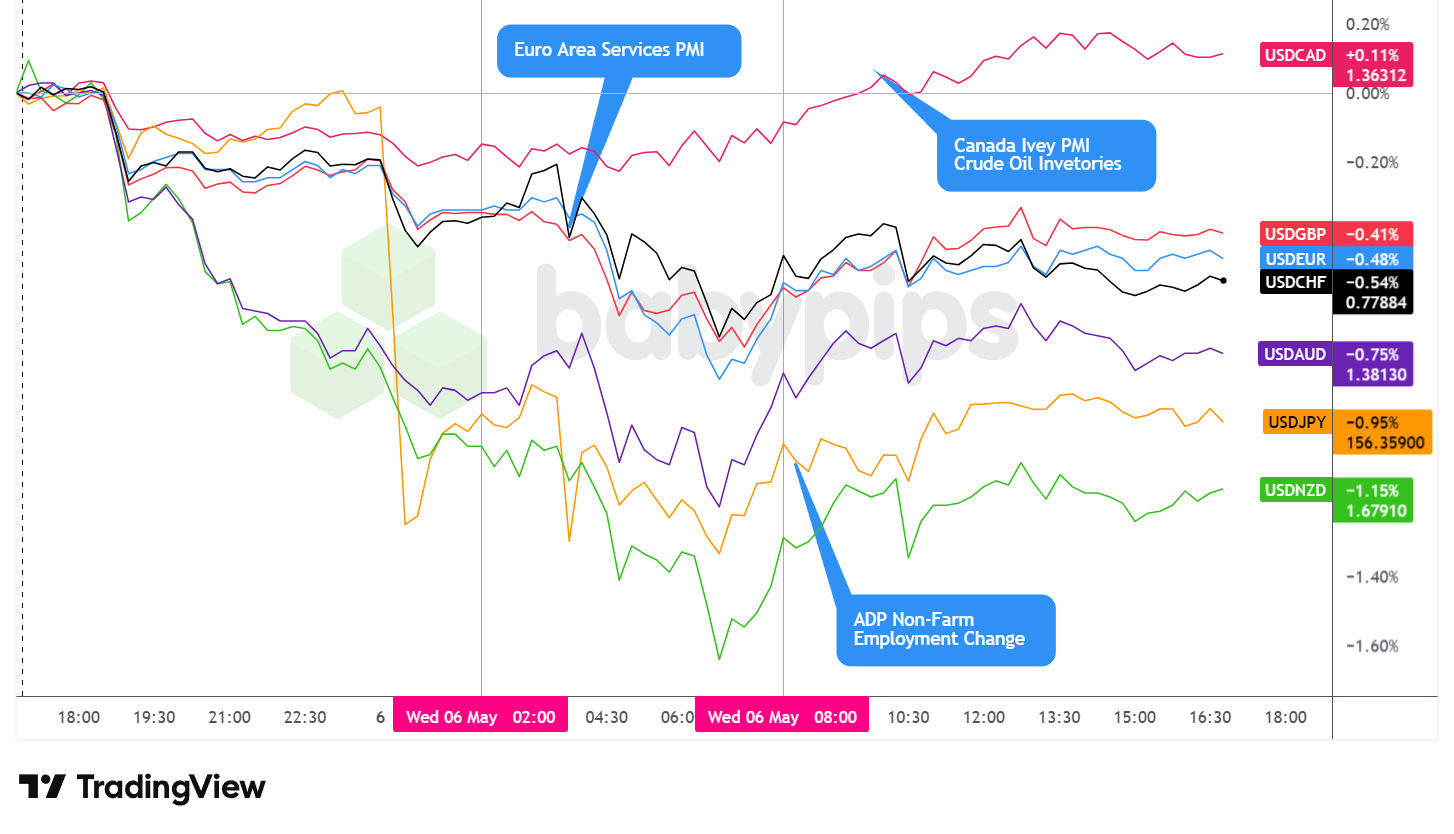

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar traded broadly lower on Wednesday, pressured by a sustained risk-on tone tied to U.S.-Iran peace deal developments. The greenback fell steadily from the Asia session open until roughly one hour before the U.S. session opened, before partially recovering and trading choppy and mostly sideways through the afternoon. At the Wednesday close, the dollar was a net underperformer against all major currencies in the basket, recording a gain only against the Canadian dollar.

During the Asian session, the dollar came under immediate and broad selling pressure as markets absorbed the overnight shift in tone from senior U.S. officials on the Iran conflict. Risk-sensitive currencies led the advance, with the Australian dollar notching a fresh four-year high against the USD and the New Zealand dollar reaching its strongest level in two months. Despite Japan’s markets remaining closed for an extended holiday period, USD/JPY still moved notably lower during the session (more intervention action?). The DXY declined from roughly 98.30 to approximately 97.89 during this period as the greenback tracked lower across the board. China’s RatingDog Services PMI came in above estimates at 52.6, and the Composite PMI beat significantly at 53.1, adding a further layer of positive risk tone and reinforcing the domestic demand resilience narrative for Chinese assets.

The London session brought a second and sharper leg of dollar weakness as the Axios report on a potential framework agreement published, followed by Pakistan’s confirmation of the reporting via Reuters and Iran’s navy announcing new Strait of Hormuz transit protocols. The DXY extended to a session low near 97.63. Notably, the final April Services PMIs for France (46.5), Germany (46.9), and the broader eurozone (47.6) all printed in contraction territory and each declined markedly from prior readings, a combination that would ordinarily weigh on the euro. Instead, the EUR strengthened alongside the broader anti-dollar move, suggesting the geopolitical narrative dominated any conventional data-driven reactions during this window. The U.K.’s Services PMI was a relative bright spot, coming in at 52.7 against a 52.0 forecast and improving from 50.5 in the prior reading, which may have offered some independent support for sterling. Euro area PPI for March came in above forecast on both a monthly and annual basis, an outcome potentially worth monitoring in the context of future ECB policy discussions.

During the U.S. session, the dollar partially recovered from its session lows in the hour ahead of the New York open, with the DXY bouncing from near 97.63 back toward the 98.00-98.10 area before settling into choppy, largely sideways trading through the afternoon. April’s ADP employment report delivered a notable beat at 109,000 versus a 70,000 forecast, the strongest reading in over a year, which may have offered some marginal support to the greenback. Canada’s Ivey PMI also surprised sharply to the upside at 57.7 versus a 50.0 forecast, though USDCAD was the only major pair where the dollar posted a net daily gain, closing up approximately 0.16% to 1.36375. Fed commentary from Goolsbee and Musalem leaned cautious on rate cuts, though neither speaker appeared to materially shift sentiment given the dominant geopolitical backdrop.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Today’s review highlights a market driven by binary geopolitical outcomes. But as any pro will tell you, a great thesis can still fail if the trader lacks the discipline to execute it.

In “Unknown Market Wizards,” (⭐ 4.6★ | 1,400+ reviews on Amazon) Jack Schwager interviews successful traders to reveal a common truth: their edge isn’t just knowledge or skills—it’s their psychological resilience and rigid risk control. Whether you’re navigating shifting geopolitical themes or top tier economic data, learn how the “wizards” stay clinical when the rest of the market is emotional.

Master Your Trading Mindset with Market Wizards!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- BoJ Monetary Policy Meeting Minutes at 11:50 pm GMT

- Australia Balance of Trade for March 2026 at 1:30 am GMT

- Germany Factory Orders for March 2026 at 6:00 am GMT

- Swiss Unemployment Rate for April 2026 at 7:00 am GMT

- Euro area ECB de Guindos Speech at 7:15 am GMT

- China Foreign Exchange Reserves for April 2026

- U.K. S&P Global Construction PMI for April 2026 at 8:30 am GMT

- Euro area Retail Sales for March 2026 at 9:00 am GMT

- U.S. Challenger Job Cuts for April 2026 at 11:30 am GMT

- U.S. Initial Jobless Claims for May 2, 2026 at 12:30 pm GMT

- U.S. Unit Labour Costs & Nonfarm Productivity Prel for March 31, 2026 at 12:30 pm GMT

- Euro area ECB Lane Speech at 12:40 pm GMT

- U.S. Consumer Inflation Expectations for April 2026 at 3:00 pm GMT

- Euro area ECB Schnabel Speech at 5:00 pm GMT

- U.S. Fed Hammack Speech at 6:05 pm GMT

- U.S. Consumer Credit Change for March 2026 at 7:00 pm GMT

- U.S. Fed Williams Speech at 7:30 pm GMT

- U.S. Fed Balance Sheet for May 6, 2026 at 8:30 pm GMT

Thursday’s calendar is dense with potential catalysts, though geopolitical headlines tied to U.S.-Iran deal developments may continue to overshadow any scheduled data releases.

The U.S. preliminary Q1 unit labor costs and nonfarm productivity figures at 12:30 pm GMT carry particular relevance given Goolsbee’s Wednesday remarks on productivity growth, AI hype, and inflation risk, with any upside surprise in productivity possibly amplifying market debate about how aggressively the Fed should respond to a productivity surge that has not yet fully materialized in the data.

Weekly jobless claims at the same time will be watched as a near-term labor market pulse check ahead of Friday’s nonfarm payrolls report.

On the European side, ECB speakers de Guindos, Lane, and Schnabel are all scheduled, and markets may be watching for any reaction to Wednesday’s sharp contraction in Eurozone Services PMIs and the above-forecast PPI print. In the background, Iran’s expected response to the U.S. memorandum of understanding via Pakistan remains the session’s key wildcard.

Stay frosty out there, forex friends!

Wednesday’s market moves were textbook geopolitical risk premium adjustment. But understanding how conflict narratives turn into currency moves requires knowing the mechanisms behind it. Premium members can read our lesson:

📖 Geopolitical Risk, Trade Policy, and Safe Haven Flows

Reading this helps you understand how geopolitical events drive currencies, which safe havens to watch when headlines shift risk sentiment, and how to manage risk when geopolitical narratives dominate the data calendar.

And if you’re not a Premium subscriber yet, now’s a good time to sign up.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just the headlines that moved markets today, but the fundamental forces shaping how currencies react when geopolitical risk shifts.