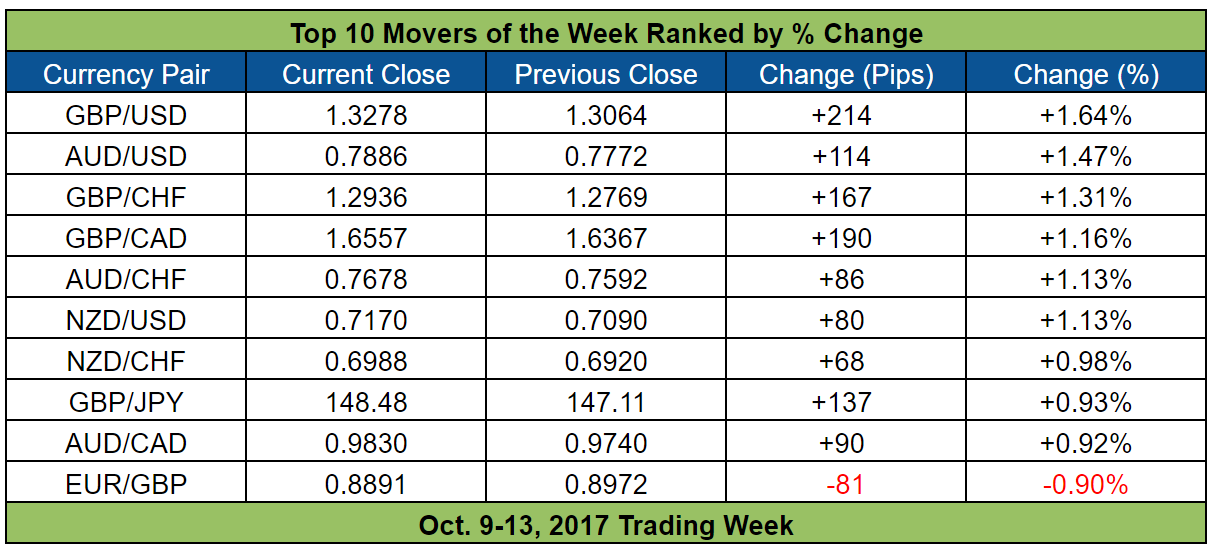

The forex trading week has come and gone, so it’s time to take a look at how the major currencies performed and what drove price action.

The pound showed broad-based strength and half of the top 10 movers are pound pairs, so pound strength is clearly a major theme this week. Other than that, Greenback weakness was also a major theme.

Great! But what about the other currencies? What drove their price action this week? Time to find out!

But before that, here’s this week’s scoreboard.

And if you only want to find out what happened to a specific currency, then you can just skip to that currency by clicking on it below.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The U.S. Dollar

The Greenback was the worst-performing currency of the week, putting an end to its four-week winning streak.

The Greenback had a mixed but somewhat steady start before starting to tank across the board on Tuesday. There weren’t really any major negative catalysts on Tuesday. However, most market analysts were attributing the Greenback’s slide to wavering faith in Trump’s tax reform plans because of the very public spat between Trump and Bob Corker, a Republican Senator from Tennessee, which the market apparently interpreted as a sign that the Republican Party is not united in backing Trump’s tax plans.

And the minutes of the most recent FOMC meeting didn’t really help in providing the U.S. dollar with some support.

You see, the minutes revealed that “nearly all [FOMC members] supported again indicating in the postmeeting statement that a gradual approach to increasing the federal funds rate will likely be warranted.”

However, the minutes also revealed that FOMC members were divided on their assessment and outlook on inflation. And it looks like the majority are leaning more towards a dovish view.

To quote directly from the minutes (emphasis mine):

“[M]any participants expressed concern that the low inflation readings this year might reflect not only transitory factors, but also the influence of developments that could prove more persistent, and it was noted that some patience in removing policy accommodation while assessing trends in inflation was warranted.”

“A few of these participants thought that no further increases in the federal funds rate were called for in the near term or that the upward trajectory of the federal funds rate might appropriately be quite shallow.”

“Some other participants, however, were more worried about upside risks to inflation arising from a labor market that had already reached full employment and was projected to tighten further.”

So, “many” Fed officials were wary of hiking further because the weakness in inflation might not be temporary. Meanwhile, “a few” were so blatantly dovish that they didn’t want more hikes. And only “some” Fed officials still had an upbeat outlook. That sounds lopsidedly dovish to me.

Moving on, the Greenback had a more mixed performance on Thursday but was mostly higher for the day, likely because of short covering by Greenback bears ahead of Friday’s CPI and retail sales reports.

And unfortunately (for dollar bulls), the Greenback got a final bearish kick on Friday, apparently as a reaction to the disappointing CPI report. The retail sales report, meanwhile, had mixed readings.

As for details, the September CPI report revealed that headline U.S. CPI only increased by 0.5% month-on-month, which is a tick slower compared to the consensus for a 0.6% rise. This is stronger than the previous month’s +0.4% reading. Like last time, however, the main driver was the surge in gasoline prices because of the disruption caused by the hurricanes (+13.1% vs. +6.3% previous).

Worse, the prices of non-food and non-energy commodities contracted at a faster pace (-0.2% vs. -0.1% previous) while the cost of services increased at a weaker rate (+0.2% vs. +0.4% previous).

These pointed to an underlying weakness in inflation, which is why the core reading only printed a measly 0.1% increase, missing expectations that it would match the previous month’s already subdued +0.2% increase.

Moving on to the September retail sales report, the headline value for retail sales rose by 1.6% during the September period. However, this missed expectations for a 1.7% increase. But on a more upbeat note, the 0.2% contraction reported back in August was revised to a less disappointing 0.1% contraction.

Looking at the details, the main driver was the 3.6% rebound in vehicles and parts sales (-2.1% previous). However, 6 of the remaining 12 store types also reported higher sales while 2 store types reported softer declines in sales, which is why the core reading was able to print a better-expected-reading (+1.0% vs. +0.9% expected, +0.5% previous).

Anyhow, there was no follow-through selling after the initial slump. Short-covering by dollar bears after a profitable week is certainly a possibility. However, it’s also probable that market players were taking into account the positive undertones of the retail sales report since odds for a December rate hike initially dropped but later climbed back up to end essentially unchanged at 82.9%, according to the CME Group’s FedWatch Tool.

Even so, the damage was already done. And so the Greenback ended up as this week’s weakest currency.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Euro

The euro had another mixed performance this week. However, a quick glance at the overlay of euro pairs above shows that the euro had roughly uniform two-way price action, since it broadly rallied from Monday to Wednesday before sliding on Thursday and Friday.

The early rally was attributed by market analysts mainly to fading concerns over Catalonia and expectations that the ECB may announce a taper to its asset purchases during the ECB statement less than two weeks from now.

As for the later slide, profit-taking ahead of ECB Overlord Draghi’s speeches is a possibility after a profitable week for euro bulls.

As to what Draghi had to say, well, he said during his Thursday speech that interest rates aren’t budging anytime soon. In fact, the ECB will maintain interest rates at accommodative levels “well past” the ECB’s QE program.

Other than that, Draghi also talked about the lackluster wage growth while refusing to comment on the ECB’s plans to taper its QE program.

During his Friday speech to the IMF, meanwhile, the Dragster sounded even more blatantly dovish when he said that:

“Progress towards a durable and self-sustaining convergence of inflation towards our objective is not yet sufficiently convincing.”

“Thus, a very substantial degree of monetary accommodation is still needed.”

Anyhow, the euro’s early rise and later fall are the reasons why the euro had a mixed performance this week, even though price action across euro pairs was roughly uniform.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Pound Sterling

After getting stomped and kicked to the bottom of the forex heap last week, the pound ended up doing all the stomping this week since it was this week’s king of pips (or queen, if you like).

But as you probably saw in the overlay of GBP pairs, the pound’s path to the top wasn’t a cakewalk. And as you also probably noticed, there were a ton of events that kicked the pound around, so prepare yourself for a wall of text.

But if you want the really short version, then just know that net positive economic data and easing Brexit-related and political worries, as well as rumors that the E.U. may present a proposal for a transitional deal (perhaps as early as next week), helped the pound to climb higher this week. That’s it. The rest are just details, but you still may wanna read them since you may pick up additional insights (also, it took a while for me to type them all out),

Having said that, the pound hit the ground running as bulls began bidding the pound higher when the new trading week opened, thanks to news over the weekend that Theresa May plans to reshuffle her cabinet in order to have firmer control in government, as well as rumors making the rounds at the time that the U.K. office for National Statistics (ONS) will supposedly issue corrections because it made a mistake when calculating the U.K.’s unit labor costs.

And as it turns out, to ONS did release a revised labour productivity report which showed that unit labour costs in the U.K. increased by 3.5% in Q1 2017, which is much better than the original estimate of +2.1% and is the strongest reading in four years to boot.

Not only that, the reading for Q2, was revised significantly higher from +1.6% to +2.4%, which is the second strongest reading since Q2 2013.

And according to some market analysts, the corrections caused odds for a November BOE rate hike to rise, very likely because the reading for Q2 is substantially better than the BOE’s forecast of +1.0%, as laid out in the August Inflation Report.

Aside from news over the weekend and the confirmed rumor that the ONS will upgrade the U.K.’s unit labour costs, the pound also got a lift when the BBC released snippets of U.K. Prime Minister Theresa May’s speech about Brexit since those snippets revealed a somewhat conciliatory tone that likely helped to ease Brexit-jitters a bit

After that, the pound encountered selling pressure a few hours before Theresa May’s speech, likely because of profit-taking by pound bulls who got in early.

And during Theresa May’s speech itself, the pound found even more sellers, very likely because Theresa May also revealed that plans for a “no deal” scenario “is under way,” which likely reignited Brexit-related jitters.

Still, May’s tone was conciliatory overall, which is probably why follow-through selling was minimal and the pound even found buyers and continued trending higher later.

More pound bulls were enticed to jump in later on Tuesday after the U.K. released a slew of economic data that were net positive overall.

As for specifics, total industrial production in the U.K. during the August period increased by 1.6% year-on-year, which is much faster than the expected 0.9% increase and marks the fourth consecutive month of ever stronger readings. In addition, the previous month’s +0.4% reading was revised significantly higher to +1.1%.

And the stronger reading for total industrial production, in turn, was driven mainly by higher-than-expected manufacturing output (+2.8% vs. +1.9% expected, +2.7% previous).

Another positive economic report was the U.K.’sonstruction output report since that printed a 3.5% year-on-year sruge in August, very soundly beating expectations for a modest 0.2% increase in output. Moreover, the previous month’s reading of a 0.4% contraction was revised to show a solid 2.7% increase instead.

The only disappointing economic report was the U.K.’s trade report since that showed that the U.K.’s trade gap widened from £4.24 billion to £5.62 billion between the months of July and August.

But on the brightside, exports rose by 0.63% after two consecutive months of heavy declines. It just so happens that imports surged by 3.15%, which is why the U.K.’s trade gap still widened.

Anyhow, the pound continued to trend higher before trading roughly sideways while tilting a bit to the downside on Wednesday, likely because of Finance Minister Hammond’s warning about the Brexit “cloud of uncertainty” that looms over the U.K. economy.

Hammond also repeated Theresa May’s Monday statement that the government has plans for a “no-deal” scenario. However, Hammond also said that “Some [U.K. officials] are urging me to spend money [on no-deal contingencies] simply to send a message to the EU that we mean business. I think the EU knows that we mean business.”

Still, the pound later found dip buyers and resumed its upward march before finding sellers later, likely because of unwinding by pound bulls ahead of Barnier and Davis’ joint conference, as well as a reaction to the BOE’s credit conditions survey for Q3 2017 since that showed that lenders expect unsecured consumer credit availability to contract at the fastest pace since Q4 2008, which hint at tightening financial conditions.

And tighter financial conditions, in turn, are not really very favorable for rate hike odds. After all, hiking rates would only serve to make loans even more expensive than they already are.

Moving on to Barnier and Davis’ joint statement to conclude the fifth round of Brexit negotiations, that event wasn’t very favorable for pound bulls since Barnier, the E.U. top Brexit negotiator, had this to say with regard to the bill that the U.K. has to pay before leaving the union:

“On this question we have reached a state of deadlock which is very disturbing for thousands of project promoters in Europe and it’s disturbing also for taxpayers.”

Moreover, Barnier said that talks on a trade deal aren’t expected to start any time soon when he said that:

“I am not able in the current circumstances to propose next week to the European Council that we should start discussions on the future relationship.”

Brexit Secretary Davis, meanwhile, said that “there is still work to be done, much work to be done.”

Moreover, Davis said that the U.K. is not yet ready to pay up and that the details on the U.K.’s financial obligations should be discussed at a later time when he said that:

“In line with the process agreed at our last round of talks, we have undertaken a rigorous examination of the technical detail where we need to reach a shared view. This is not a process of agreeing specific commitments – we have been clear this can only come later.”

Given the “deadlock” on the U.K.’s Brexit bill and lack of progress on a trade deal, the pound found itself getting drowned by sellers because of renewed Brexit-jitters.

After getting the stuffing beaten out of it, the pound found dip buyers and began to swim against the bearish tide. However, it wasn’t until Germany’s Handelsblatt newspaper released a report that cited unnamed E.U. diplomats as allegedly saying that the E.U. may offer the U.K. a two-year transitional Brexit deal perhaps as early as next week.

That apparently eased Brexit-related jitters, market analysts say, which is very likely why the pound skyrocketed, erasing its losses (and then some).

There was follow-through buying on the pound on Friday and it helped that the BBC released a report saying that it got a peek at a draft document of the E.U.’s plan for a future deal with the U.K., which seems to affirm the earlier Handelsblatt report.

However, the pound stumbled a bit when European Commission President Jean-Claude Juncker said on Friday the the U.K. still has to pay up before leaving. After that, the pound’s price action became more mixed.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Swiss Franc

The Swissy was a major loser this week, even though the euro was mixed. And if you’re getting a sense of déjà vu, then that’s because that’s also what happened last week.

So, has the positive correlation between the Swissy and the euro’s price action finally been broken? Nope!

As marked above, however, the Swissy initially diverged from the euro’s price action, with the Swissy tumbling even as the euro began climbing higher. And this divergence is the reason why the Swissy fared worse than the euro, even though their price action was quite similar.

As to why the Swissy tanked at the start of the week, there’s no direct catalyst for that. Although it’s highly likely that the divergence was because of fading concerns over Catalonia.

After all, the narrative was that jitters over Catalonia were beginning to fade, which helped to drive the euro’s rally. However, if you stop and think about, easing jitters over Catalonia means less safe-haven demand for the Swissy, so the initial divergence does make sense. Of course, it’s also possible that the SNB was using the opportunity to try and kick the Swissy lower.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Japanese Yen

The yen had a mixed performance this week, even though bond yields slumped hard, which should have given the yen a bullish boost.

And looking at the overlay of inverted yen pairs and the benchmark 10-year U.S. bond yields above, we can see that yen pairs roughly tracked bond yields on Monday and Tuesday before diverging on Wednesday and then becoming a complete mess on Thursday.

The yen then roughly tracked bond yields again come Friday before becoming a mess again after the U.S. CPI report was released.

As to why the yen’s price action diverged from bond yields on Wednesday and the yen became vulnerable to opposing currency price action after that, well, there wasn’t really any direct catalysts for that. However, global equities were in rally mode on Wednesday.

Actually, most of the major global equity indices were already climbing higher since Monday. However, most European equity indices only joined the fray on Wednesday because of easing concerns related to Catalonia, market analysts say. And that likely helped to dampen demand for the safe-haven yen, making it vulnerable to opposing currencies.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Canadian Dollar

As usual, the Loonie didn’t really track oil prices since oil rallied hard this week but the Loonie ended up being a net loser.

- U.S. crude oil up (CLG6) by 4.30% to $51.41 per barrel for the week

- Brent crude oil up (LCOH6) by 2.80% to $57.18 per barrel for the week

And as you saw in the overlay of CAD pairs earlier, the Loonie’s price action was rather chaotic with lots of diverging price action, which is a sign that the Loonie was vulnerable to opposing currency price action this week.

Canada released a bunch of housing data this week, but they didn’t do diddly-squat for the Loonie’s price action.

Also, BOC Senior Deputy Governor Carolyn Wilkins spoke on Tuesday but the Loonie’s price action was like chop suey or a mixed bag of nuts, likely because Wilkins didn’t really talk about the Loonie or monetary policy, expressing only some concern about the levels of household debt (which is not really new).

However, some market analysts say that the Loonie did try to track oil prices. It just so happens that worries related to NAFTA after Trump made fresh demands supposedly raised doubts that renegotiations will succeed, dampened demand for the Loonie in the process. Well, that’s what some market analysts say anyway.

Hopefully we’ll get more uniform price action from the Loonie next week since Canada’s CPI report is scheduled for release on Friday.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Australian Dollar

As I’ve been noting in the past few weeks, the positive correlation between the Aussie and iron ore appears to have been broken, or no longer as strong at least. And as I’ve also been noting, the Aussie appears to track gold prices more nowadays.

And since there wasn’t really much in terms of top-tier catalysts for the Aussie during the week, the Aussie apparently took directional cues mainly from gold.

But as you can see below, the Aussie also took some directional cues from iron ore. This can be seen on Monday when gold (and most other commodities) climbed higher but the Aussie found itself getting kicked lower instead.

This can also be seen on Tuesday when gold continued to rally but most Aussie pairs were leaning towards the downside, which is more in-line with iron ore’s price action.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The New Zealand Dollar

The Kiwi started the week by gapping lower across the board, by news over the weekend that the final tally for the New Zealand election gave Labour and the Greens a combined 54 seats, which are enough to mount an effective challenge against National’s 56 seats.

Not only that, New Zealand First (NZF) got 9 seats, which are more than enough to get either National or a Labour-Greens coalition over the 61 seats needed to form a government. As such, NZF gets to be the “kingmaker” in New Zealand.

And all of that, quite obviously, point to another week of political limbo/drama/entertainment/uncertainty, which is why the Kiwi gapped lower across the board when the new trading week opened.

After that, the Kiwi climbed higher and closed the gaps on most pairs before before resuming its slide against everything except the Greenback, which had its own issues to deal with.

However, the Kiwi began to find support late Wednesday and even began trading higher across the board come Thursday, even though there were no apparent catalysts.

The likely reason for this was short covering by Kiwi bears since NZF’s Winston Peters was expected to make an announcement on Thursday on whether to support National or a Labour-Greens coalition.

However, Peters later said that he won’t be announcing NZF’s decision on Thursday, which probably triggered relief buying as well.

Aside from short covering by Kiwi bears and relief buying by Kiwi bulls, it’s also probable that interest rate differentials favored the Kiwi since the CME Group’s FedWatch Tool showed that odds for a December Fed rate hike hovered between 87% and 88% from Monday until Wednesday before the FOMC minutes were released.

However, odds for a December Fed rate hike dropped to 82.7% when the minutes were released late on Wednesday.

And since the Fed was deemed to be a bit less likely to hike, that probably sent some capital flows towards the higher-yielding Kiwi.

This can also be seen on Friday when the disappointing U.S. CPI report caused odds for a December rate hike to drop, which pushed the Kiwi higher against everything except the Aussie, which is another higher-yielding currency.

However, odds for a December rate hike recovered later, which also forced the Kiwi to return some of its hard-earned gains.

By the way, NZF’s Peters said late on Friday that the party board and caucus will be meeting this Monday and may finally be able to come to a decision before the end of next week, so it looks like politics will continue to have an effect on NZD’s price action for yet another week, which is good news for volatility junkies, I suppose.