Greetings, forex friends! The U.S. will be releasing its CPI and retail sales reports this Friday (January 12, 1:30 pm GMT). And if you’re planning to trade these top-tier reports and you need a quick recap, as well as a preview on what’s expected, then today’s edition of my Event Preview is just for you!

1. U.S. CPI Report (December)

What happened last time?

- Headline CPI (m/m): +0.4% as expected vs. +0.1% previous

- Core CPI (m/m): +0.1% expected vs. 0.2% expected, same as previous

- Headline CPI (y/y): +2.2% as expected vs. +2.0% previous

- Core CPI (y/y): +1.7% vs. steady at +1.8% expected

The headline CPI readings for November came in at 0.4% month-on-month and 2.2% year-on-year, which are both within expectations and faster readings than their respective previous readings of 0.1% month-on-month and 2.0% year-on-year respectively.

However, the core readings were unable to meet the market’s expectations since core CPI only rose by 0.1% month-on-month (+0.2% expected) and 1.7% year-on-year (+1.8% expected).

Given these misses, market analysts concluded that the November CPI report was leaning more to the negative side since the misses were interpreted to mean that the Fed will be less likely to communicate a faster pace of hiking in 2018.

And as a result, the Greenback encountered selling pressure across the board.

Overlay of USD Pairs: 15-Minute Forex Chart

What’s expected this time?

- Headline CPI (m/m): +0.1% expected vs. +0.4% previous

- Core CPI (m/m): +0.2% expected vs. 0.1% previous

- Headline CPI (y/y): +2.1% as expected vs. +2.2% previous

- Core CPI (y/y): steady at +1.7% expected

For the Friday’s December CPI report, economist are of the consensus that headline CPI rose by 0.1% month-on-month (+0.4% previous) and 2.1% year-on-year (2.2% previous). Economists are therefore expecting December headline CPI to print weaker readings compared to November’s numbers.

As for the core reading, most economist forecast that core CPI rose by 0.2% month-on-month, which is a tick faster than November’s 0.1% rise, but the annual reading is expected to maintain the +1.7% pace.

And since headline CPI is expected to weaken while the core readings are expected to either accelerate or hold steady, then that means that there’s an implied consensus that food and energy prices weakened in December since those two components are excluded from the core reading.

Okay, let’s take a loot at the leading indicators:

- The price index of ISM’s manufacturing PMI report jumped from 65.5 to 69.0 index points. This means that manufacturing companies are paying higher input costs. And according to ISM, “The only industry reporting price decreases in December compared to November is Textile Mills.

- Markit’s manufacturing PMI report agrees with ISM’s findings since Markit found that the increase in input costs “was the second-fastest since December 2013.” More importantly, companies are passing on their higher input costs since “factory gate charges rose solidly.”

- The price index of ISM’s non-manufacturing PMI report only improved very slightly from 60.7 to 60.8 index points. And according to ISM, “Twenty-one percent of respondents reported higher prices, 72 percent indicated no change in prices paid and 7 percent of respondents reported lower prices.”

- Markit’s services PMI report is more pessimistic since it found that “Inflationary pressures eased in December, with both input price and charge inflation softening.”

Overall, the leading indicators are presenting a somewhat mixed picture since the manufacturing sector reported higher input costs and passed on those costs while the services sector either only saw a small increase in input prices or saw a decline in both input and charged price. And since the cost of services account for around 60.2% of headline CPI, the leading indicators therefore do seem to support the consensus that headline CPI slowed in December, or at least maintained the pace.

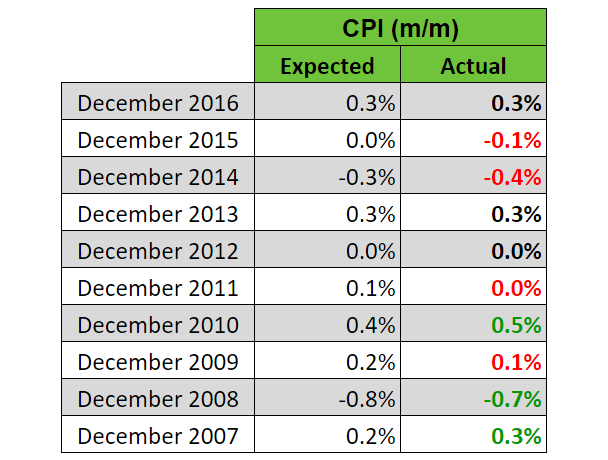

Let’s move on to historical tendencies. Do they help to clarify things? Well, not really, since market analysts have a mixed record when it comes to their guesstimates for the headline reading.

When it comes to the core reading, however, market analysts either get it right or overshoot their guesstimates. In fact, there have been no better-than-expected December core CPI readings in the last 10 years, as you can see below.

To sum it all up, the leading indicators are presenting a mixed picture, but they do seem to support the consensus for a weaker December headline reading, or at least a reading that matches November’s readings.

As for historical tendencies, there are none for the headline reading. The core reading is another story since market analysts either get it right or are too optimistic with their guesstimates, since there are no upside surprises for the December CPI reading in the last 10 years.

As such, it’s a coin toss for the headline reading but probability does seem skewed more towards the downside for the core reading.

However, just keep in mind that we’re playing with probabilities here, so the actual reading could still print an upside surprise.

2. U.S. Retail Sales Report (December)

What happened last time?

- November headline retail sales (m/m): 0.8% vs. 0.3% expected

- October headline retail sales (m/m): revised higher from +0.2% to +0.5%

- November core retail sales (m/m): +1.0% vs. +0.6% expected

- October core retail sales (m/m): upgraded from +0.1% to +0.4%

The total value of retail sales in the U.S. rose by 0.8% month-on-month in November, beating expectations for a 0.3% rise. Even better, October’s reading was upgraded from +0.2% to +0.5%.

Better still, the core retail reading came in at 1.0% month-on-month, which is also stronger than the expected 0.6% increase. Moreover, October’s core reading was also revised higher from +0.1% to +0.5%.

Overall, the November retail sales report was very positive, which is why the Greenback’s knee-jerk reaction was to jump higher.

However, there was no follow-through buying, very likely because the U.S. dollar was reeling from the somewhat cautious FOMC statement at the time.

Overlay of USD Pairs: 15-Minute Forex Chart

What’s expected this time?

- Headline retail sales (m/m): +0.4% vs. +0.8% previous

- Core retail sales (m/m): +0.4% vs. +1.0% previous

The general consensus among economists is that the headline value of retail sales rose by 0.4% in December, which is a softer rise compared to the +0.8% printed in November.

The core reading is also expected to weaken since it’s expected to come in at +0.4% (+1.0% previous).

Since the core reading is forecasted to weaken at a stronger pace compared to the headline reading, there’s therefore also an implied consensus that non-vehicles sales weakened in December.

Okay, let’s now check out the leading/related indicators:

- Total vehicle sales in December increased by an annualized rate of 17.9 million, which is slightly more than the previous reading of 17.5 million, which supports the implied consensus that non-vehicle sales would be a drag on December retail sales.

- ISM’s non-manufacturing PMI report for December noted that the retail trade industry saw an increase in both business activity and new sales growth. However, retail trade was also one of the industries that reported “a feeling that their inventories were too high in December,” which may be a hint that consumer spending wasn’t strong.

- Meanwhile, the Conference Board consumer confidence index dropped from 128.6 to 122.1 in December.

- Likewise, The University of Michigan’s consumer confidence index weakened from 98.5 to 95.9.

- The December NFP report reveals that the trade trade industry trimmed 20.3K jobs in December after adding 26.4K jobs back in November, which implies downsizing and a possible weakness in retail trade.

Overall, the available leading/related indicators do seem to support the consensus that headline and core retail sales reading will print weaker numbers in December.

In addition, the available leading/related indicators also support the implied consensus that non-vehicle sales would be the cause of the weaker growth rate in retail trade.

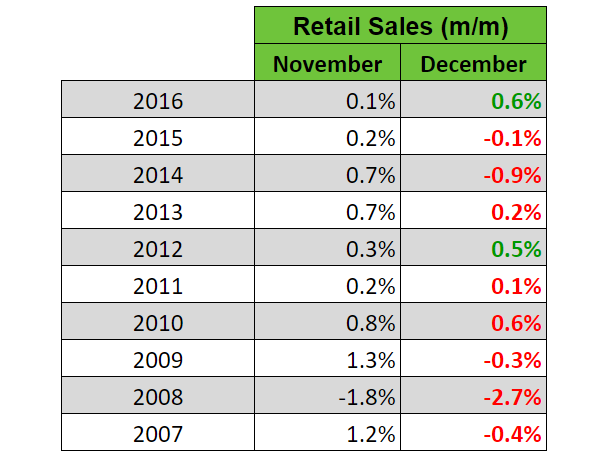

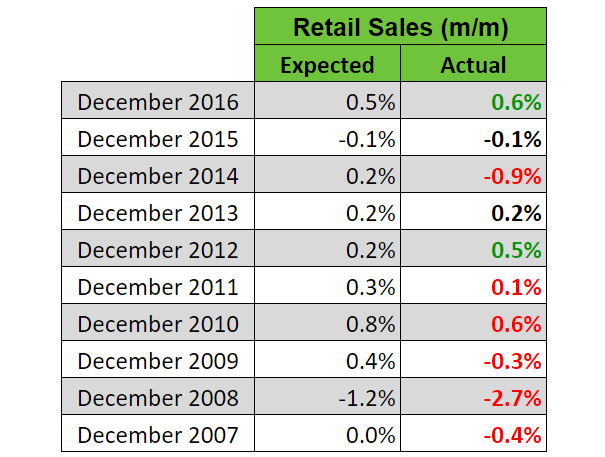

Moving on to historical tendencies, the consensus that headline and core December retail sales growth is slower compared to November is supported by historical data.

Even so, economists still tend to be too optimistic with their guesstimates for the headline reading, resulting in more downside surprises.

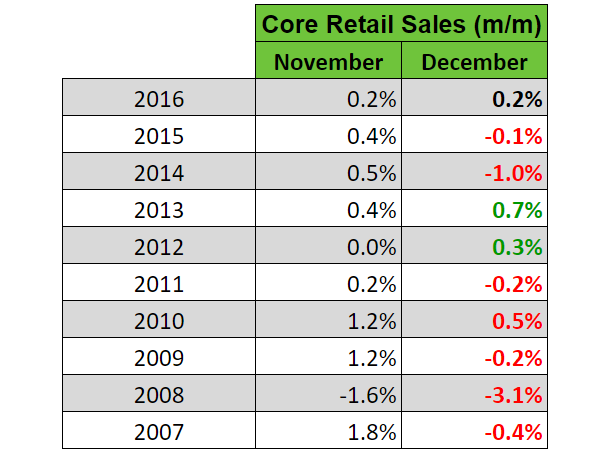

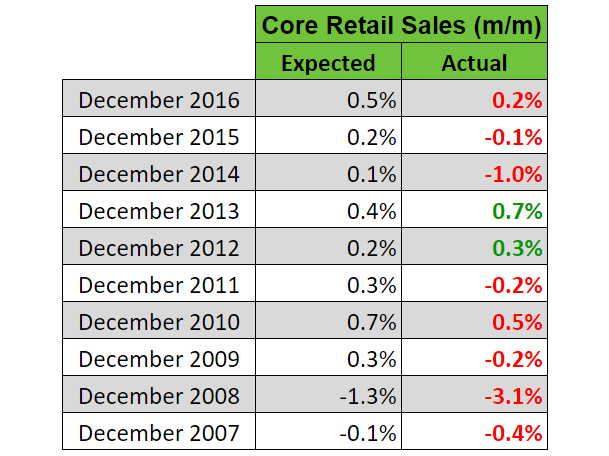

As for the core retail sales reading, economists have a strong historical tendency to overshoot their guesstimates since there were only two upside surprises in the past 10 years.

In summary, the available leading/related indicators are pointing to weaker consumer spending in December. And this is supported by historical data.

Moreover, economists still tend to be too optimistic with their guesstimates for the headline reading since there are more downside surprises. And the same cane be said for the core reading. Probability therefore seems skewed more to the downside for both.

Again, however, just keep in mind that we’re playing with probabilities here, so there are no guarantees.

Final Thoughts

Keep in mind that the CPI and retail sales reports will be released simultaneously.

If both reports miss expectations, then that usually triggers a quick Greenback sell-off while a quick rally is usually triggered if both reports end up being better-than-expected.

But what if the reports are mixed? Which top-tier economic report do traders usually put more weight on?

Well, traders usually have their sights on the CPI report because it’s more directly link to rate hike expectations. And usually (but not always), the spotlight falls on the headline reading.

And if the headline reading is within expectations, then that’s usually when traders pay attention to the core reading. The Greenback’s reaction to the November CPI report is a classic example of this.

And as always, just remember that if news trading ain’t your thing or if high volatility makes you jittery, then you always have the choice of sitting it out on the sidelines.