We found out yesterday that the U.S. economy actually grew less than what was initially reported.

The Final Q1 2013 reading only printed at 1.8% when the Preliminary version of the report came in at 2.4% while the Advance was at 2.5%. What a way to burst our bubble about growth in the U.S. economy, huh?!

Before we go any further, you should know that there are three versions of the U.S. GDP report: Advance, Preliminary, and Final.

The first two are based on incomplete data from different sectors of the economy and estimates from historical trends. Thus, this makes the GDP reading vulnerable to revisions often seen in the Final version when all the data become available.

However, it’s noteworthy to point out that the difference from the Advance and Final reading is a pretty big chunk. On average, revisions are only somewhere around 0.2% but in the Final reading we saw a 0.7% discrepancy. That’s more than thrice as much!

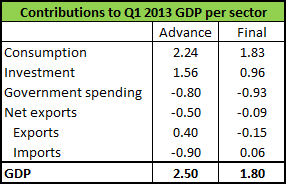

In order to make some sense out this, let’s break down the contribution of each sector to the GDP for Q1 2013.

Looking at the table to the left we can see that each component actually contributed to the chunky downward revision.

First, investment growth dropped from 1.56% to just 0.96% over the quarter.

Second, government spending continued its downward spiral, as it shrank even faster than expected last quarter. Apparently, Uncle Sam has cut back spending on all types of projects, and this led to a 0.93% decline in spending.

Third, net exports dropped for the second consecutive quarter, as export growth was revised from positive to negative. It appears not even the weakening of the dollar during the second quarter was enough to entice foreigners to ramp up their shopping of U.S. goods.

Lastly, and most importantly, consumer spending – which has the biggest contribution to the GDP figure – saw the largest downward revision of the four components. The numbers revealed that everyday Joes mainly cut back on vacations and legal advice.The culprit for this change in mindset? The two percent increase in payroll tax! Due to this implementation, consumable income saw its largest drop in four years!

Now that GDP growth wasn’t as fast as we had initially thought, what does this mean for us forex traders?

The revision could make Fed officials reconsider their plans. Remember that the central bank was actually thinking of tapering asset purchases sometime later this year.

For the most part, the Fed’s plans were based on an assumption that the labor market would continue its steady progress during Q1 2013 until the end of the year. However, these revisions could throw a curveball into those plans, as slower growth suggests that job gains may slow down as well.

Moving forward, we’ll have to pay special attention to labor market data as well as the advance GDP report for Q2 2013.

I think the latter could have a particularly large impact on the markets, as it could prove to be the make-or-break moment for the Fed to decide whether to taper bond purchases later this year or not.