The Swiss National Bank (SNB) kept its policy rate at 0% on June 18, right in line with market expectations.

So why did the Swiss franc still get smoked on Thursday?

Turns out, a two-word language tweak and one very telling silence at the press conference moved CHF more than the rate decision itself.

What Did the SNB Actually Decide?

Holding at 0.00% interest rate was a deliberate positioning choice, not a passive default.

If the SNB had raised rates, it might’ve made Swiss assets more attractive compared to other major markets. That could’ve pulled more money into Switzerland and pushed the franc even higher. Great for CHF bulls, not so great for Swiss exporters trying to sell stuff abroad.

On the flip side, cutting rates back below zero would’ve brought its own headaches. The SNB used negative rates for years before 2022, but going back would hit Swiss banks and squeeze profit margins across the financial sector.

So zero is the SNB’s sweet spot for now. It’s easy enough to support growth, but not so easy that it looks like the bank is panicking.

Aside from the rate decision, the SNB gave traders three things to watch.

First, it raised its inflation forecasts just a tiny bit. The bank now sees CPI at 0.6% in both 2026 and 2027, then 0.7% in 2028. That’s only 0.1 percentage points higher than its March forecasts, so we’re not exactly talking about an inflation scare here.

Swiss CPI did climb from 0.1% in February to 0.6% in May, but the SNB said that was mostly because of energy prices tied to the Middle East conflict. It also noted that “the contribution of other goods and services was negligible.” Translation: underlying inflation still looks pretty tame.

Second, the SNB kept its growth forecasts unchanged. It still expects the Swiss economy to grow by about 1% in 2026 and 1.5% in 2027, and even calls the economy “resilient” despite the conflict backdrop.

Third, and this is probably the line CHF traders cared about most, the SNB changed how it talked about FX intervention. In March, the bank said it was ready to act in the currency market. This time, it said: “If necessary, the SNB has an increased willingness to intervene in the foreign exchange market.”

It’s not a total policy shift, but it’s not throwaway wording either. The SNB basically told markets it’s getting more uncomfortable with franc strength, and traders heard it loud and clear.

Promoted: Trade the SNB’s Dovish Shift Without Putting Your Own Capital at Risk.

When central bank wording alone is enough to trigger a session-long slide, the real question isn’t whether there’s a trade. It’s whether you have enough capital to make your conviction count.If the widening rate gap between the SNB and its major peers has you eyeing CHF weakness for continuation, Funded Trading Plus can scale up your position. Evaluation packages start at just $89.00 with straightforward, fair rules — and traders can grow up to $2,500,000 in funded capital by doubling their account every 10%.

Learn more about Funded Trading Plus!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

What Did the Press Conference Signal?

With central banks, wording changes usually aren’t accidents. In this case, “if necessary” did a lot of heavy lifting, shifting the SNB’s intervention stance from a standing threat to a conditional warning.

When reporters asked SNB Chairman Martin Schlegel why the wording had changed, he declined to explain. Markets seemed to read that silence as a sign that the SNB isn’t in a rush to fight franc strength right now. The bank told traders the tool exists, but it didn’t say the tool is loaded and ready to fire.

The bigger takeaway isn’t that the SNB suddenly doesn’t want to fight franc strength. It’s that the bank doesn’t seem eager to make up for its ultra-easy policy stance with aggressive FX intervention either. With no rate hikes on the table and no clear standing threat to step into the currency market, the franc looks like it’s being left with less central bank support than traders had priced in.

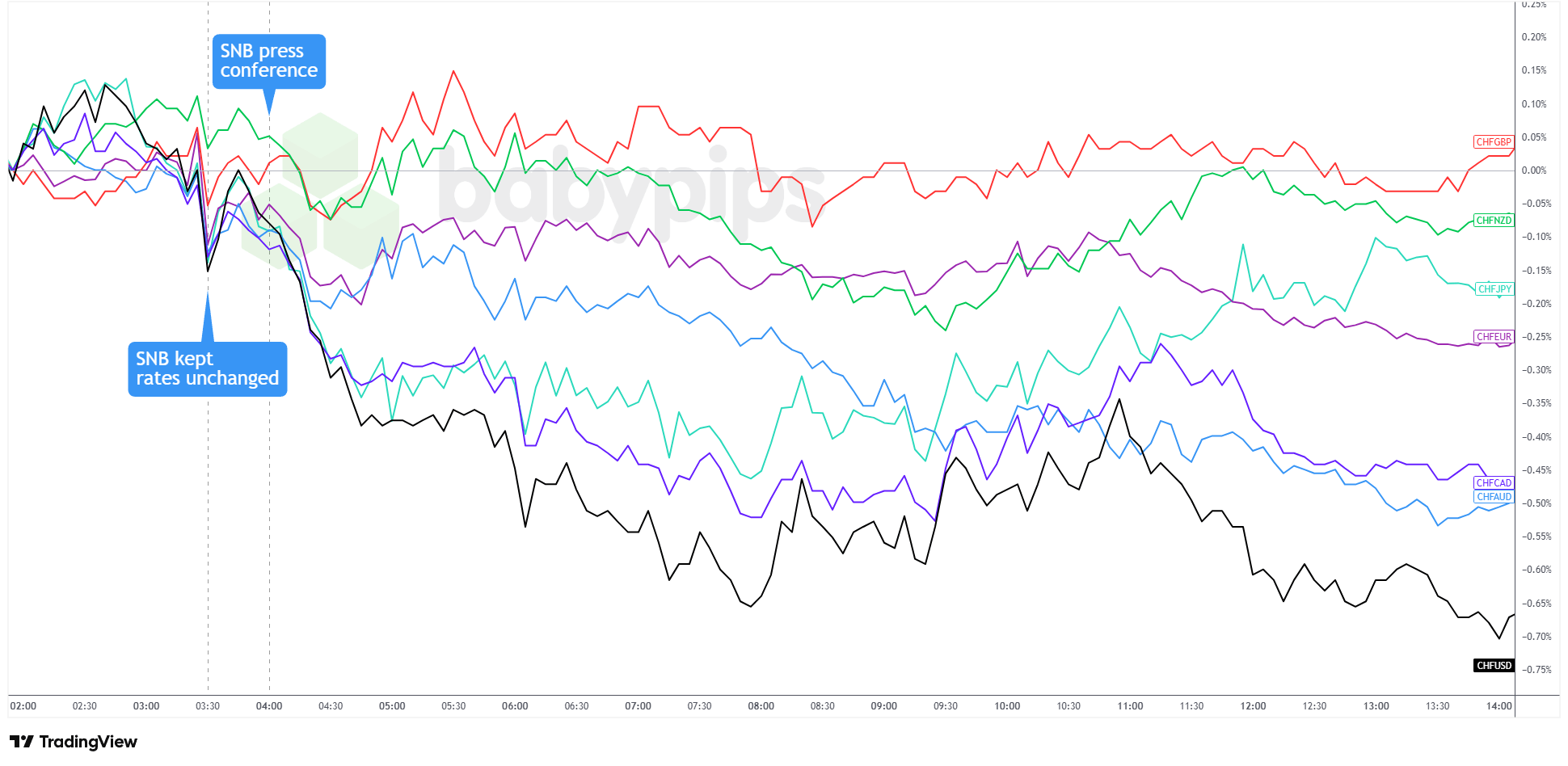

This is likely why the franc selloff was quick and broad. As the 5-minute chart below shows, CHF started weakening as soon as the statement dropped, then pulled back a bit before sliding through the press conference and across the European and U.S. sessions without much of a bounce.

CHF 5-Minute Forex – Chart Faster with TradingView

CHF/USD and CHF/AUD took the biggest hits by the end of the day, closing down nearly 0.65%, while CHF/GBP barely moved as Bank of England-related pound weakness offset franc weakness. This kind of steady, session-long decline looks more like real repositioning than a quick emotional spike.

Schlegel later reinforced the conditional tone on CNBC, saying: “Uncertainty is still very high, so much depends on the situation in the Middle East, and also a strong and rapid appreciation of the Swiss franc could endanger price stability in Switzerland. Therefore, we still have this increased willingness to intervene in the FX market.”

In other words, the SNB still has the tool, but it seems to be saving it for genuine stress rather than using it as a permanent safety net.

What Does This Mean for CHF?

The near-term setup for the franc still looks soft.

With the ECB hiking last week and the Fed signaling more tightening ahead, Switzerland’s rate gap with its major peers is widening. Investors can earn more elsewhere, so franc-based assets don’t look quite as attractive right now.If traders know the SNB is willing to sell francs when CHF gets too strong, then holding bullish franc bets becomes a lot less comfortable. Nobody wants to be caught on the wrong side of a central bank with a big balance sheet and very little patience.

This is also why Schlegel’s refusal to explain the wording change felt dovish. The SNB didn’t have to spend a single franc to move the market. All it had to do was sound less eager to step in, and traders took the hint.

There is one political wrinkle, though. Actual intervention could get awkward fast.

Switzerland is facing a 39% U.S. tariff rate, partly tied to long-running American complaints about currency manipulation. That refers to a country deliberately keeping its currency weak to help exporters. So if the SNB does jump into the FX market to weaken the franc, the move wouldn’t just matter for CHF pairs. It could also stir up fresh political noise with Washington.

Watch For

The SNB’s next policy decision is set for September 2026, but CHF traders may not need to wait that long for fresh direction.

The two big drivers to watch are the Middle East ceasefire progress and rate signals from the ECB and Fed. Any escalation could revive safe-haven demand for the franc, while a de-escalation could keep pressure on CHF.

At the same time, if the ECB and Fed keep sounding more hawkish than the SNB, wider rate gaps could make franc-based assets less attractive. That would help cool CHF strength without the SNB having to lift a finger.

The SNB held rates at zero and the Swiss franc still sold off across the board, and the reason comes down to a subtle but significant shift in how the central bank talked about currency intervention. Premium members can read our lesson:

📖 Hawkish vs. Dovish: How to Read Central Bank Language

Reading this helps you understand how central bank language shapes currency moves, why a wording change at a press conference can carry more weight than the rate decision itself, and how to identify a policy signal when a central bank chooses its words very carefully.

And if you’re not a Premium subscriber yet, now’s a good time to sign up.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just what the rate decision was, but the language signals behind it and why the SNB’s wording shift moved CHF when the actual decision moved nothing.