Tuesday’s session was defined by crude oil’s relentless climb toward the $100 mark and a yen that surged, then surrendered its gains as Bank of Japan Governor Ueda’s cautious press conference dampened hopes for an imminent rate hike. The U.S. dollar closed as the best performing major currency of the day, while gold and equities retreated in a session shaped by stagflation anxiety as persistently elevated energy prices collided with softening U.S. labor market signals.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- U.K. BRC Shop Price Inflation for April 2026: 1.0% (1.4% forecast; 1.2% previous)

- Japan Unemployment Rate for March 2026: 2.7% (2.7% forecast; 2.6% previous)

- Bank of Japan Holds Rate at 0.75% in Closest Vote Yet Under Ueda

- ECB Consumer Inflation Expectations for March 2026: 4.0% (2.9% forecast; 2.5% previous)

- U.S. ADP Employment Change Weekly for April 11, 2026: 39.25k (54.75k previous)

- U.S. S&P/Case-Shiller Home Price for February 2026: 0.4% m/m (-0.2% m/m forecast; -0.1% m/m previous); 0.9% y/y (1.1% y/y forecast; 1.2% y/y previous)

- U.S. House Price Index for February 2026: 0.0% m/m (0.1% m/m forecast; 0.1% m/m previous); 1.7% y/y (1.6% y/y forecast; 1.6% y/y previous)

- Richmond Fed Manufacturing Index for April 2026: 3.0 (6.0 forecast; 0.0 previous)

- U.S. CB Consumer Confidence for April 2026: 92.8 (88.9 forecast; 91.8 previous)

- U.S. Dallas Fed Services Index for April 2026: -9.9 (-10.0 forecast; -13.3 previous)

- U.S. Money Supply for March 2026: 22.69 (22.8 forecast; 22.65 previous)

- President Trump said Tehran has asked the U.S. to lift its naval blockade of the Strait of Hormuz while peace negotiations continue, claiming Iran is in a “State of Collapse.”

Promoted: Protecting your trading capital starts with securing your access. Don’t let a weak password be the single point of failure for your brokerage or prop firm accounts. LastPass simplifies your digital life by generating and storing complex, encrypted passwords for every site you use.

Try LastPass for Free Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

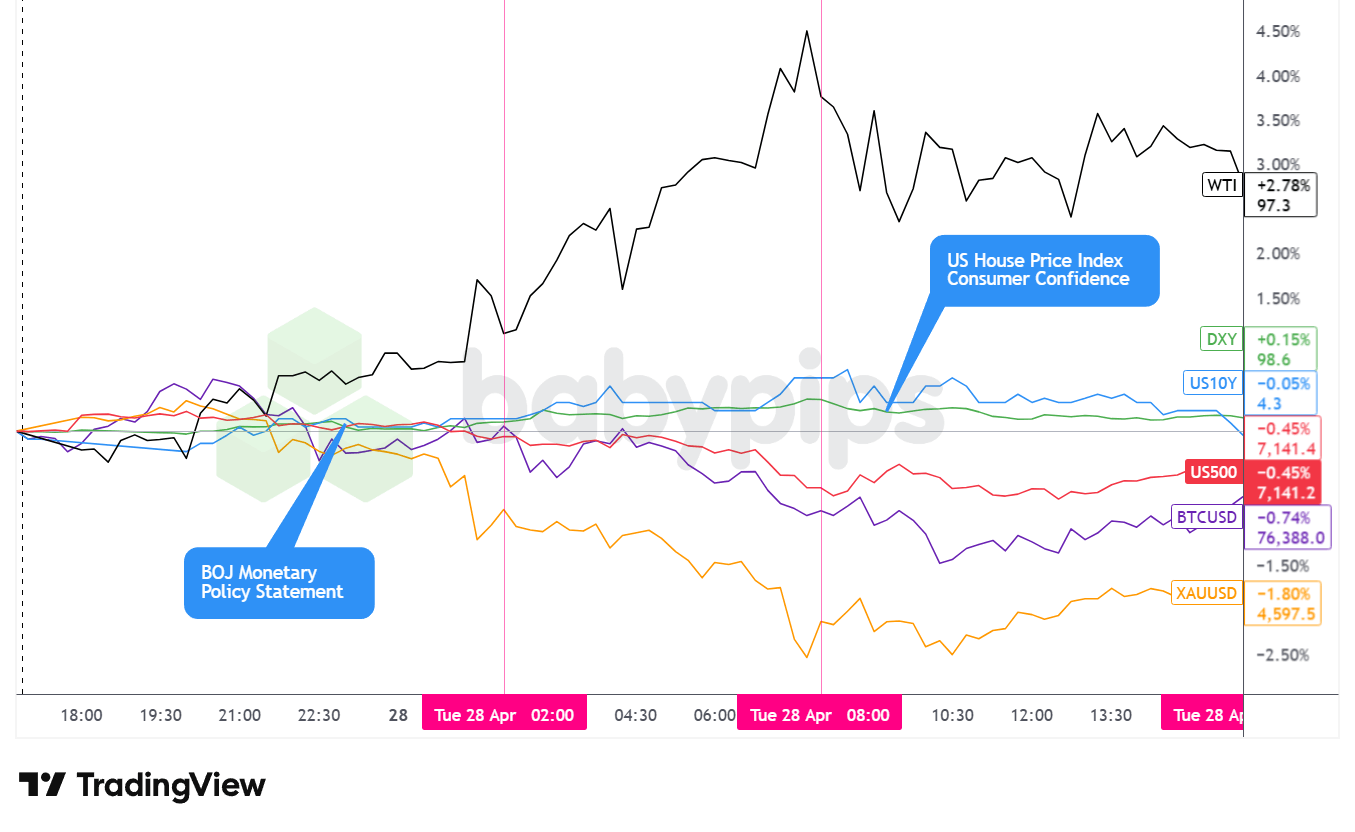

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Tuesday’s broad market price action suggested mounting stagflation anxiety, with crude oil surging on the prolonged Hormuz supply disruption while equities and gold retreated in a session defined more by geopolitical risk than domestic data surprises.

WTI crude oil was the session’s standout performer, climbing approximately 3.05% to close near $97.38 per barrel, its seventh consecutive session of gains. The advance appeared driven by the continued closure of the Strait of Hormuz and the lack of a clear near-term diplomatic resolution, with Trump signaling dissatisfaction with Iran’s latest nuclear proposals. The UAE’s decision to exit OPEC added further uncertainty to the supply outlook, though the near-term impact was likely muted given existing wartime production constraints.

Gold declined approximately 2.08% to close near $4,591.90 per ounce, making it the weakest performer among tracked major assets on the session. The precious metal sold off steadily throughout the Asian and early London sessions, with the move possibly reflecting a combination of profit-taking following a prolonged run higher and headwinds from a broadly stronger dollar. Gold found tentative support in the $4,555-$4,556 area before stabilizing during the U.S. afternoon.

The S&P 500 fell approximately 0.44% to close near 7,142. The decline appeared to reflect risk-off sentiment tied to rising energy prices and their potential to complicate the Federal Reserve’s easing path ahead of Wednesday’s FOMC decision. Shares of OpenAI-linked companies including SoftBank, Oracle, and CoreWeave added to the negative tone in technology-adjacent names, with broader risk aversion likely keeping buyers cautious into the close.

Bitcoin fell approximately 0.75% to close near $76,308, drifting lower alongside equities in a session that saw limited appetite for risk assets. The move was relatively contained compared to gold’s sharper decline, with Bitcoin trading within a relatively narrow range during the U.S. hours after a more volatile overnight session.

U.S. 10-year Treasury yields rose approximately 0.60% to close near 4.36%. The move higher possibly reflected concerns that persistently elevated oil prices could keep inflation sticky and complicate the Fed’s ability to ease, a theme likely to feature prominently at Wednesday’s FOMC press conference with Chair Powell.

Promotion: If your confidence has grown in your market awareness & strategies with this market recap, and you wanna take action, Maven Trading can help. They provide simulated funding challenges starting as low as $13, allowing you to trade major pairs with professional-sized capital. No time limits mean you can take swing plays on these market themes without the pressure of a ticking clock.

Learn More About Maven Trading Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

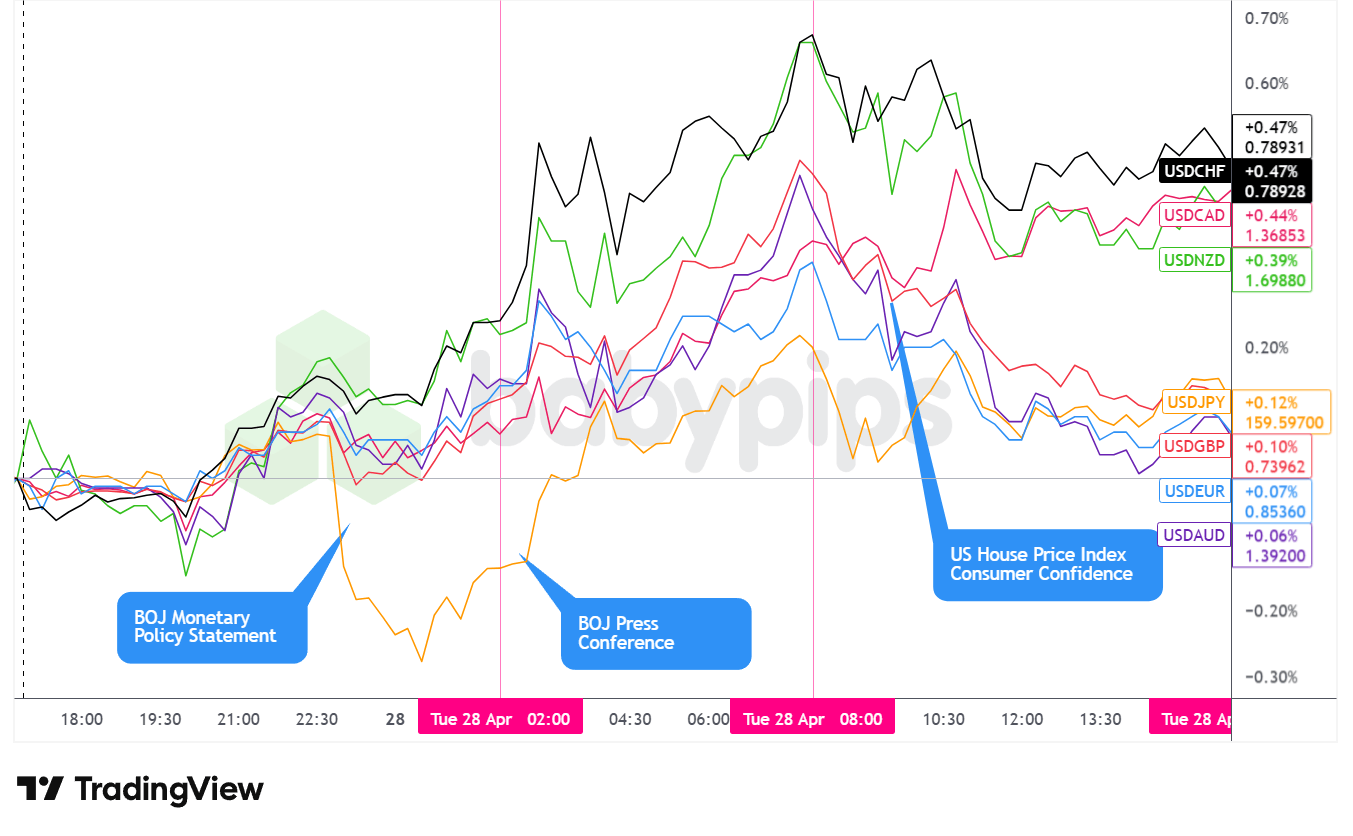

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar closed as the best performing major currency on Tuesday, advancing against all tracked majors despite an intraday reversal during the U.S. session that erased much of the day’s gains before the dollar stabilized into the close.

During the Asian session, the dollar traded with notably low volatility in the early going before bouncing higher around mid-morning Asia trade. The advance pulled back modestly before resuming, leaving the dollar with a net bullish lean against the major currencies heading into the London open. The session’s most significant event was the Bank of Japan’s policy decision. The initial 6-3 vote triggered a brief yen surge, with USD/JPY testing the 159.00 area as traders processed the closest Policy Board split under Ueda as a hawkish lean pointing toward a June rate hike. The yen’s gains proved short-lived, however.

During the London session, the dollar continued to move net higher against the major currencies as Governor Ueda’s press conference weighed on the yen. His acknowledgment that he did not know how many months it would take to gauge the timing of the next rate hike appeared to disappoint traders who had priced in a more hawkish lean from the lopsided vote, and the yen reversed to give back all of the initial post-decision gains. Adding to the session’s backdrop, the ECB’s consumer inflation expectations survey for March came in significantly above forecast at 4.0% versus 2.9% expected, with traders reportedly increasing ECB rate hike bets modestly following the data. The broader dollar strength during this window was broadly based, with gains against the franc, Canadian dollar, and commodity currencies also accumulating.

After the U.S. session opened, the dollar reversed lower against the major currencies. The reversal appeared to coincide with the release of mixed U.S. data: the ADP weekly employment reading came in at 39,250, well below the prior 54,750 reading, raising questions about labor market momentum ahead of the FOMC decision. Consumer Confidence for April beat expectations at 92.8 versus 88.9 forecast, while housing data was mixed. The dollar’s weakness during this window proved temporary, however, stabilizing during the U.S. afternoon session ahead of Wednesday’s high-stakes central bank calendar.

Upcoming Potential Catalysts on the Economic Calendar

- Australia CPI Growth Rate for March 2026 at 1:30 am GMT

- New Zealand RBNZ Gov Breman Speech at 1:30 am GMT

- Japan Housing Starts for March 2026 at 5:00 am GMT

- Swiss Economic Sentiment Index for April 2026 at 8:00 am GMT

- Euro area Monetary Developments for March 2026 at 8:00 am GMT

- Euro area Consumer Inflation Expectations for April 2026 at 9:00 am GMT

- Euro area Economic Sentiment for April 2026 at 9:00 am GMT

- U.S. MBA 30-Year Mortgage Rate & Applications for April 24, 2026 at 11:00 am GMT

- Germany CPI Growth Rate Prel for April 2026 at 12:00 pm GMT

- U.S. Building Permits Prel for March 2026 at 12:30 pm GMT

- U.S. Durable Goods Orders for March 2026 at 12:30 pm GMT

-

Bank of Canada Interest Rate Decision at 1:45 pm GMT

- BoC Press Conference at 2:30 pm GMT

- U.S. EIA Crude Oil Stocks Change for April 24, 2026 at 2:30 pm GMT

-

FOMC Funds Rate & Policy Statement at 6:00 pm GMT

- FOMC Press Conference at 6:30 pm GMT

Wednesday brings one of the most consequential calendar days of the week. In Asia, Australia’s CPI data at 1:30 am GMT could trigger significant AUD volatility, particularly given the broader inflation concerns stemming from elevated oil prices. RBNZ Governor Breman’s speech at the same time is worth monitoring for NZD direction.

During the European session, Germany’s preliminary April CPI at 12:00 pm GMT will be closely watched for early clues on whether energy-driven inflation is beginning to feed through more broadly into the eurozone’s largest economy. Euro area economic sentiment and inflation expectations data earlier in the morning will add to the picture ahead of the ECB’s own decision later in the week.

The Bank of Canada’s rate decision at 1:45 pm GMT, alongside its Monetary Policy Report and press conference, is the first major central bank event of the day. With USD/CAD ending Tuesday’s session near the high end of the day’s range, traders will be watching for any BoC commentary on the dual impact of elevated crude prices and U.S. trade policy uncertainty on the Canadian economic outlook.

The FOMC rate decision at 6:00 pm GMT and Chair Powell’s press conference at 6:30 pm GMT are likely the week’s single most market-moving events. With WTI crude back above $97 per barrel and the ADP employment reading disappointing, markets will be focused on how Powell balances energy-driven inflation persistence against early signs of labor market cooling, and whether the Fed signals any shift in its rate cut timeline.

Stay frosty out there, forex friends!

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Most trading mistakes aren’t technical—they’re psychological. In the classic “Trading in the Zone” by Mark Douglas (⭐ 4.7★ | 10,000+ reviews on Amazon), you’ll learn how to master the probabilistic thinking and emotional discipline mentioned in today’s article. If you struggle with hesitation or breaking your rules, this is your manual for consistent execution.

Click on the link to learn more about “Trading in the Zone” by Mark Douglas!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.