Oil prices surged more than 5% after U.S. and Iranian forces exchanged fire in the Strait of Hormuz on Monday, shaking a four-week ceasefire and driving broad risk-off flows across markets. Equities fell from record highs, gold extended a session-long slide despite the escalating conflict, and the U.S. dollar closed as arguably the best performing major currency. Minneapolis Fed President Kashkari warned the Iran war raises inflation risks and may require rate hikes, adding a monetary policy dimension to what was otherwise a geopolitics-dominated session.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Australia TD-MI Inflation Gauge for April 2026: 0.6% m/m (1.1% m/m forecast; 1.3% m/m previous)

- Australia ANZ-Indeed Job Ads for April 2026: -0.8% m/m (0.9% m/m forecast; -3.1% m/m previous)

- Australia Building Permits Prel for March 2026: 9.0% y/y (13.2% y/y forecast; 14.0% y/y previous); -10.5% m/m (-6.0% m/m forecast; 29.7% m/m previous)

- Australia Private House Approvals Prel for March 2026: 0.9% m/m (-0.2% m/m forecast; 0.2% m/m previous)

- Swiss procure.ch Manufacturing PMI for April 2026: 54.5 (52.5 forecast; 53.3 previous)

- Germany S&P Global Manufacturing PMI Final for April 2026: 51.4 (51.2 forecast; 52.2 previous)

- Euro area S&P Global Manufacturing PMI Final for April 2026: 52.2 (52.2 forecast; 51.6 previous)

- France New Car Registrations for April 2026: -0.3% y/y (4.5% y/y forecast; 12.9% y/y previous)

- U.S. Total Vehicle Sales for April 2026: 15.9M (16.1M forecast; 16.3M previous)

- Euro area ECB Annual Report: The euro area achieved moderate GDP growth of 1.4% in 2025 (up from 0.9% in 2024), driven initially by export front-loading amid tariff concerns and later sustained by resilient domestic demand, a robust labour market, and the effects of prior rate cuts, despite global challenges and uncertainty.

- U.S. Factory Orders for March 2026: 1.5% m/m (0.5% m/m forecast; 0.0% m/m previous)

- ECB Survey of Professional Forecasters: revised up near-term headline HICP inflation expectations to 2.7% for 2026 (from 1.8%) and core to 2.2%, while keeping longer-term (2030) at 2.0%. They lowered GDP growth forecasts for 2026 to 1.0% (from 1.2%) and 2027 to 1.3%

- The US and Iran exchanged fire in the Persian Gulf on Monday; US military claims it fought off attacks from Iranian drones, missiles and armed small boats.

- UAE Defense Ministry says that 3 missiles from Iran were intercepted

Promoted: Day traders & Scalpers have better odds of making great decisions if they see market catalysts right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

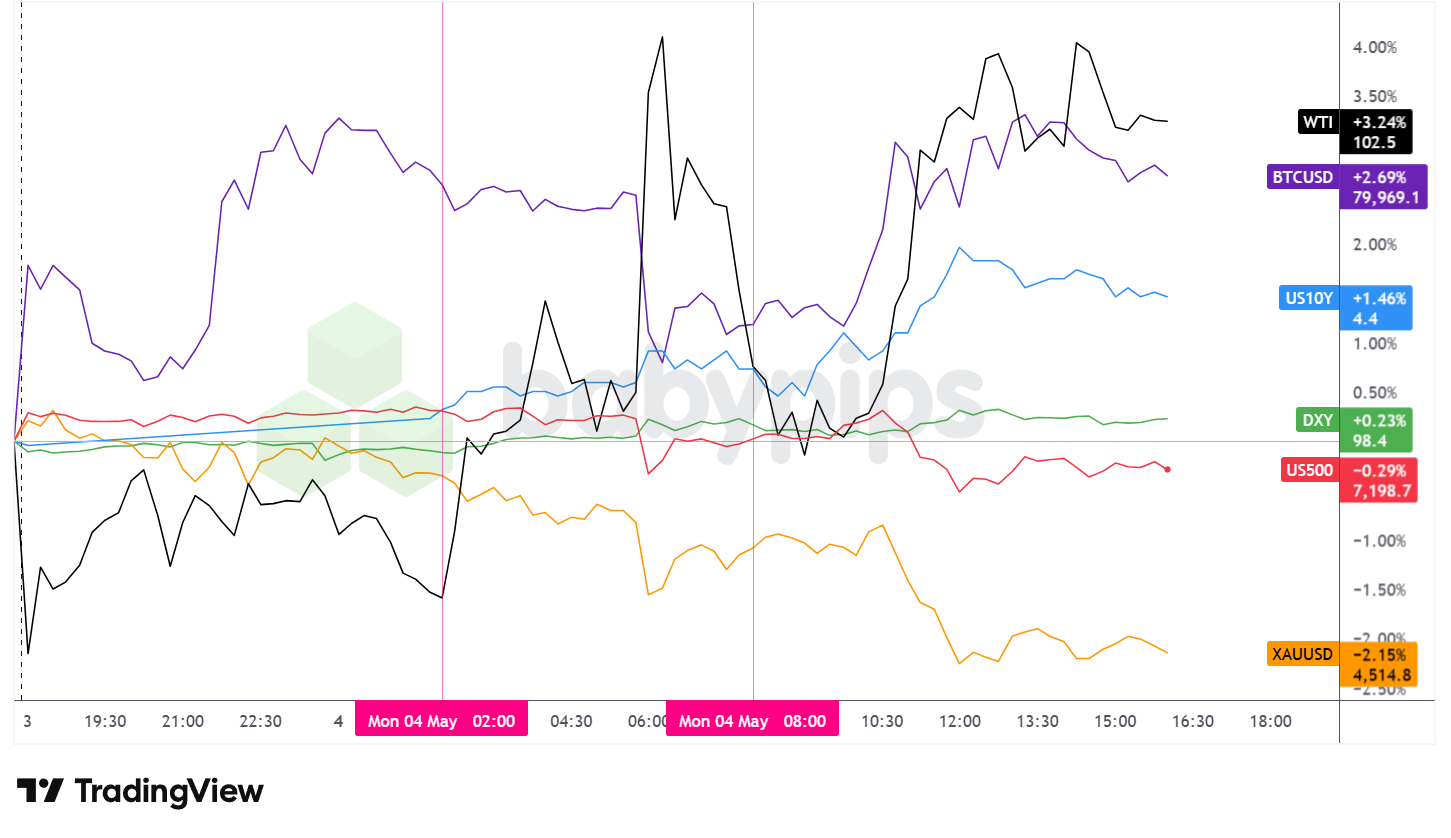

Broad Market Price Action:

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Monday’s session was defined by escalating conflict in the Strait of Hormuz. The violence between U.S. and Iranian forces drove energy prices sharply higher, pushed bond yields up on inflation concerns, and sent equities and gold lower in a broadly risk-off environment.

WTI crude oil was the session’s clear outperformer, closing up 5.53% at $102.495 per barrel. Crude began climbing during the Asian session as President Trump’s Project Freedom announcement filtered into markets. Prices surged during the European session following reports of a tanker struck north of Fujairah, and again after the U.S. open as confirmed exchanges of fire between U.S. and Iranian forces triggered fresh buying. WTI reached intraday highs near $103.80 before pulling back to settle at $102.495.

The S&P 500 declined 0.57% to 7,198.8, further retreating from last week’s all-time highs. The index opened with a modest tone, but a cluster of geopolitical escalation headlines around midday ET sent the index sharply to session lows near 7,171 before a partial recovery into the close. The move coincided with a broad risk-off flush across equities as oil surged and Treasury yields climbed.

Gold fell 2.28% to $4,517.8, a notable decline given the intensifying geopolitical backdrop. The precious metal had been drifting lower since the Asian session open, with the selling accelerating through the London and U.S. sessions. Rising Treasury yields and broad dollar strength may have weighed on the non-yielding metal, possibly offsetting what would ordinarily be safe-haven demand in an active conflict environment. The magnitude of gold’s decline on a day of direct U.S.-Iran military exchange is worth flagging as further signals the recent Dollar-led regime for the precious metal.

Bitcoin closed up 1.24% at $79,991.23. The cryptocurrency briefly traded above $80,000 during Asian hours, breaking that area for the first time since late January. A sharp drop to the $78,280 area around the London open reversed much of that gain, before Bitcoin recovered above $80,000 during the U.S. morning session and then pulled back slightly into the close. No notable cryptocurrency drivers to point to on the day, so BTC’s behavior was likely driven by broad sentiment, as well as equity movement.

The 10-year Treasury yield rose approximately 6.5 basis points to 4.429%, a 1.49% increase on the session. Yields climbed steadily throughout the day, reaching a peak near 4.451% around midday ET before easing modestly. The move likely reflected heightened inflation expectations tied to the energy price surge, with Minneapolis Fed President Kashkari explicitly linking the Iran war to upside inflation risks and the potential need for rate hikes.

Promoted: Navigating Geopolitical Volatility? Get the Capital You Need to Trade It.

Surprise geopolitical news like unexpected military action can move markets quickly and create prime opportunities for disciplined traders. Don’t let a lack of liquidity hold you back from capitalizing on these developments

Alpha Capital Group provides access to simulated funded accounts from $5K to $200K, you can execute high-conviction setups with the professional position sizing they deserve. Join 250K+ traders in 180+ countries today!

Learn more about Alpha Capital Group and use coupon code “babypips” to save 15% on a trading evaluation!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

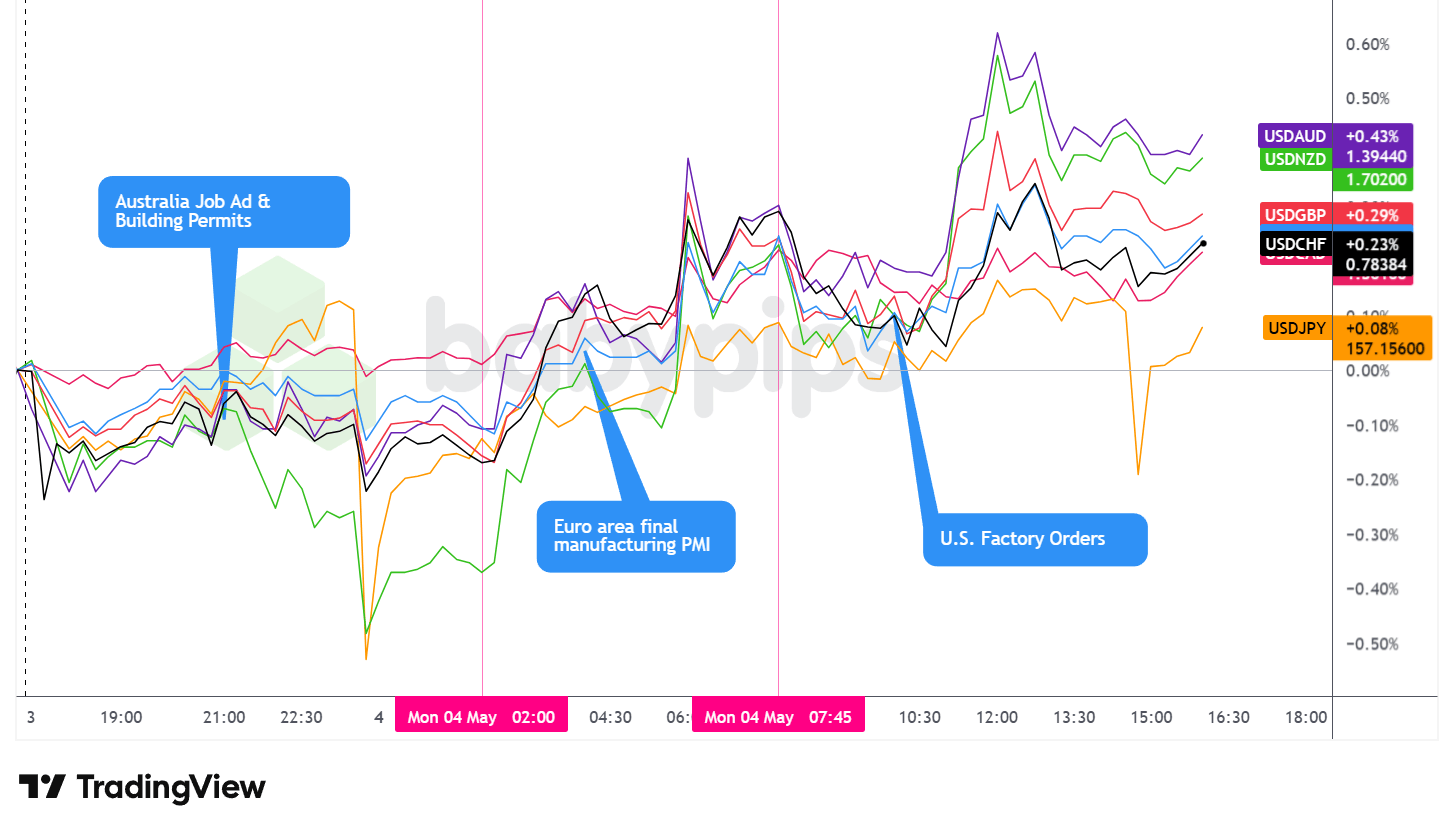

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar closed as the best performing major currency on Monday, posting net gains against all seven majors tracked in the overlay chart above.

During the Asian session, the dollar dipped shortly after the session opened before trading choppy and largely sideways for the remainder of the period, leaving it with a net bearish lean against major currencies through the Asian close. Japan and mainland China were both out for public holidays, limiting liquidity and keeping most FX pairs in confined ranges. USD/JPY saw some early volatility before grinding higher, which could have been additional intervention moves from Japan, sending USD/JPY from 157.20 down to 155.89 earlier in the session; but there doesn’t seem to be any confirmation of that at the time of this writing.

After the London open, the dollar shifted to a net higher posture against the major currencies. The move coincided with escalating Middle East headlines, including Trump’s Project Freedom announcement, CENTCOM’s confirmation of guided-missile destroyers and more than 15,000 service members committed to the strait, and Iran’s parliament security chief rejecting the initiative as a ceasefire violation. On the European data front, the eurozone Manufacturing PMI Final for April came in at 52.2, in line with expectations, while Switzerland’s manufacturing PMI beat at 54.5. Eurozone Sentix investor confidence printed at -16.4 versus -21.0 forecast, a beat, but the backdrop of ECB policymakers signaling inflation acceleration and a possible June rate hike likely kept the broader tone cautious for European currencies.

After the U.S. open, the dollar initially dipped against the major currencies through the remainder of the London session, possibly correlating with early U.S. session volatility as markets processed the ongoing geopolitical developments. U.S. Factory Orders for March 2026 came in well above forecast at 1.5% m/m versus 0.5% expected, but the data release appeared to have limited directional effect on the dollar in the context of the day’s dominant Hormuz narrative.

We did see USD spike higher just after the London close, correlating with a cluster of fresh geopolitical headlines. These included UAE Defense Ministry confirmation of three intercepted Iranian missiles, a fire at Fujairah’s petroleum industrial site attributed to an Iranian drone strike, and a statement from the IRGC spokesperson that vessels violating rules in the Strait of Hormuz would be stopped by force. The spike in USD also broadly coincided with the S&P 500 selling to session lows and oil prices surging toward their intraday highs.

Monday’s session was shaped by direct U.S.-Iran military exchanges in the Strait of Hormuz, and if you’re not sure how geopolitical shocks translate into currency moves and safe haven flows, this is worth reading. Premium members can read our lesson:

📖 Geopolitical Risk, Trade Policy, and Safe Haven Flows

Reading this helps you understand how geopolitical events drive currency markets, which safe havens typically benefit during conflict (and why gold’s decline on Monday was unusual), and how risk-off flows shape FX behavior when a shock hits.

And if you’re not a Premium subscriber yet, now’s a good time to sign up.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just what the charts are showing, but the geopolitical forces and safe haven dynamics driving the moves.

Upcoming Potential Catalysts on the Economic Calendar

- Australia S&P Global Services PMI Final for April 2026 at 11:00 pm GMT

- Australia Household Spending for March 2026 at 1:30 am GMT

-

Australia RBA Interest Rate Decision for May 5, 2026 at 4:30 am GMT

- Australia RBA Press Conference at 5:30 am GMT

- Swiss Inflation Rate for April 2026 at 6:30 am GMT

- U.S. Building Permits Final for March 2026 at 12:00 pm GMT

- Canada Balance of Trade for March 2026 at 12:30 pm GMT

- ECB President Lagarde Speech at 12:30 pm GMT

- U.S. Balance of Trade for March 2026 at 12:30 pm GMT

- New Zealand Global Dairy Trade Price Index for May 5, 2026

- Canada S&P Global Services PMI for April 2026 at 1:30 pm GMT

- U.S. S&P Global Services PMI Final for April 2026 at 1:45 pm GMT

- U.S. New Home Sales for March 2026 at 2:00 pm GMT

- U.S. JOLTs Job Openings & Quits for March 2026 at 2:00 pm GMT

- U.S. ISM Services PMI for April 2026 at 2:00 pm GMT

- Fed Bowman Speech at 2:00 pm GMT

- Euro area ECB Lane Speech at 3:40 pm GMT

- BoE Woods Speech at 4:30 pm GMT

- Fed Barr Speech at 4:30 pm GMT

Tuesday’s calendar is headlined by the Reserve Bank of Australia’s May interest rate decision at 4:30 am GMT, followed by a press conference at 5:30 am GMT. With Australia’s TD-MI inflation gauge coming in well below forecast at 0.6% m/m and building permits missing on a monthly basis, markets may be watching closely for any dovish signals.

ECB President Lagarde speaks at 12:30 pm GMT against a backdrop of ECB policymakers explicitly flagging a possible June rate hike and the ECB Survey of Professional Forecasters sharply revising up 2026 inflation expectations.

The U.S. session brings a dense afternoon cluster including ISM Services PMI, JOLTs job openings, and the trade balance at 2:00 pm GMT, all of which could shape the market’s read on Federal Reserve policy trajectory amid the Hormuz-driven inflation risk premium building in energy markets.

Stay frosty out there, forex friends!

Promotion: When the Market Swings, Are You Reacting or Executing?

Monday delivered a “geopolitical shock regime” that saw market volatility spike higher! Unforeseen market reactions are where even some of the best technical setups fail, a lot of times due to emotional execution.

In “Positive Trading Psychology,” renowned psychologist Brett Steenbarger reveals in his newest book that the secret to navigating such volatility isn’t “fixing” your flaws—it’s doubling down on your innate character strengths. Learn how to stay clinical while the rest of the market is emotional, turning Monday’s military action into your professional edge.

Learn more about “Positive Trading Psychology: Turning personal strengths into trading strengths” on Amazon!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.