The U.S. dollar ended April as the session’s worst-performing major currency, likely pressured by Japanese yen intervention warnings, central bank holds from both the Bank of England and European Central Bank, and a softer-than-expected U.S. Q1 GDP print that weighed on greenback sentiment into the close.

Equities and gold both gained ground, with the S&P 500 capping its best monthly performance since late 2020 at fresh record highs, while WTI crude retreated despite an elevated geopolitical backdrop centered on Iran.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Japan’s Vice Finance Minister for International Affairs Mimura issued what he described as a “final warning” to currency speculators, adding that Japanese authorities were in close contact with their U.S. counterparts.

- Japan Industrial Production Prel for March 2026: 2.3% y/y (3.3% y/y forecast; 0.4% y/y previous); -0.5% m/m (1.1% m/m forecast; -2.0% m/m previous)

- Japan Retail Sales for March 2026: 1.7% y/y (2.1% y/y forecast; -0.2% y/y previous); 1.3% m/m (0.8% m/m forecast; -2.0% m/m previous)

- New Zealand ANZ Business Confidence for April 2026: -10.6 (27.0 forecast; 32.5 previous)

- Australia Import Prices for Q1 2026: 0.1% q/q (0.7% q/q forecast; 0.9% q/q previous)

- Australia Export Prices for Q1 2026: 0.5% q/q (1.0% q/q forecast; 3.2% q/q previous)

- China NBS Manufacturing PMI for April 2026: 50.3 (50.6 forecast; 50.4 previous)

- Japan Housing Starts for March 2026: -29.3% y/y (-26.0% y/y forecast; -4.9% y/y previous)

- Japan Consumer Confidence for April 2026: 32.2 (31.0 forecast; 33.3 previous)

- Germany Retail Sales for March 2026: -2.0% y/y (0.4% y/y forecast; 0.7% y/y previous); -2.0% m/m (-0.3% m/m forecast; -0.6% m/m previous)

- Germany Unemployment Rate for April 2026: 6.4% (6.3% forecast; 6.3% previous)

- Germany GDP Growth Rate Flash for Q1 2026: 0.3% y/y (0.2% y/y forecast; 0.4% y/y previous); 0.3% q/q (0.1% q/q forecast; 0.3% q/q previous)

- Euro area Unemployment Rate for March 2026: 6.2% (6.2% forecast; 6.2% previous)

- Euro area GDP Growth Rate Flash for Q1 2026: 0.8% y/y (0.8% y/y forecast; 1.2% y/y previous); 0.1% q/q (0.1% q/q forecast; 0.2% q/q previous)

- Euro area CPI Growth Rate Flash for April 2026: 3.0% y/y (2.9% y/y forecast; 2.6% y/y previous); 1.0% m/m (1.0% m/m forecast; 1.3% m/m previous)

- U.K. Official Bank Rate for April 30, 2026: 3.75% (3.75% forecast; 3.75% previous)

- Euro area ECB Interest Rate Decision for April 30, 2026: 2.15% (2.15% forecast; 2.15% previous)

- Canada Average Weekly Earnings for February 2026: 3.4% y/y (2.1% y/y forecast; 2.0% y/y previous)

- Canada GDP Prel for March 2026: 0.0% m/m (-0.1% m/m forecast; 0.2% m/m previous)

- U.S. Initial Jobless Claims for April 25, 2026: 189.0k (219.0k forecast; 214.0k previous)

- U.S. Core PCE Price Index for March 2026: 3.2% y/y (3.1% y/y forecast; 3.0% y/y previous); 0.3% m/m (0.3% m/m forecast; 0.4% m/m previous)

- U.S. GDP Growth Rate Adv for Q1 2026: 2.0% q/q (1.8% q/q forecast; 0.5% q/q previous)

- ECB President Lagarde stated that most measures of longer-term inflation expectations stand around 2%; her press conference was described as lacking the hawkish tone some participants had anticipated.

Promoted: Protecting your trading capital starts with securing your access. Don’t let a weak password be the single point of failure for your brokerage or prop firm accounts. LastPass simplifies your digital life by generating and storing complex, encrypted passwords for every site you use.

Try LastPass for Free Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

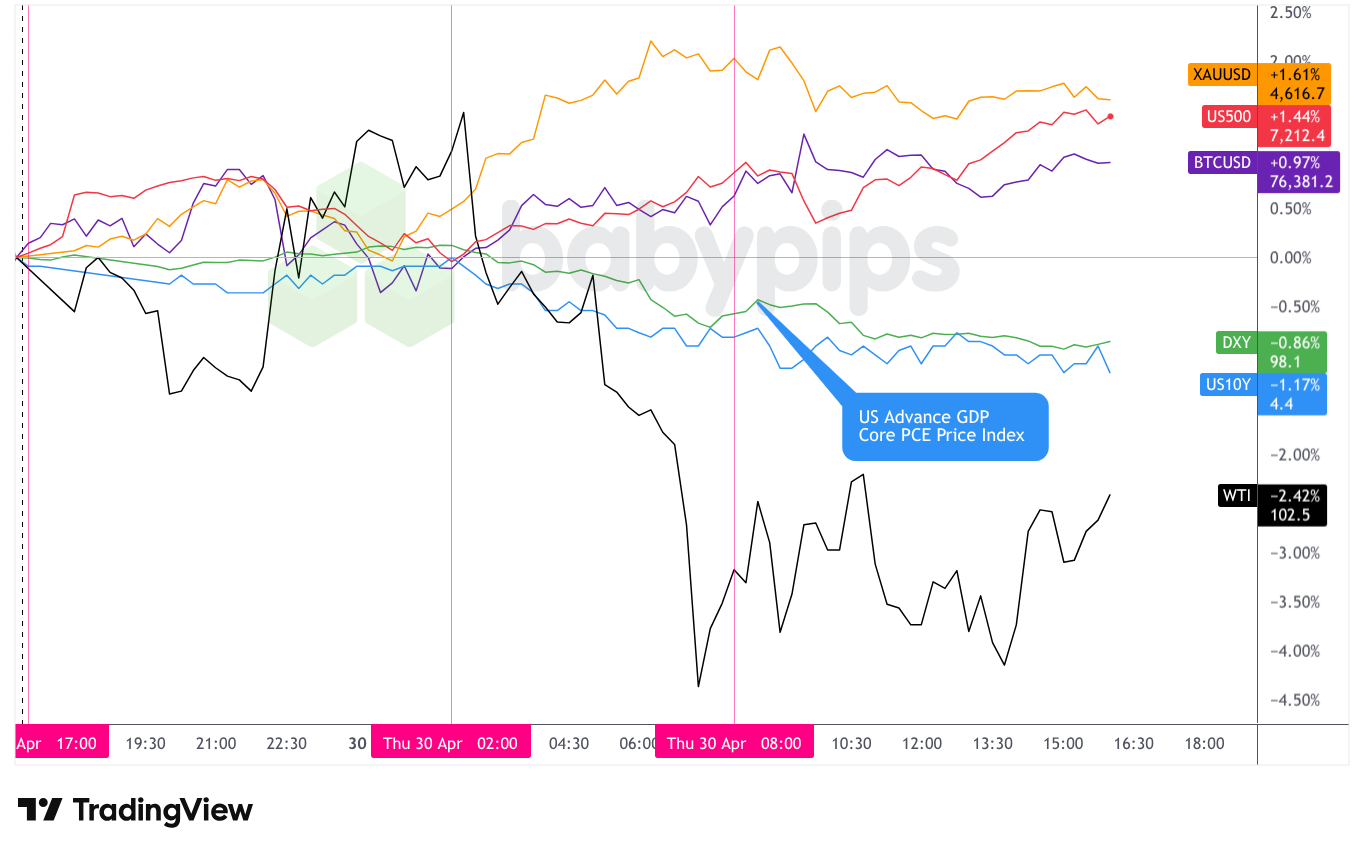

Broad Market Price Action:

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Thursday’s broad market session delivered a mostly risk-on finish, with equities and gold both advancing while Treasury yields declined and WTI crude retreated. The session marked the final trading day of April, and month-end positioning may have amplified directional moves across asset classes.

The S&P 500 gained and closed near 7,218, capping its best monthly performance since late 2020. The index pushed steadily higher through the North American session to break all-time highs, and with US Data coming in mixed, it’s possible that strong earnings this week from major technology firms, a dip in unemployment claims and a rebound in GDP may have outweighed concerns about energy prices and ongoing geopolitical uncertainty.

Gold rose approximately 1.59%, closing near $4,616 per ounce. The precious metal dipped toward $4,545 during the late Asian session before rallying during the London hours, reaching a session high near $4,647. The advance may have reflected a combination of broad dollar weakness and residual safe-haven demand from the Iran-related geopolitical backdrop, though pinpointing a single catalyst for the full extent of the move is difficult given the number of concurrent events during the session.

WTI crude oil fell approximately 1.92%, closing near $102.46 per barrel. Oil was bid during the Asian session, reaching highs near $107, possibly correlating with an Axios report that U.S. CENTCOM was preparing to brief President Trump on fresh military options against Iran, including potential infrastructure strikes and a special forces mission targeting Iran’s uranium stockpile. The sharp reversal that unfolded during the London session is one possible explanation being a “sell the news” dynamic or a rotation toward de-escalation scenarios, though the precise driver of the reversal is uncertain. WTI spent most of the U.S. session consolidating in the $100-$103 range.

Bitcoin gained approximately 1.03%, closing near $76,400. The cryptocurrency traded broadly in line with the wider risk-on tone throughout the session, with no apparent crypto-specific catalysts influencing the move.

Promotion: If your confidence has grown in your market awareness & strategies with this market recap, and you wanna take action, Maven Trading can help. They provide simulated funding challenges starting as low as $13, allowing you to trade major pairs with professional-sized capital. No time limits mean you can take swing plays on these market themes without the pressure of a ticking clock.

Learn More About Maven Trading Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

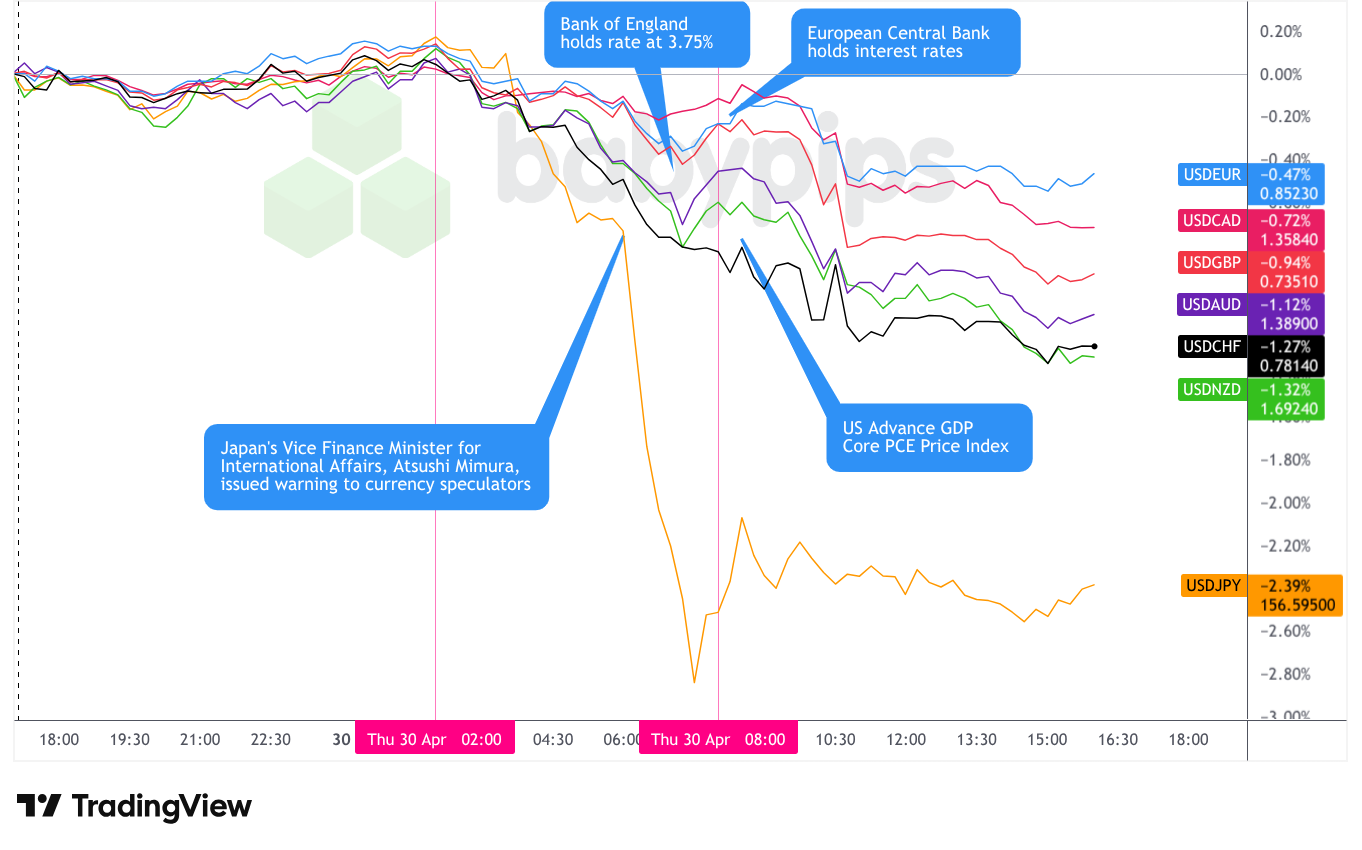

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar closed Thursday as the worst-performing major currency, posting broad losses in a session shaped by Japanese intervention activity, central bank decisions from the BoE and ECB, and weaker-than-expected U.S. growth data.

During the Asian session, the dollar initially pulled back slightly, possibly reflecting cautious positioning ahead of a heavy event calendar. The dollar then rebounded and pushed modestly higher heading into the London open, with the DXY approaching the 99.10 area and USD/JPY extending above the 160.00 handle toward 160.40 without any immediate intervention response from Japanese officials. China’s PMI data delivered a mixed verdict during the session: the official NBS Manufacturing PMI held at 50.3, marginally below the 50.6 forecast but still above the 50.0 expansion threshold, while the Non-Manufacturing PMI slipped back into contraction at 49.4, a roughly 40-month low and a miss against the 50.4 forecast, suggesting soft domestic demand despite a resilient export-oriented factory sector. The private RatingDog Manufacturing PMI told a more upbeat story, surging to 52.2 against a 50.7 forecast, its strongest reading since late 2020, reflecting the relative outperformance of China’s private and export-focused firms. New Zealand’s ANZ Business Confidence collapsed to -10.6 from +32.5 in March, well below the +27.0 forecast, likely due to cost pressures possibly linked to energy market disruption from the Iran conflict; this likely weighed on the NZD at the margin during the session, though the broader impact on dollar direction was limited.

The London session brought the day’s most consequential FX catalyst in the form of escalating verbal intervention from Japanese authorities. Finance Minister Katayama’s initial warning gave the yen its first meaningful boost, and as USD/JPY began recovering from that move, Vice Finance Minister Mimura issued what he characterized as a “final warning,” noting close coordination with U.S. counterparts. USD/JPY then dropped sharply, falling from highs near 160.40 to levels approaching 156 at the most extreme intraday point, in a move consistent with what the IL Wrap described as a pattern resembling late-January “rate checks,” though Nikkei confirmed it was direct intervention. The scale of the yen’s reversal dragged broad USD lower across the other major pairs as well, with the DXY dropping from near 99.10 to sub-98.20 in relatively short order.

Layered on top of the yen dynamics, a range of European economic data added nuance to the session. Eurozone Q1 flash GDP came in at +0.1% q/q, in line with the forecast but below the prior quarter’s +0.2% pace and representing a softer growth impulse heading into a potential Q2 contraction if the Iran conflict extends through summer. Eurozone flash CPI for April picked up to 3.0% y/y, a touch above the 2.9% forecast, while core CPI eased slightly to 2.2% y/y, in line with expectations. Germany Q1 GDP beat at +0.3% q/q, but German retail sales for March came in well below forecast and German unemployment rose by 20k versus a 2k estimate, adding to the cautiously mixed European backdrop. French inflation surprised to the upside.

The Bank of England held its policy rate at 3.75%, as widely expected, but the MPC vote split surprised markets: eight members voted to hold, one voted to hike, and none voted to cut, versus the nine-to-zero hold outcome consensus. The BoE’s overall tone was described as cautious, acknowledging that second-round inflation effects from elevated energy prices remained a risk while noting monetary policy cannot directly offset global energy price shocks. The probability of a June BoE hike reportedly fell from 63% to 48% following the decision. GBP/USD nonetheless rallied strongly through the North American session, rising over a full figure, in what may have reflected the broader USD selling environment as much as any specific sterling catalyst.

The ECB held all rates as expected, with the main refinancing rate at 2.15% and the deposit facility rate at 2.0%. President Lagarde’s press conference was perceived as lacking the strong hawkish tone some participants had anticipated, and EUR/USD declined initially. Reports attributed to ECB sources that emerged after the conference were reportedly more hawkish, however, and the euro subsequently reversed higher. The overall ECB signal appeared to lean toward patience rather than outright hawkishness, arguably consistent with a eurozone growth picture that remains modest and a core inflation trend that is gradually easing.

During the U.S. session, the dollar extended its losses following the release of the Q1 2026 advance GDP estimate, which came in at +2.0% annualized against a +2.3% consensus. Core PCE inflation printed in line at +3.5% y/y, providing no additional hawkish impetus from the inflation side. U.S. initial jobless claims surprised strongly to the downside at 189k versus a 215k forecast, suggesting labor market resilience, though the strong claims data appeared insufficient to reverse the greenback’s broader trend lower. Canada’s February GDP came in at +0.2% m/m, in line with expectations.

Upcoming Potential Catalysts on the Economic Calendar

- New Zealand ANZ Roy Morgan Consumer Confidence for April 2026 at 10:00 pm GMT

- New Zealand Building Permits for March 2026 at 10:45 pm GMT

- Australia S&P Global Manufacturing PMI Final for April 2026 at 11:00 pm GMT

- Japan Tokyo CPI for April 2026 at 11:30 pm GMT

- Japan S&P Global Manufacturing PMI Final for April 2026 at 12:30 am GMT

- Australia PPI for March 31, 2026 at 1:30 am GMT

- U.K. Nationwide Housing Prices for April 2026 at 6:00 am GMT

- Australia Commodity Prices for April 2026 at 6:30 am GMT

- Swiss Retail Sales for March 2026 at 6:30 am GMT

- U.K. Monetary Developments for March 2026 at 8:30 am GMT

- U.K. S&P Global Manufacturing PMI Final for April 2026 at 8:30 am GMT

- Bank of England Pill Speech at 12:15 pm GMT

- Canada S&P Global Manufacturing PMI for April 2026 at 1:30 pm GMT

- U.S. S&P Global Manufacturing PMI Final for April 2026 at 1:45 pm GMT

- U.S. ISM Manufacturing PMI for April 2026 at 2:00 pm GMT

Friday’s calendar is headlined by the U.S. ISM Manufacturing PMI, which arrives alongside the S&P Global Manufacturing PMI final for April. Given the softer-than-expected GDP print from Thursday and persistent concerns about how elevated energy prices are filtering through to business costs and demand conditions, these manufacturing reads could attract closer scrutiny than usual.

Japan’s Tokyo CPI data for April will likely be watched carefully in the wake of confirmed yen intervention, as the print may influence expectations for the Bank of Japan’s June policy meeting, particularly with Governor Ueda’s June 3 speech already on the schedule.

BoE Chief Economist Pill is also scheduled to speak, and any commentary on the rate path following Thursday’s surprise hawkish dissent could be market-moving for sterling, especially given the sharp repricing in June hike odds.

Australia’s commodity price data may offer a read on terms-of-trade dynamics under the current energy market backdrop.

Stay frosty out there, forex friends!

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Most trading mistakes aren’t technical—they’re psychological. In the classic “Trading in the Zone” by Mark Douglas (⭐ 4.7★ | 10,000+ reviews on Amazon), you’ll learn how to master the probabilistic thinking and emotional discipline mentioned in today’s article. If you struggle with hesitation or breaking your rules, this is your manual for consistent execution.

Click on the link to learn more about “Trading in the Zone” by Mark Douglas!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.