The Bank of Canada left its policy rate unchanged at 2.25% on July 15, pointing to a resumption of economic growth and a gradually improving inflation picture, while flagging elevated uncertainty tied to the Middle East conflict and the US trade relationship.

The decision was accompanied by the release of the July Monetary Policy Report (MPR) and a press conference from Governor Tiff Macklem and Senior Deputy Governor Carolyn Rogers.

Key Takeaways from July BOC Statement

- Policy rate held at 2.25% — Bank Rate at 2.5%, deposit rate at 2.20%, unchanged from the prior meeting.

- Growth resuming — Canadian GDP is estimated to have grown 2.5% in Q2 2026, rebounding after growth stalled in Q1; the Bank projects 0.7% growth for all of 2026 and 1.8% in both 2027 and 2028.

- Inflation elevated but expected to ease — CPI inflation rose to 3.2% in May, largely due to higher gasoline prices; core inflation has stayed close to 2%. The Bank expects headline inflation to return to the 2% target by early 2027.

- Labour market still soft — unemployment held in the 6.5%–7% range, with excess supply persisting in the economy.

- Two dominant risks — the Middle East conflict (via oil prices) and the ongoing US trade relationship, including the now-annual review of the Canada-US-Mexico Agreement (CUSMA).

- CAD depreciation acknowledged — a widening gap between rising US bond yields and largely unchanged Canadian yields has weighed on the Canadian dollar.

The official statement framed Canada’s economy as “showing signs of improvement,” with growth picking up and inflation projected to ease “gradually from its recent spike.”

Since the April MPR, global prospects have been dented by higher oil prices tied to the Middle East conflict, though the Bank noted that AI-related investment is helping offset some of that drag in a growing number of economies.

Link to official Bank of Canada Monetary Policy Statement (July 2026)

Policymakers also pointed to a choppy past year of GDP data as Canada adjusted to new tariffs, elevated uncertainty, and slower population growth, with the unemployment rate at 6.5% in June.

The Governing Council concluded that the current policy rate remains appropriate to support the recovery and bring inflation back to target, while reiterating it is “prepared to adjust monetary policy as needed” given how high uncertainty remains.

Meanwhile, the July Monetary Policy Report (MPR) detailed that inflation excluding gasoline and core inflation measures have stayed near 2%, suggesting that spillover from the energy shock into broader prices has so far been contained.

The Bank projects growth averaging just above 1% in the first half of 2026 and around 1.5% in the second half, before settling at 1.8% in both 2027 and 2028 as excess capacity is gradually absorbed.

Link to BOC Monetary Policy Report (July 2026)

Furthermore, the MPR projects inflation easing to about 2.5% in the second half of 2026, then reaching the 2% target by early 2027. The Bank was explicit that this projection is “highly dependent on developments in the Middle East,” with upside risk if currency depreciation or cost pressures pass through more persistently, and downside risk if global financial conditions tighten or the export recovery underwhelms.

During the press conference, Governor Macklem distilled the Bank’s message into three points: growth has resumed after a year of stalling; inflation is poised to ease gradually provided global oil prices continue to retreat; and uncertainty remains elevated, with the Middle East conflict having “re-escalated in recent days” alongside ongoing US trade discussions.

Link to BOC Press Conference (July 2026)

On inflation, Macklem flagged that the near-term forecast assumes oil prices settle between US$70 and US$75 per barrel but cautioned that “since finalizing our forecast on Friday, the futures curve for oil prices has moved higher,” a notable real-time caveat.

He also pointed out that the recent depreciation of the Canadian dollar cuts both ways: making exports more competitive while raising the cost of imports.

When asked to weigh the risks, Macklem identified the Middle East conflict and the US trade relationship as the two dominant external threats, alongside a domestic risk that inflation could get “stuck” above 2% if cost pass-through proves larger than expected or the economy recovers faster than forecast.

Promoted: Can Your Strategy Handle a Fast Loonie Repricing?

The Bank of Canada policy statement can send the Loonie moving in seconds. FTMO gives traders access to free trials, no time limits, and up to $200K in Demo Capital to test whether their risk management holds up when markets get volatile.

Start a free trial with FTMO!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

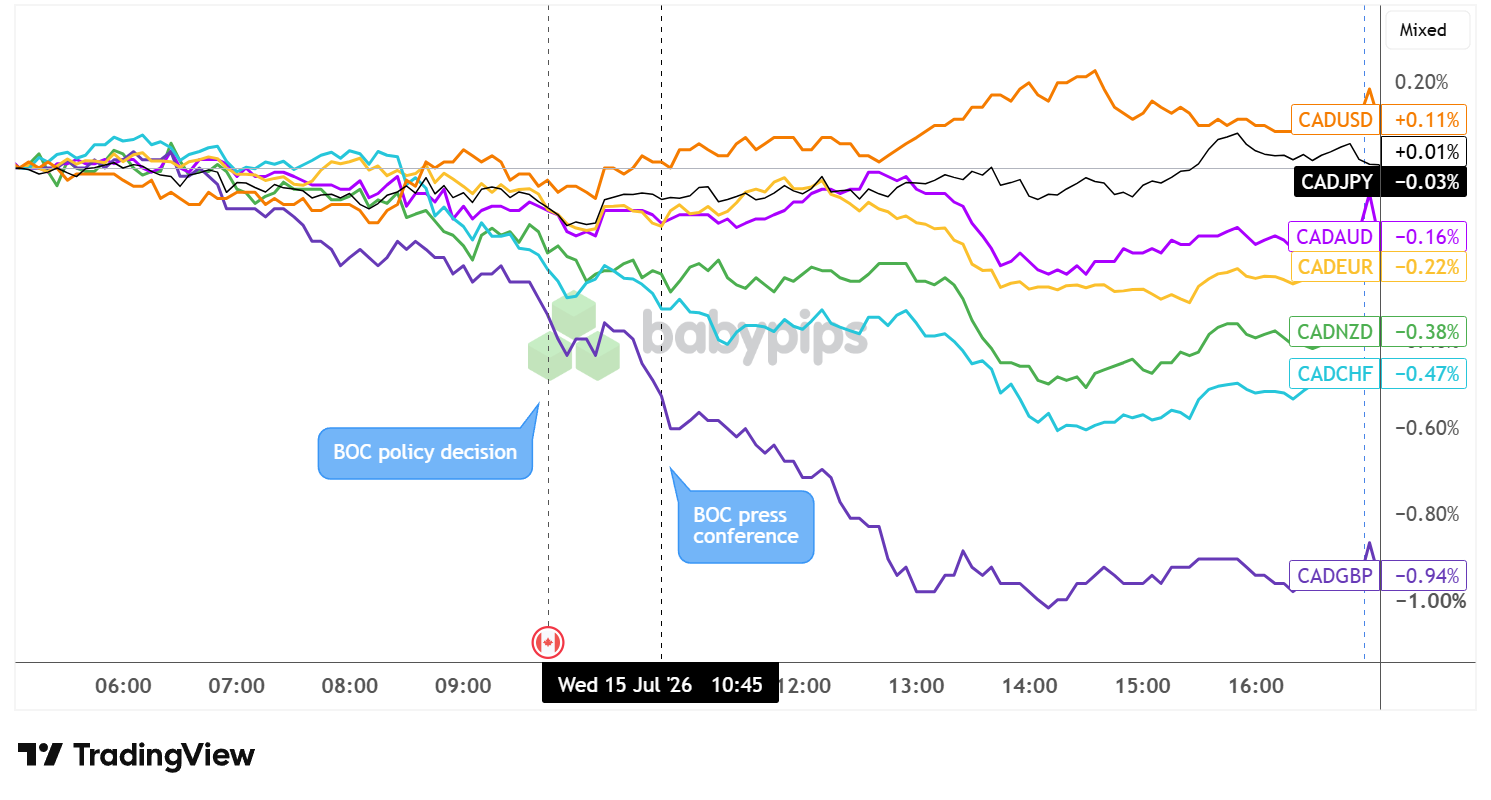

Market Reactions

Canadian Dollar vs. Major Currencies: 5-min

Overlay of CAD vs. Major Currencies 5-minute Forex Chart Faster with TradingView

The Canadian dollar’s response to Wednesday’s announcements was mixed rather than one-directional.

In the hours leading into the 9:45 a.m. ET policy decision, CAD drifted broadly lower against most major currencies, with the steepest declines showing up against the British pound and Swiss franc.That slide continued through the official statement and release of the Monetary Policy Report, including the subsequent press conference. CAD continued to fall sharply against GBP in the immediate aftermath, likely reflecting how markets weighed the Bank’s cautious tone on uncertainty against a relatively steady policy stance.

By the end of the session, the pound had extended its gains against the Loonie to roughly 0.94%, with the Swiss franc up about 0.47% and the New Zealand dollar up around 0.38%. The euro and Australian dollar posted smaller gains against CAD, up roughly 0.22% and 0.16% respectively.

Notably, CAD’s performance against the US dollar diverged from this broader pattern. After tracking lower alongside the other crosses through the morning, CAD/USD staged a steady recovery through the afternoon session, suggesting that the afternoon move was driven more by broad dollar softness than by outright Canadian dollar strength.