Geopolitical risk dominated Monday’s session as the collapse of US-Iran peace talks over the weekend and a US naval blockade of the Strait of Hormuz jolted markets at the open, only for Trump’s mid-session claim that Iran had reached out for a deal to spark a sharp recovery in risk assets.

Oil prices surged early but pared most gains by the close, equities rallied to multi-week highs, and the U.S. dollar reversed its early safe-haven bid to finish as one of the session’s weakest major currencies.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- US-Iran peace talks collapsed over the weekend in Islamabad, with the US announcing a naval blockade of the Strait of Hormuz effective April 13 at 10 a.m. ET. Iran warned it would target all ports in the Persian Gulf if its own shipping hubs are threatened.

- President Trump said Iran had reached out to his administration about a peace deal, stating “we’ve been called this morning by the right people.” Iran has not confirmed further negotiations. Trump reiterated there would be no deal without Iran abandoning its nuclear program.

- New Zealand Services NZ PSI for March 2026: 46.0 (50.6 forecast; 48.0 previous)

- On Monday, Bank of Japan Governor Ueda signaled a more cautious stance on additional rate hikes

- China Monetary Developments for March 2026

- China M2 Money Supply for March 2026: 8.5% (9.1% forecast; 9.0% previous)

- China New Loans for March 2026: 2,990.0B (2,250.0B forecast; 900.0B previous)

- Canada Building Permits for February 2026: -8.4% m/m (1.5% m/m forecast; 4.8% m/m previous)

- U.S. Existing Home Sales for March 2026: -3.6% m/m to 3.98M unites (-2.0% m/m forecast; 1.7% m/m previous)

- The Federal Reserve announced it will buy approximately $25 billion of Treasury bills per month in the period ending May 13, a larger-than-anticipated step-down from the $40 billion monthly pace in place since December 2025. Market participants had expected a more gradual reduction.

Promotion: Use TradeZella’s AI Powered trade journal to deep-dive into your execution and see exactly how you performed during today’s trading session.

Click here to get the TradeZella edge and use code PIPS20 to save 20% on your first purchase!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

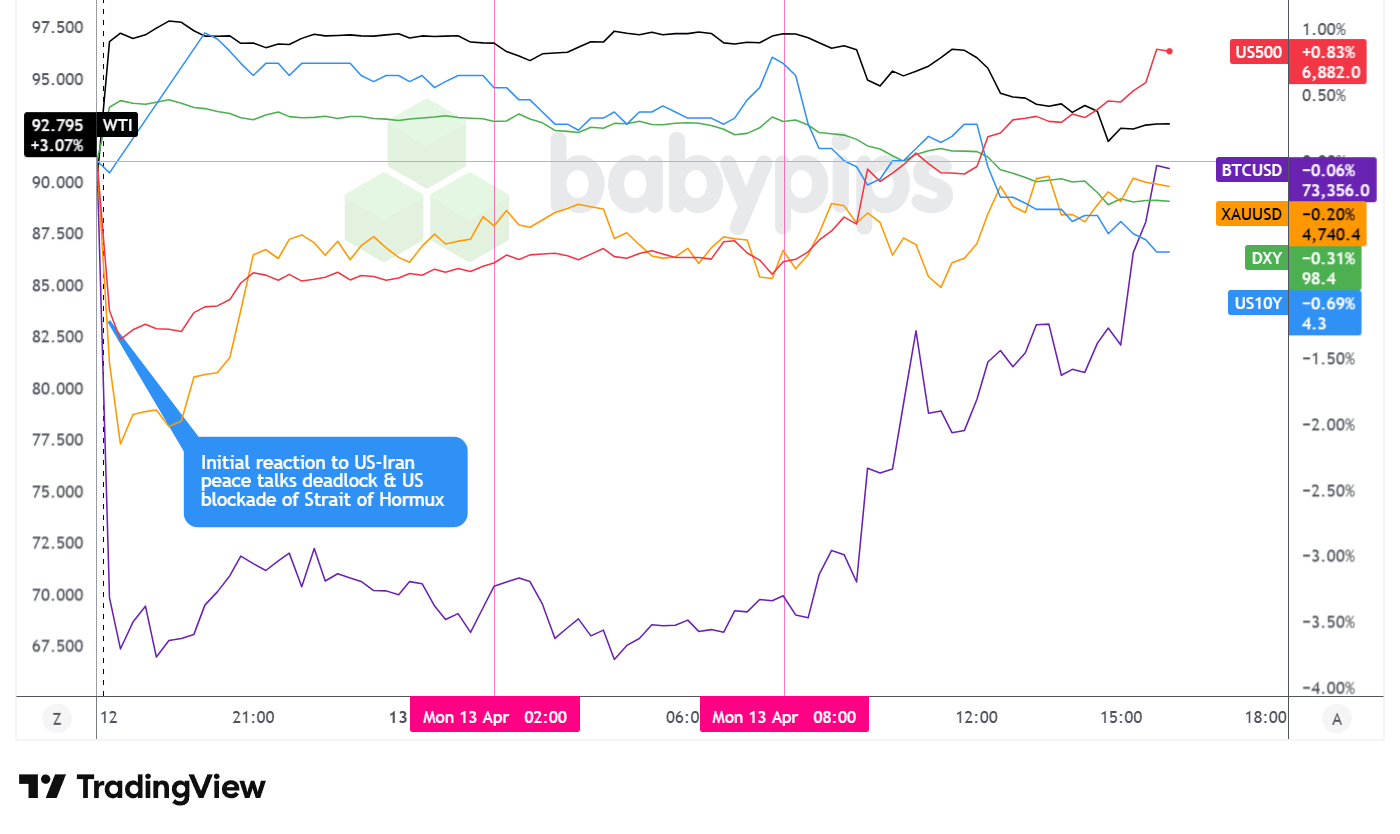

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Monday’s broad market story was one of sharp intraday reversal. The session opened with a pronounced risk-off shock as news of the failed US-Iran ceasefire extension talks and the formal start of a US naval blockade of the Strait of Hormuz hit markets, sending oil prices surging and putting pressure on risk assets. The mood shifted materially after President Trump stated that Iran had reached out to his administration seeking a deal, which helped pull oil off its highs and provided the equity market with the footing to push steadily higher through the afternoon.

The S&P 500 closed near 6,885, up approximately 0.88% on the day and at its highest level since early March. The index trended broadly higher from the London session onward, with the pace of gains accelerating after the Trump-Iran deal comments. Earnings season also got underway, with Goldman Sachs posting a mixed quarter that appeared to weigh on financials without disrupting the broader market’s upside. Analysts currently project roughly 12% annual earnings growth for the S&P 500 in Q1.

WTI crude oil was the session’s most volatile asset. Prices gapped higher on supply disruption fears, reaching above $97 early in the Asia-Pacific session, before gradually declining through London and the US afternoon as Trump’s deal comments eased the immediate worst-case energy market anxiety. WTI closed near $92.67, still up approximately 2.92% from the prior close. The intraday range — from above $97 to a close near $92 — illustrated how tightly oil remains tethered to headline risk around the conflict. WTI crude oil futures expiry next week is worth monitoring as a potential source of volatility.

Gold traded with notable intraday volatility. The precious metal initially spiked lower at the Asian session open before pulling back through London toward the $4,700-$4,710 area. It recovered through the US afternoon and closed near $4,743.6, still down for the day.

Bitcoin diverged sharply from the cautious tone seen in early trading. After consolidating in the $70,600-$71,300 range through most of the Asian and London sessions, BTC surged sharply around the US market open and continued higher through the afternoon, closing near $73,253.73, slightly red for the day.

The 10-year US Treasury yield rose early in the session, peaking near 4.36% around the London-to-US transition, possibly reflecting inflation concerns tied to the surge in crude prices and the escalating conflict. Yields then pulled back steadily through the US session, closing near 4.30%, down approximately 0.44% on the day. The reversal likely correlated with the broader easing of geopolitical risk sentiment following Trump’s deal comments, and possibly also reflected the broader bond market digesting the Fed’s sharper-than-expected step-down in T-bill purchases.

Promoted: Don’t Just Survive the Hormuz Whipsaw. Trade It.

The US-Iran stalemate is turning the charts into a minefield of intraday reversals. When oil gaps $5 and the Dollar Index flips on a single headline, you need more than just a strategy—you need the capital to execute. If your journal shows you navigated today’s risk-off-to-risk-on pivot with precision, don’t let a small account limit your edge. Tradeify’s Lightning accounts offer instant funding with no evaluation phase — so you can trade the next catalyst, US PPI updates, at the size your results deserve.

Get Instant Funding with Tradeify!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

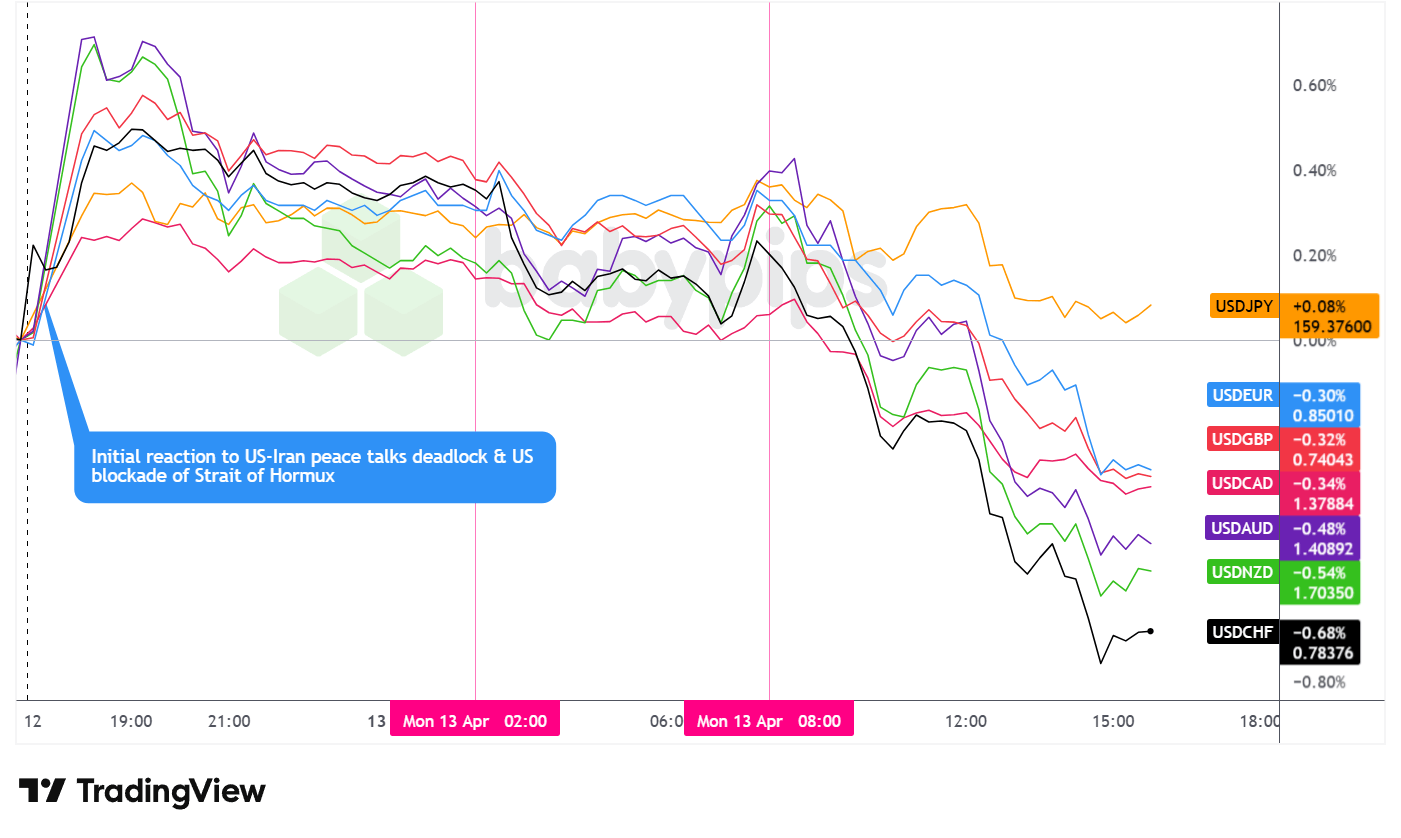

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar closed as one of the weakest major currencies on Monday, reversing an early safe-haven spike as risk sentiment recovered on hopes for a renewed US-Iran diplomatic channel and a broader pullback in crude prices.

During the Asian session, the dollar spiked higher at the open against most of the major currencies on net, likely reflecting initial safe-haven demand following the weekend collapse of US-Iran peace talks and the formal start of the Strait of Hormuz blockade. The move proved short-lived: the dollar quickly stabilized and pulled lower heading into the London session, suggesting the market moved quickly to price in the known risks and reassessed the escalation risk premium.

During the London session, the dollar continued to be volatile, extending its decline and trading net bearish against the majors heading into the US session open. European equity markets were lower but by relatively contained margins, and the broader risk mood was cautious rather than panicked. BOJ Governor Ueda’s speech, delivered by his deputy in Tokyo, signaled a notably more cautious stance on rate hikes amid Middle East uncertainty, and market expectations for an April BOJ hike were cut roughly in half. This dynamic likely provided relative support for USDJPY from a policy divergence standpoint even as broader dollar sentiment remained under pressure. The Hungary election result, removing Viktor Orbán, was seen as modestly euro-supportive at the margin.

After rebounding briefly just ahead of the US session open, the dollar reversed and traded back to the downside on net against the major currencies through the rest of the Monday US session. Weaker-than-expected US Existing Home Sales for March (actual: 3.98M, -3.6% m/m; forecast: -2.0% m/m) and a sharper-than-signaled reduction in the Fed’s T-bill purchase program offered additional headwinds for the greenback, though the primary driver appeared to be the broader risk-on shift after Trump’s deal comments reduced immediate safe-haven demand.

Upcoming Potential Catalysts on the Economic Calendar

- Australia RBA Hauser Speech at 10:15 pm GMT

- U.K. BRC Retail Sales Monitor for March 2026 at 11:01 pm GMT

- Australia Westpac Consumer Confidence Change for April 2026 at 12:30 am GMT

- Australia NAB Business Confidence for March 2026 at 1:30 am GMT

- China Balance of Trade for March 2026 at 3:00 am GMT

- Japan Industrial Production Final for February 2026 at 4:30 am GMT

- U.S. NFIB Business Optimism Index for March 2026 at 10:00 am GMT

- U.S. ADP Employment Change Weekly for March 28, 2026 at 12:15 pm GMT

- U.S. PPI for March 2026 at 12:30 pm GMT

- ECB Cipollone Speech at 3:00 pm GMT

- ECB Lane Speech at 3:30 pm GMT

- BoE Gov Bailey Speech at 4:00 pm GMT

- Fed Goolsbee Speech at 4:15 pm GMT

- Fed Barr Speech at 4:45 pm GMT

- Fed Collins Speech at 5:00 pm GMT

- BoE Greene Speech at 7:00 pm GMT

Tuesday’s calendar is dense with data and central bank speakers. The US PPI for March (12:30 pm GMT) arrives amid elevated energy price concerns and will be closely watched for evidence that oil-driven cost pressures are broadening into the broader producer price complex.

The ADP employment report (12:15 pm GMT) offers an early read on labor market conditions. Multiple Fed speakers, including Goolsbee, Barr, and Collins, may offer insight into how policymakers are weighing the inflation risk from elevated crude prices against a softening housing market and broader growth concerns.

On the European side, ECB’s Lane is scheduled to appear alongside Cipollone and President Lagarde, providing potential EUR volatility catalysts. BOE’s Bailey and Greene also speak, with markets watching for any updated guidance.

US-Iran geopolitical developments remain the dominant wildcard and could override any scheduled data at any point. Stay frosty out there, forex friends!

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Most trading mistakes aren’t technical—they’re psychological. In the classic “Trading in the Zone” by Mark Douglas (⭐ 4.7★ | 10,000+ reviews on Amazon), you’ll learn how to master the probabilistic thinking and emotional discipline mentioned in today’s article. If you struggle with hesitation or breaking your rules, this is your manual for consistent execution.

Click on the link to learn more about “Trading in the Zone” by Mark Douglas!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.