The forex trading week has come and gone, so it’s time to take a look at how the major currencies performed and what drove price action.

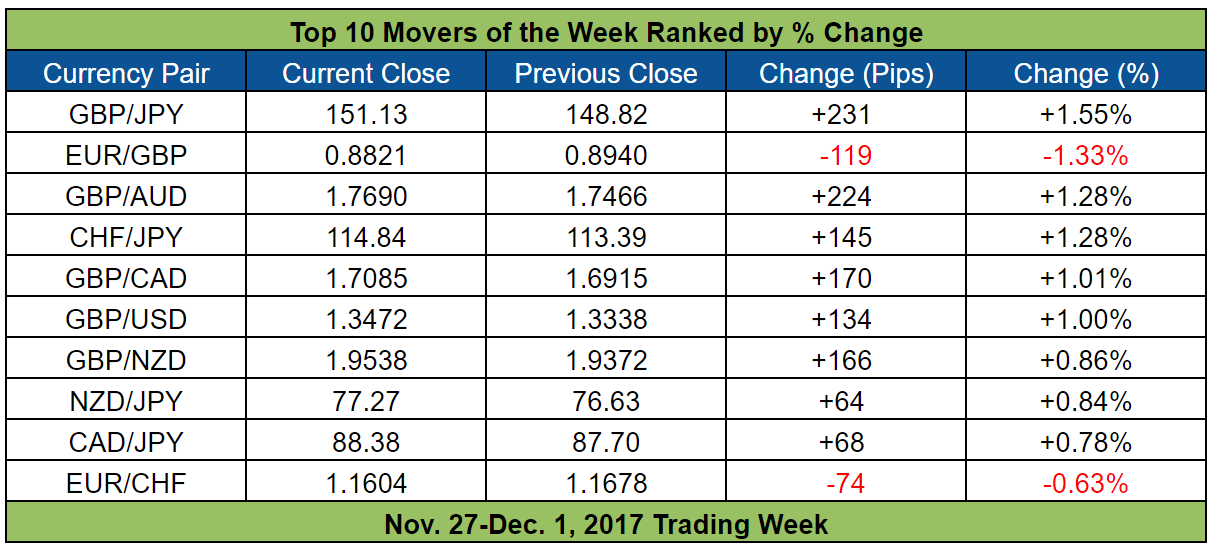

A quick glance at the table of top 10 movers and you easily conclude that pound domination was the main theme this week.

So, what drove the pound higher this week? And what about the other currencies, what drove their price action? Time to find out!

But before that, here’s this week’s scoreboard.

And if you only want to find out what happened to a specific currency, then you can just skip to that currency by clicking on it below.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The U.S. Dollar

Overlay of USD Pairs: 1-Hour Forex Chart

The Greenback was mixed for the week and price action was also pretty messy. However, if we simply remove GBP/USD’s price action, then we get this:

Overlay of USD Pairs: 1-Hour Forex Chart

Yeah, it’s still a bit messy and, as marked above, price action did diverge a bit on Wednesday and Thursday, which implies that the Greenback was vulnerable to opposing currency price action.

Even so, it now a bit clearer that the Greenback’s price action had a certain uniformity to it, so price action on the Greenback wasn’t completely dominated by its forex rivals.

With that said, the Greenback had a mixed and messy start but began to tilt to the upside by Tuesday’s Asian session. There were no apparent catalysts, but market analysts cited incoming Fed Chair Powell’s confirmation hearing speech, which was released late on Tuesday, as well as optimism with regard to the tax reform bill, as the main reasons for the Greenback’s rise.

The Greenback also got a bullish injection after word got around that the U.S. Senate Budget Committee voted to advance the Republican tax reform bill for voting in the U.S. Senate.

Price action on the Greenback then became a bit more mixed before getting another bullish injection when the second estimate for U.S. Q3 GDP growth was revealed to have been upgraded from 3.0% quarter-on-quarter annualized to 3.3% (+3.1% in Q2), which is the strongest quarterly growth in 10 quarters and marks the second quarter of ever stronger growth.

Sadly, the Greenback’s rise got capped a couple of hours later when outgoing Fed Head Yellen gave her speech. There wasn’t really anything surprising in Yellen’s speech since she basically reiterated the message from last week’s FOMC statement.

However, Yellen didn’t give any hints with regard to a highly-anticipated December rate hike. And that may have disappointed some rate hike junkies since the Greenback slid lower but there was no follow-through selling and the Greenback’s price action became more mixed before tilting to the upside again later.

Thursday was another volatile day for the Greenback since it got kicked lower across the board, apparently as a reaction to reports that cited unnamed officials as saying that Secretary of State Rex Tillerson will supposedly be fired and replaced with CIA Director Mike Pompeo, a rumor which Trump later denied.

Fortunately for Greenback bulls, Republican Senator John McCain came to save the day when he said that he’d back the tax reform bill in the U.S. Senate. Despite McCain’s support, however, the Senate adjourned without coming to a vote on Thursday, so the Greenback’s rally stalled.

The Greenback then had another bout of mixed and messy price action after that before getting gutted during Friday’s late U.S. session, apparently because of an ABC News report that claimed that ex-adviser Flynn will supposedly testify that Trump directed Flynn to contact the Russians while Trump was still a candidate.

This put the Trump-Russia collusion conspiracy theory front and center once more and triggered the usual speculation about Trump getting impeached and delays to the tax reform, etc.

By the way, the U.S. Senate has already approved their version of the tax reform bill. You can check out the changes to their version in this Reuters report, if you’re interested.

The House and the Senate still need to reconcile their versions, though, and they could start doing that as early as next week, so this drama is not over yet.

Also worth mentioning is that the ABC News report was revealed to have been what many decried as fake news. And so ABC News issued the correction below, which, if true, significantly changes the implications and blurs the legality of Trump’s actions. However, the correction came hours later and the markets were already closed by then. Even so, it would be interesting to see if the correction below and the approval of the Senate’s version of the tax reform bill will cause gaps to form on Monday.

CORRECTION of ABC News Special Report: Flynn prepared to testify that President-elect Donald Trump directed him to make contact with the Russians *during the transition* — initially as a way to work together to fight ISIS in Syria, confidant now says. https://t.co/ewrkVZTu2K pic.twitter.com/URLiHf3uSm

— ABC News (@ABC) December 2, 2017

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Euro

Overlay of EUR Pairs: 1-Hour Forex Chart

The overlay of EUR pairs above excludes EUR/GBP since that pair was an outlier, which means that GBP drove price action on EUR/GBP. Also worth pointing out is the dashed horizontal line since that marks the previous week’s close.

Having said that, the euro started the trading week mixed but began to weaken against its peers (not so much against CAD) when Social Democratic Party of Germany (SPD) leader Martin Schulz said at the start of Monday’s U.S. session that “No options are off the table” and that the SPD is even ready to walk away from talks to form a coalition government with Angela Merkel.

This seems to contradict Schulz’s conciliatory statement from last week that “We [the SPD] won’t be obstructionist for the sake of being obstructionist” and that the SPD would even cooperate with Merkel in a minority government, which is likely why the euro reacted negatively to Schulz’s Monday comments.

The euro finally found support during Tuesday’s late U.S. session and even began to tilt higher on some pairs. No clear reason why, though.

It later became clear at the start of Wednesday’s U.S. session that the euro was getting bid up, likely because of speculation that the Euro Zone will print stronger inflation numbers on Thursday, given that demand for the euro began to noticeably pick up after Germany printed stronger inflation readings.

And when Thursday rolled around, the Euro Zone’s November inflation report revealed that headline HICP for the Euro Zone as a whole only increased by 1.5% year-on-year, missing the consensus for a 1.6% rise.

But as I pointed out in Thursday’s London session recap, and before the EUR rally kicked it into high gear, the 1.5% increase in November is still faster compared to the previous month’s 1.4% increase.

More importantly, the 1.5% reading is still in line with the ECB’s forecast that headline inflation will rise by 1.5% year-on-year in 2017, as laid out in the ECB’s September macroeconomic projections.

Moreover, the ECB’s preferred measures for core inflation are still evolving within expectations since, HICP less energy maintained the previous month’s annual pace of +1.2%, which is in-line with the ECB’s +1.2% forecast for 2017. Meanwhile, HICP less energy and unprocessed food, came in at +1.1%, which is also in-line with the ECB’s +1.1% forecast for 2017.

Also, the Euro Zone’s October jobs report was released together with the inflation report and that showed that the jobless rate for the Euro Zone as a whole fell from 8.9% to 8.8% in October, which is the best reading since January 2009 and is soundly beating the ECB’s forecast that the jobless rate would come in at 9.1% by the end of the year.

Given the above, the euro initially reacted by spiking lower when headline HICP failed to meet the market’s expectations. However, dip demand was present because HICP is still evolving within the ECB’s expectations and the labor market is tightening at a faster rate to boot.

It’s worth pointing out that, as can be seen in the overlay of EUR pairs above, the euro became a net winner on Thursday after being a net loser for most of the week.

Unfortunately for the euro, the euro’s rally sputtered to a stop and then began to reverse course on Friday. And it’s this reversal of fortune on Friday that spelled doom for the euro.

As to what caused the euro to dip, there’s no clear reason for that.

Schulz did repeat his Monday message by saying on Friday that “Regarding the formation of a new government, there was broad support [from SPD members] for not ruling any option out.”

And that may have helped to send the euro lower. However, the euro’s broad-based slide started during the late Asian session, even though there were no catalysts, which is why I opined in Friday’s London session recap that the euro’s slide was possibly due to profit-taking by bulls who rode the euro rally, especially the upswing on Thursday.

Well, whatever the case may be, the fact remains that the euro was a net winner on Thursday but the broad-based slide on Friday did a number on the euro. And so the euro ended up being a net loser this past week.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Pound Sterling

Overlay of GBP Pairs: 1-Hour Forex Chart

The pound was the one currency to rule them all this past week. And as marked on the chart above, the pound’s bullish onslaught started on Tuesday, thanks to Brexit-related rumors.

To be more specific, The Telegraph and The Financial Times independently released very similar reports that cited unnamed sources familiar with the talks as claiming that the U.K. has capitulated to the E.U.’s demands and has agreed to pony up the cash for the Brexit bill.

The Telegraph report claimed that the U.K.’s bill “will be between €45bn and €55bn” while The Financial Times report claimed that “the UK would assume EU liabilities worth up to €100bn although net payments, discharged over many decades, could fall to less than half that amount,” so roughly similar figures and the two reports seemed to be corroborating each other.

These news/rumors caused the pound to surge higher since it greatly increases the odds that Brexit talks could move on to Phase 2, which refers to the post-Brexit trade deal.

After all, the E.U. has three main demands left: (1) citizens’ rights, (2) the Brexit bill, and (3) a resolution to the Irish border issue. Pretty much everyone thinks that there’s no problem with citizens’ rights, and with the Brexit bill now rumored to have been resolved, that leaves the Irish border issue as the sole obstacle left.

Going back to the pound’s price action, the pound’s rumor-fueled rally was unstoppable and the pound just steamrolled all its forex rivals on Wednesday and Thursday.

The pound’s rally finally began to run out of steam on Friday. And not even the better-than-expected manufacturing PMI reading (58.2, a 51-month high vs. steady at 56.5 expected) was able to reignite demand for the pound.

And as noted in Friday’s London session recap, there were no negative catalysts for the pound at the time, so I opined that Friday’s dip was likely due to profit-taking by pound bulls ahead of British PM Theresa May’s meeting with European Commission President Jean-Claude Juncker and E.U. top Brexit negotiator Michel Barnier this coming Monday. Some market analysts also had the same thoughts.

By the way, Reuters’ Factbox has listed down the key Brexit-related events to watch out for, including the ones scheduled for next week. So click on that link if you want to know more and/or plan ahead.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Swiss Franc

Overlay of CHF Pairs: 1-Hour Forex Chart

The euro was one of the worst-performing currencies of the week while the Swissy was the second-best-performing currency of the week.

The euro and the Swissy were therefore clearly on different ends of the spectrum. So does that mean that the euro and the Swissy have finally parted ways?

Hah! Nope! However, as you can see in the sample pairs below, market players likely ran while crying and screaming to the safe-haven Swissy when an ABC News report (that was already discussed when we talked about USD) triggered mass hysteria and intensified risk aversion, since the Swissy was able to significantly outpace the euro then.

ABC has already issued a correction to that report, which significantly changes the implications, but markets were already closed when the correction was issued, so it’s interesting to see if the Swissy would give back its gains (or not) come Monday.

USD/CHF (inverted, red) vs. EUR/USD (black): 1-Hour Forex Chart

NZD/CHF (inverted, red) vs. EUR/NZD (black): 1-Hour Forex Chart

GBP/CHF (inverted, red) vs. EUR/GBP (black): 1-Hour Forex Chart

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Japanese Yen

Overlay of Inverted JPY Pairs & US10Y Bond Yield (Black Line): 1-Hour Forex Chart

As always, yen pairs (other than NZD/JPY) were taking directional hints from bond yields. And since bond yields closed higher this past week, the yen ended up weaker, so much so that the yen was the worst-performing currency of the week.

The yen initially had the upper hand (except on NZD/JPY) when bond yields dipped on Monday and Tuesday because of safe-haven demand for bonds due to news that North Korea may be getting ready for another missile test, market analysts say.

However, the yen’s fortunes started to sour during Tuesday’s U.S. session when bond yields started to rise after the U.S. Senate Budget Committee voted to advance the Republican tax reform bill for a full vote in the U.S. Senate.

It was then downhill for the yen from there since bond yields climbed even higher on Wednesday, thanks to the upgraded reading for U.S. GDP growth.

Thursday was another painful day for the yen since risk appetite dominated, causing bond yields to spurt higher. The rise in bond yields also gained momentum during the U.S. session, thanks to McCain’s endorsement of the tax reform bill, market analysts say.

The yen’s retreat finally slowed during Friday’s Asian and London session, thanks to renewed demand for U.S. bonds, according to market analysts, amid worries that the tax reform bill may get delayed because of reports that Senate Republicans were squabbling with the Democrats and amongst each other.

The yen later got a chance to take back some lost ground during the U.S. session, apparently because bond yields plunged hard after an ABC News report claimed that ex-adviser Flynn will supposedly testify that Trump directed Flynn to contact the Russians during the election campaign.

Even so, the damage to the yen was already done and so the yen ended up at the bottom of the forex heap.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Canadian Dollar

Overlay of CAD Pairs & Crude Oil (Black Line): 1-Hour Forex Chart

The ranking table for CAD pairs shows that the Loonie was a net winner for the week while also showing that the Loonie’s gains were rather small.

But as you can see on the overlay of CAD pairs, the reason why Loonie’s gains were so small was that the Loonie was broadly on the defensive from Monday to Thursday before catching a bid on Friday and then violently surging higher during Friday’s U.S. session.

Interestingly enough, the Loonie appears to be taking directional cues from oil again after decoupling in the past few weeks. And the likely reason why the Loonie was tracking oil prices again was the news that TransCanada’s Keystone pipeline restarted operations.

Unfortunately for the Loonie, the same news that the Keystone pipeline is operational again was cited as one of the two major reason why oil prices tanked this week.

The other reason for oil’s weakness was uncertainty ahead of the OPEC meeting. Although we now know that OPEC decided to extend its oil cut deal again until the end of 2018 late on Thursday, which later caused oil prices to recover.

And since oil prices began to recover, so did the Loonie. However, the Loonie later surged higher at the start of the U.S. session, thanks to Canada’s impressive jobs report (+79.5K jobs vs. +10.0K expected, +35.3K previous) and Canada’s better-than-expected GDP readings (1.7% q/q annualized vs. 1.6% expected, 4.5% previous).

By the way, another BOC statement is coming our way, so make sure to keep an eye on the Loonie next week.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The Australian Dollar

Overlay of AUD Pairs & Gold (Black Line): 1-Hour Forex Chart

The Aussie was a net loser this week. But looking at the overlay of AUD pairs above, we can see that the Aussie’s price action was quite messy overall, with lots of divergence. And since weekly % change across Aussie pairs (other than GBP/AUD) were relatively small, we can safely conclude that the Aussie was vulnerable to opposing currency price action.

It’s still worth noting that the Aussie tried to track gold prices. However, risk sentiment apparently got in the way.

Gold, for example, was tilting slightly lower on Tuesday. However, risk-taking was the dominant sentiment on Tuesday, so the Aussie was mixed but was a net winner for the day.

Wednesday and Thursday, were also days when risk sentiment interfered with the Aussie’s attempt to track gold prices since gold was slumping but risk-taking was the dominant sentiment on Wednesday and the prevalent sentiment on Thursday.

Basically, conflicting directional cues, which is probably why the Aussie’s price action was quite messy and choppy back then.

Anyhow, we’ve got a lot of top-tier events lined up for the Aussie next week, including another RBA statement and GDP report. Hopefully, we’ll get more uniform price action from the Aussie next week.

- The U.S. Dollar (USD)

- The Euro (EUR)

- The Pound Sterling (GBP)

- The Swiss Franc (CHF)

- The Japanese Yen (JPY)

- The Canadian Dollar (CAD)

- The Australian Dollar (AUD)

- The New Zealand Dollar (NZD)

The New Zealand Dollar

Overlay of NZD Pairs: 1-Hour Forex Chart

The Kiwi had a mixed performance this week. However, that doesn’t mean that the Kiwi was vulnerable to opposing currencies since price action on Kiwi pairs were actually uniform, as you can see in the overlay of NZD pairs.

The Kiwi started the new trading week by stumbling a bit because of risk aversion during Monday’s Asian session. Appetite for risk made a comeback during the course of Monday’s morning London session, though, so the Kiwi recovered from its earlier losses and then some.

Risk-taking persisted on Tuesday. However, the Kiwi started to encounter sellers during Tuesday’s U.S. session, possibly because of profit-taking by Kiwi bulls ahead of the RBNZ’s Financial Stability Report.

And when the report was finally released, the Kiwi tried to jump higher likely because the RBNZ gave the following conclusions:

“New Zealand’s financial system remains sound. The banking system maintains adequate buffers over minimum capital requirements. Recent stress tests suggest that banks can withstand a severe economic downturn, although results are sensitive to a range of assumptions.”

Kiwi bears were quick to return, though, likely because the RBNZ also noted that there was “a tightening in lending standards, which has contributed to a slowing in credit growth.”

Moreover, the RBNZ warned that while the risk of a housing bubble in no longer great, “house prices remain elevated relative to incomes and rents.” And to make matters worse, “the Government has announced a number of policies that are likely to reduce housing demand and increase housing supply.”

The RBNZ also pointed out that the dairy sector, the main driver of New Zealand’s export-oriented economy, remain highly indebted. In fact, the recent slide in dairy prices “has led to an increase in debt in the sector.”

Finally, the RBNZ also noted that:

“New Zealand’s long-term market interest rates will likely move higher as monetary policy stimulus is removed in major advanced economies. An increase in global interest rates and term premiums could also reduce demand for New Zealand assets as portfolios are rebalanced ”

The RBNZ didn’t really talk about how the above factors will impact the RBNZ’s monetary policy.

However, if we read between the lines, then the implication of slower credit growth and higher indebtedness in the dairy sector would be that the RBNZ will be less likely to hike because hiking would mean that credit conditions would tighten even further, slowing credit growth even more while also squeezing the dairy sector, which increases the risk of default in that sector.

And with regard to that bit about tighter monetary policy in foreign advanced economies, the RBNZ is basically saying that higher interest rates elsewhere and steady rates in New Zealand would put interest rate differentials into play. And that would be at the expense of New Zealand assets (and the Kiwi) since investors would choose to go elsewhere.

So, yeah, a dovish message overall, which is likely why the Kiwi continued to slide lower.

Fortunately for the Kiwi, appetite for risk was still the name of the game on Wednesday, especially in Europe (Asia was more mixed), so the Kiwi was able to lick its wounds.

Unfortunately for the Kiwi, risk aversion returned during Wednesday’s U.S. session, so the Kiwi got dragged broadly lower.

And then to add salt to injury, ANZ’s business outlook survey showed that New Zealand’s business confidence index drastically plummeted from -10.1 to a mind-numbing -39.3, which is an eight-year low.

Quite naturally, the Kiwi fell sharply as well. And there was apparently follow-through selling since the Kiwi closed out as a net loser on Thursday despite the prevalence of risk-taking. Although it’s worth noting that the Kiwi did recover temporarily during Thursday’s morning London session.

And when Friday rolled around, the Kiwi was able to stage a broad-based recovery and was a winner for the day (except against the resurgent Loonie), even though risk aversion returned in force.

I noted in Friday’s London session recap that there were no apparent catalysts for the Kiwi’s rally, but since bond yields were down hard at the time, the market may have viewed the higher-yielding Kiwi as a more attractive alternative.

In hindsight, however, the more likely reason for the the Kiwi’s Friday recovery was short-covering by Kiwi bears to lock in some delicious profits from the Kiwi’s broad-based slide this past week.

Anyhow, the three-way intraweek action on the Kiwi is the reason why the Kiwi had a mixed performance this week, despite having roughly uniform price action.