Markets faced a heavy macro schedule on Wednesday as the Federal Reserve delivered a historically divided rate hold and President Trump confirmed an indefinite extension of the Iranian naval blockade, sending WTI crude above $104 per barrel.

The hawkish tone from the FOMC’s 8-4 vote, in which three regional presidents pushed back against easing bias language in the post-meeting statement, reinforced the view that rate cuts are likely off the table for the foreseeable future, lifting Treasury yields to a one-month high and propelling the U.S. dollar to its strongest close among major currencies on the day.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Australia CPI Growth Rate for March 2026: 4.6% y/y (4.8% y/y forecast; 3.7% y/y previous); 1.1% m/m (1.4% m/m forecast; 0.0% m/m previous)

- Swiss Economic Sentiment Index for April 2026: -30.3 (-40.0 forecast; -35.0 previous)

- Euro area M3 Money Supply for March 2026: 3.2% (2.9% forecast; 3.0% previous)

- Euro area Consumer Inflation Expectations for April 2026: 49.1 (48.0 forecast; 43.4 previous)

- Euro area Economic Sentiment for April 2026: 93.0 (94.0 forecast; 96.6 previous)

- U.S. MBA 30-Year Mortgage Rate for April 24, 2026: 6.37% (6.35% previous)

- U.S. MBA Mortgage Applications for April 24, 2026: -1.6% (7.9% previous)

- Germany CPI Growth Rate Prel for April 2026: 2.9% y/y (3.1% y/y forecast; 2.7% y/y previous); 0.6% m/m (0.8% m/m forecast; 1.1% m/m previous)

- U.S. Building Permits Prel for March 2026: -10.8% m/m (-0.7% m/m forecast; 10.9% m/m previous)

- U.S. Durable Goods Orders for March 2026: 0.8% m/m (0.8% m/m forecast; -1.4% m/m previous)

- The Bank of Canada held rates steady for a fourth consecutive meeting at 2.25%. Governor Tiff Macklem said a policy rate close to current settings “looks appropriate,” but flagged major risks from the Middle East conflict and a potential North American trade deal review. Macklem warned that if oil prices continue to rise and broader inflationary pressures build, “there may be a need for consecutive increases in the policy rate.”

- President Trump told Axios he had rejected a recent Iranian proposal to reopen the Strait of Hormuz and would not lift the naval blockade until a nuclear deal is secured. Trump said Iran is “choking like a stuffed pig” and that the blockade is “somewhat more effective than the bombing.”

- U.S. EIA Crude Oil Stocks Change for April 24, 2026: -6.23M (1.93M previous)

- Kevin Warsh, President Trump’s nominee to succeed Jerome Powell as Federal Reserve chair, won the backing of the Senate Banking Committee on a 13-11 party-line vote, putting him on track for full Senate confirmation before Powell’s term as chair ends May 15.

- The FOMC voted 8-4 to leave its benchmark federal funds rate in a target range of 3.5%-3.75%, marking the first time since October 1992 that four officials dissented at a single FOMC meeting. Cleveland Fed President Beth Hammack, Minneapolis’ Neel Kashkari, and Dallas’ Lorie Logan voted against inclusion of easing bias language in the post-meeting statement, while Governor Stephen Miran dissented in favor of a 25 basis point cut.

- Federal Reserve Chair Jerome Powell said at his final press conference as chair that he intends to remain at the central bank as a member of the Board of Governors. Powell cited the ongoing Department of Justice investigation into the Fed, saying he will remain “until this investigation is well and truly over with transparency and finality.”

Promoted: Protecting your trading capital starts with securing your access. Don’t let a weak password be the single point of failure for your brokerage or prop firm accounts. LastPass simplifies your digital life by generating and storing complex, encrypted passwords for every site you use.

Try LastPass for Free Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

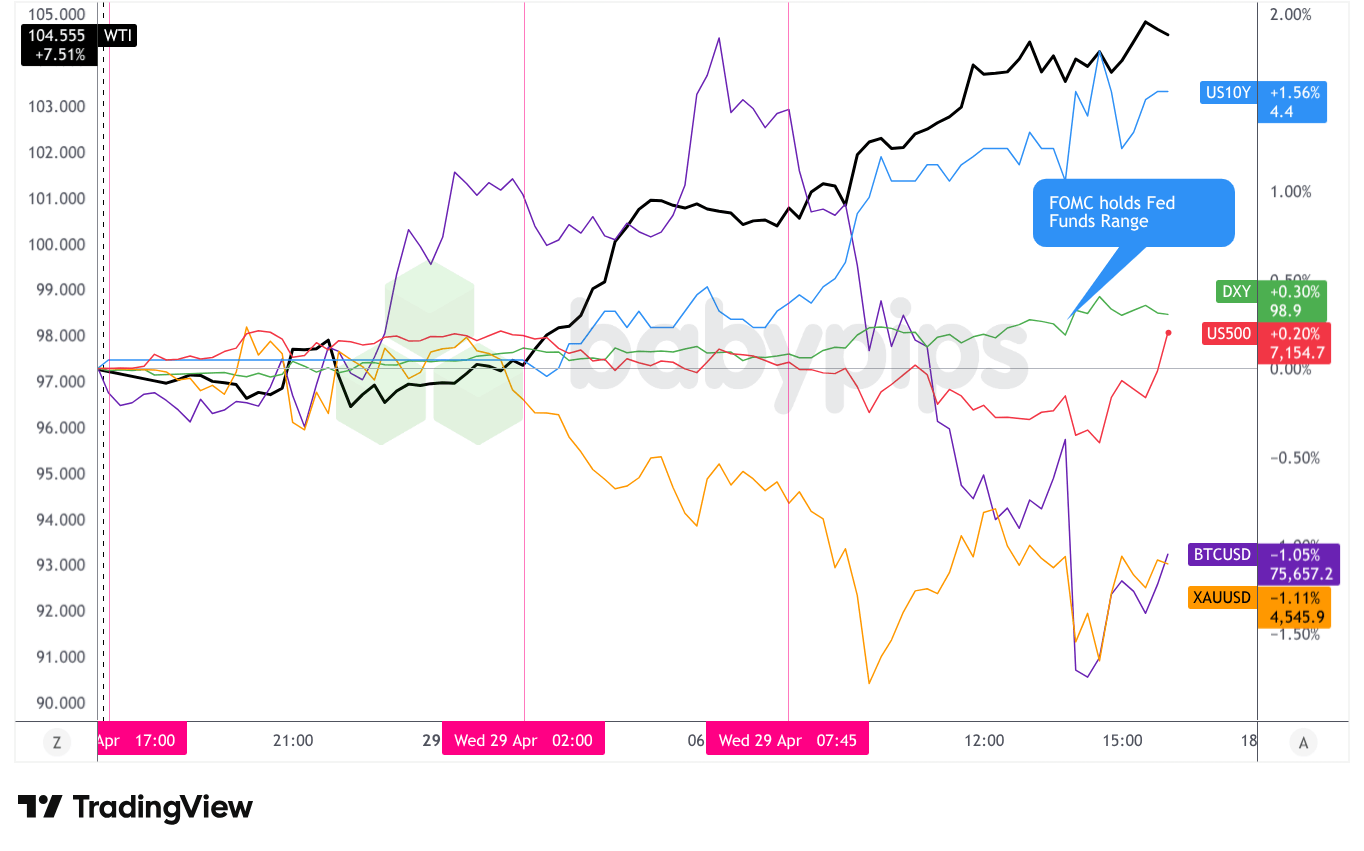

Broad Market Price Action:

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Wednesday’s session was defined by two intersecting forces: an escalating Iran energy crisis and a deeply divided Federal Reserve, whose hawkish dissenters sent a clear signal that the bar for near-term rate cuts has risen considerably.

WTI crude oil was the session’s standout performer, climbing approximately 7.80% to close near $104.58 per barrel. The rally appeared to gather pace through the European session as headlines confirmed Trump’s instructions to aides to prepare for an indefinite blockade extension, then extended further into the U.S. session after Trump confirmed to Axios around midday that he had rejected Iran’s Strait of Hormuz reopening proposal outright. A larger-than-expected EIA crude inventory draw of 6.23 million barrels, reversing a prior build of 1.93 million barrels, likely provided additional support. WTI broke and held above the $100 per barrel level during the European session, posting the largest single-day percentage gain among the tracked assets.

The U.S. 10-year Treasury yield climbed on the day to around 4.407% and reaching a one-month high. Yields rose steadily through the U.S. session, with the move accelerating after the FOMC decision revealed three hawkish dissents objecting to easing bias language. The move appeared to suggest that markets were pricing out near-term rate cuts and beginning to price a small probability of hikes in 2027.

Gold declined approximately 0.96%, closing near $4,552.40 per ounce. The precious metal traded with modest gains during the Asian session before trending broadly lower through the London and U.S. sessions. The sell-off appeared to correlate with the post-FOMC rise in Treasury yields and the broad strengthening of the U.S. dollar, both of which typically weigh on the non-yielding metal. No specific gold-related catalysts were apparent beyond the broader cross-asset macro dynamics of the day.

The S&P 500 ended essentially flat, closing near 7,143 with a gain of just 0.04%. The index traded with an intraday range of roughly 50 points: edging higher during the overnight and early Asian hours, softening through the pre-U.S. session period, and falling to a session low near 7,111 before recovering into the close. The relatively contained equity reaction suggested that the rate hold itself was widely anticipated, though the hawkish dissent tone and ongoing Iran uncertainty appear to have capped any meaningful upside.

Bitcoin declined approximately 1.03%, closing near $75,599. The cryptocurrency rallied during the Asian and early London sessions, reaching highs near $77,900, before reversing and trending lower through the U.S. sessions. No specific Bitcoin-related catalysts were apparent, and the move appeared broadly consistent with a cautious lean in speculative assets.

Promotion: If your confidence has grown in your market awareness & strategies with this market recap, and you wanna take action, Maven Trading can help. They provide simulated funding challenges starting as low as $13, allowing you to trade major pairs with professional-sized capital. No time limits mean you can take swing plays on these market themes without the pressure of a ticking clock.

Learn More About Maven Trading Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

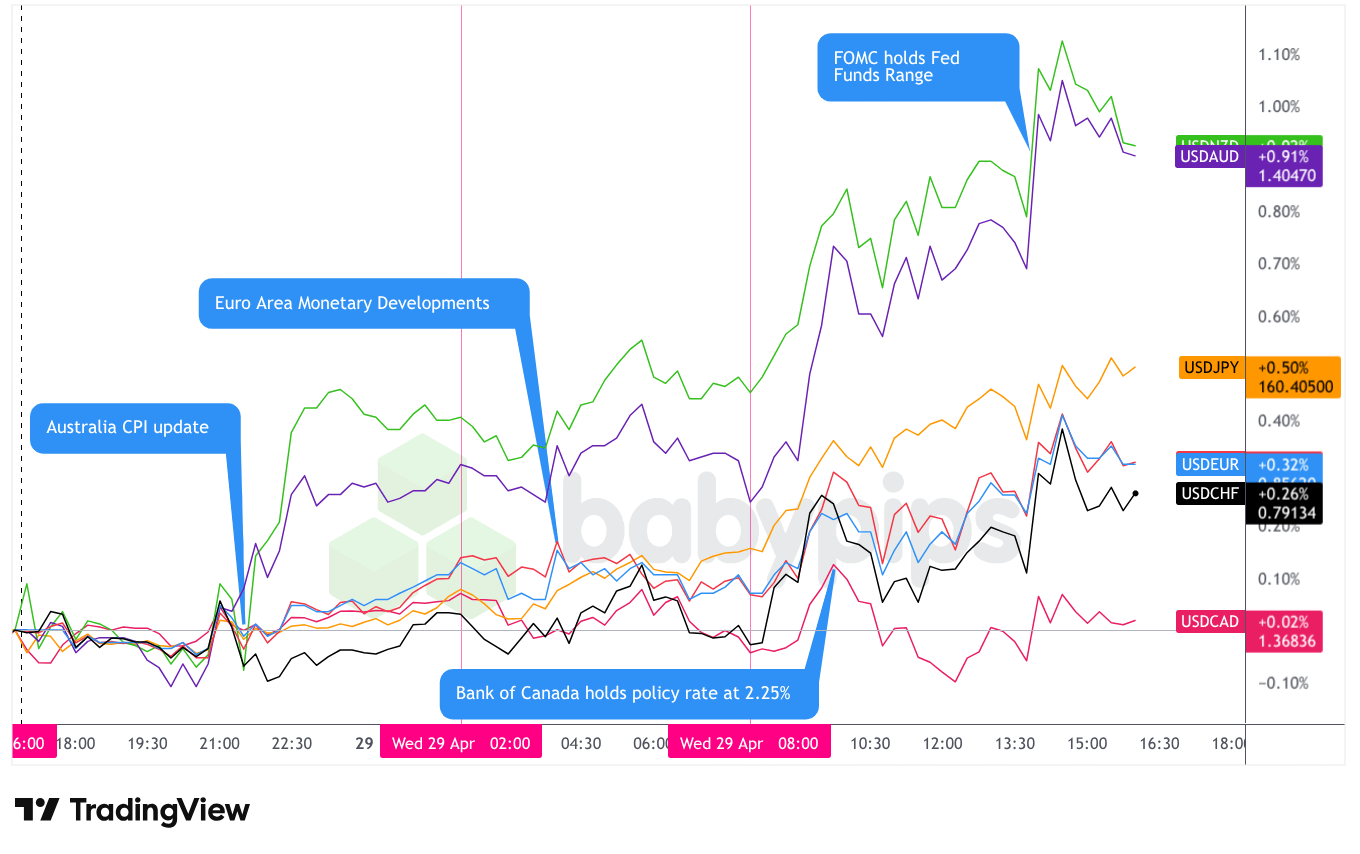

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar traded with a net bullish bias across the full session on Wednesday, closing as arguably the best-performing major currency on the day, slightly edging out the Canadian dollar for the top position.

During the Asian session, regional liquidity was thinner than usual, with Tokyo markets closed for Japan’s Showa Day public holiday. The absence of Tokyo removed a significant source of participation from currency and rates markets, and cash U.S. Treasury trading was shut down for the duration. In this context, the dollar maintained a modest net bullish lean. The most notable FX development in the session was the market’s reaction to Australia’s Q1 CPI data. Headline inflation surged on Middle East-driven energy cost pass-through, but the RBA trimmed mean core measure came in slightly below forecasts, reducing the perceived urgency of near-term RBA tightening. Elsewhere, dollar price action was contained and mixed across other pairs, with no clear directional force beyond the general sideways-to-bullish lean.

During the London session, the dollar continued its broadly net bullish trajectory, with gains gradual rather than sharp. Euro area data painted a softening picture overall: April economic sentiment fell to 93.0 from 96.6 prior and missed the 94.0 forecast, services sentiment dropped sharply to 0.9 from 4.9, and consumer inflation expectations jumped to 49.1 from 43.4, suggesting households are pricing in a more persistent inflation environment. Preliminary German CPI for April came in at 2.9% year-over-year, below the 3.1% forecast, though up from 2.7% prior. Euro area M3 money supply growth and loan data both beat expectations modestly. On balance, the European data offered limited support for the major European currencies. The Swiss Economic Sentiment Index for April came in at -30.3, well above the -40.0 forecast but remaining in deeply negative territory.

During the U.S. session, the dollar’s bullish bias became increasingly pronounced, driven initially by pre-FOMC positioning and then by the hawkish character of the FOMC outcome itself. The morning data slate was mixed: Housing Starts for March surged 10.8% month-over-month, well above the -0.7% forecast, while Building Permits fell a sharp 10.8% against the -0.7% expected, complicating the housing outlook. Core Durable Goods Orders beat expectations at 0.9% versus 0.6% forecast, and Non Defense Goods Orders Ex Air came in at a notably strong 3.3% against a 0.5% forecast. The Goods Trade Balance widened further than expected to -$87.87B. These releases did not appear to generate significant directional FX moves on their own, with the market’s attention likely held in reserve for the FOMC announcement.

The Bank of Canada’s rate hold at 2.25%, matching expectations, generated limited net follow-through for USD/CAD. USD/CAD briefly dipped following the announcement before reversing. Governor Macklem’s commentary, while flagging the risk of consecutive hikes if energy prices remain elevated, also signaled comfort with holding at current settings if the outlook evolves as expected.

The FOMC announcement and Powell’s press conference were the clear catalysts for the session’s most significant FX moves. The 8-4 vote and the three hawkish dissents objecting to easing bias language was arguable the biggest driver that pushed the dollar broadly higher. At the Wednesday close, the U.S. dollar posted gains against all tracked major currencies, with the Australian dollar as the weakest performer on the day.

Upcoming Potential Catalysts on the Economic Calendar

- Japan Industrial Production Prel for March 2026 at 11:50 pm GMT

- Japan Retail Sales for March 2026 at 11:50 pm GMT

- Japan Industrial Production Prel for March 2026 at 11:50 pm GMT

- New Zealand ANZ Business Confidence for April 2026 at 1:00 am GMT

- Australia Import & Export Prices for March 31, 2026 at 1:30 am GMT

- Australia Private Sector & Housing Credit for March 2026 at 1:30 am GMT

- China NBS Manufacturing & Services PMI for April 2026 at 1:30 am GMT

- China RatingDog Manufacturing PMI for April 30, 2026 at 1:45 am GMT

- Japan Housing Starts for March 2026 at 5:00 am GMT

- Japan Consumer Confidence for April 2026 at 5:00 am GMT

- France GDP Growth Rate Prel for March 31, 2026 at 5:30 am GMT

- Germany Retail Sales for March 2026 at 6:00 am GMT

- France CPI Growth Rate Prel for April 2026 at 6:45 am GMT

- Swiss KOF Leading Indicators for April 2026 at 7:00 am GMT

- Germany Unemployment Situation Update for April 2026 at 7:55 am GMT

- Germany GDP Growth Rate Flash for March 31, 2026 at 8:00 am GMT

- Euro area Unemployment Rate for March 2026 at 9:00 am GMT

- Euro area CPI Growth Rate Flash for April 2026 at 9:00 am GMT

- Euro area GDP Growth Rate Flash for March 31, 2026 at 9:00 am GMT

- Bank of England Monetary Policy Report & Official Bank Rate at 11:00 am GMT

- European Central Bank Interest Rate Decision for April 30, 2026 at 12:15 pm GMT

Thursday brings two major central bank events alongside a dense slate of European and Asia-Pacific data. The Bank of England will release its Monetary Policy Report and Official Bank Rate at 11:00 AM GMT, followed by the European Central Bank’s interest rate decision at 12:15 PM GMT. Both decisions arrive in a complex environment shaped by the Iran conflict-driven energy price surge and Wednesday’s hawkish Fed tilt. The ECB decision will likely draw focus on whether officials still see room for further easing given growth risks, or whether the persistent oil price shock warrants a more cautious stance. The BoE announcement comes alongside its quarterly Monetary Policy Report, which may include updated forecasts reflecting the energy shock’s impact on the U.K. inflation outlook.

Earlier in the European session, flash GDP readings from France at 5:30 AM GMT and Germany at 8:00 AM GMT will offer a first look at Q1 2026 growth momentum, followed by the euro area’s own flash GDP, CPI, and unemployment rate data simultaneously at 9:00 AM GMT. A combination of weak growth and above-forecast inflation would create an uncomfortable stagflationary backdrop for the ECB’s deliberations.

In the Asia-Pacific region, Japan releases industrial production and retail sales data late Wednesday evening GMT, alongside consumer confidence and housing starts early Thursday morning. China’s NBS Manufacturing and Services PMI for April arrives at 1:30 AM GMT and will be closely watched given ongoing trade and geopolitical disruptions. New Zealand’s ANZ Business Confidence for April is also due.

Stay frosty out there, forex friends!

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Most trading mistakes aren’t technical—they’re psychological. In the classic “Trading in the Zone” by Mark Douglas (⭐ 4.7★ | 10,000+ reviews on Amazon), you’ll learn how to master the probabilistic thinking and emotional discipline mentioned in today’s article. If you struggle with hesitation or breaking your rules, this is your manual for consistent execution.

Click on the link to learn more about “Trading in the Zone” by Mark Douglas!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.