U.K. CPI rose to 3.3% year-on-year in March 2026, up from 3.0% in each of the two prior months, marking a three-month high and delivering the first hard data showing the Iran war’s impact on British consumer prices. The jump was driven almost entirely by a sharp surge in fuel costs after the conflict brought Persian Gulf energy exports to a near standstill.

On a monthly basis, CPI rose 0.7% in March, compared with a rise of just 0.3% in the same month a year earlier. The broader CPIH measure — which includes owner-occupiers’ housing costs and is the ONS’s most comprehensive gauge — rose to 3.4% annually, up from 3.2% in February.

Key Takeaways

-

CPI (y/y): 3.3% in March 2026, up from 3.0% in February 2026

- Core CPI ex-energy, food, alcohol, and tobacco (y/y): +3.1%, down from +3.2% — lowest since September 2021

- CPI (m/m): +0.7% in March 2026, compared with +0.3% in March 2025

- Transport (y/y): +4.7%, fastest since December 2022; motor fuels +8.7% (m/m), largest gain since June 2022

- Housing and household services (y/y): +5.3%, up from +4.6% in February 2026, driven by a surge in domestic heating oil

- Food and non-alcoholic beverages (y/y): +3.7%, up from +3.3% in February 2026

- Services inflation (y/y): +4.5%, up from +4.3% in February 2026

- Clothing and footwear (y/y): -0.8%, steepest decline since March 2021

- Petrol averaged 140.2p/litre in March 2026, highest since August 2024; diesel averaged 158.7p/litre, highest since November 2023

The war that began on February 28 quickly fed through to prices, with motor fuel jumping 8.7% on the month and pushing transport inflation to 4.7% annually, its fastest pace since late 2022. Petrol averaged 140.2p per litre while diesel surged to 158.7p, both hovering near recent highs.

Broader price pressures also picked up, as housing costs rose 5.3% annually on higher heating oil and food inflation accelerated to 3.7%, with gains across key categories and more supply chain pass-through from energy still ahead. Services inflation edged up to 4.5%, driven in part by a sharp rise in airfares as early Easter demand lifted long-haul travel costs.

One offset came from clothing, which fell 0.8% annually as retailers discounted amid soft demand, while core CPI dipped slightly to 3.1%, suggesting underlying price pressures remain relatively contained even as the headline rate climbed.

Link to official ONS U.K. CPI (March 2026)

Before the war, inflation had been drifting toward the Bank of England’s 2% target, and rate cuts were widely expected this year.

That outlook has shifted as the energy shock feeds into the data and more pressure builds, with gas and electricity prices set to rise in July and food producers signaling further pass-through.

With that backdrop, the BOE’s Monetary Policy Committee is expected to hold rates at 3.75% on April 30 while gauging how far the shock spills into wages and broader prices. Money markets are pricing in a one-quarter-point hike with roughly even odds of another, though many economists still see weak demand and a soft labor market keeping the BOE on pause.

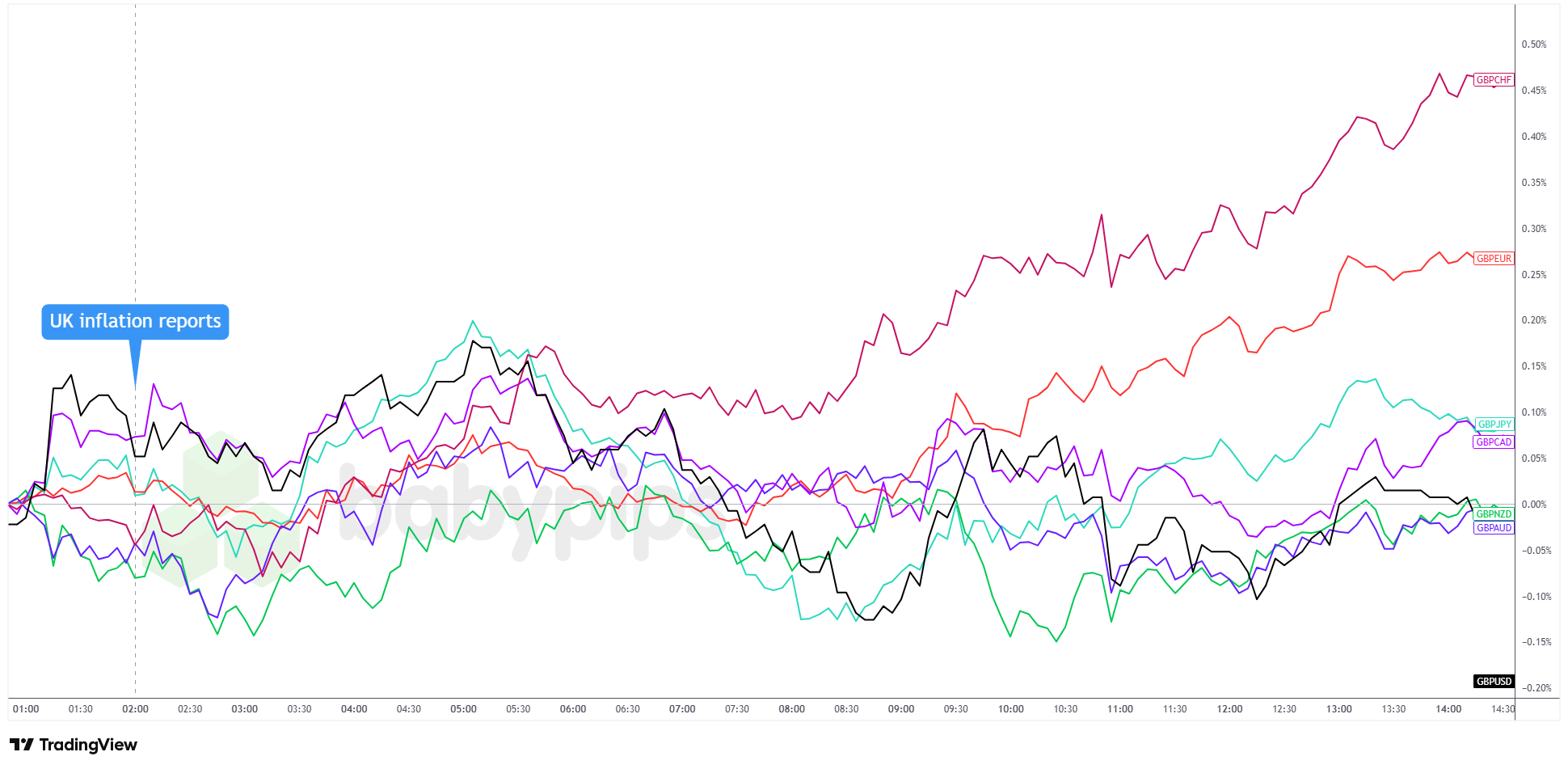

Market Reactions

British Pound vs. Major Currencies: 5-min

Overlay of GBP vs. Majors – Chart Faster with TradingView

GBP/CHF and GBP/EUR emerged as the day’s standout performers, climbing to roughly +0.45% and +0.25% respectively by the afternoon as the higher inflation print lent some support to expectations that the BOE would keep rates elevated for longer, with GBP/JPY and GBP/CAD also managing to hold modest positive territory through the close.

GBP/NZD was the notable laggard on the day. At the same time, GBP/AUD and GBP/USD spent most of the day hovering near flat, caught between the competing pulls of a hawkish inflation backdrop and ongoing uncertainty over how far the Iran conflict would continue to weigh on global risk sentiment heading into the BOE’s April 30 decision.

Promoted: Fuel-driven CPI is shifting BOE expectations, but muted price action shows how tricky trading macro surprises can be.

When volatility hits, small accounts often can’t capitalize even with the right bias. Alpha Capital Group gives you access to simulated funded accounts so you can trade these setups with proper size.

Learn more about Alpha Capital Group!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.