The pound has recently been doing rather well against its forex rivals, except against the Kiwi and the U.S. dollar.

Demand for the pound is usually attributed to positive merger and acquisition (M&A) stories such as the one between Anheuser-Busch InBev and Sabmiller, the two largest brewing companies on the planet in terms of revenues.

Another major factor keeping the pound afloat is the consensus among forex traders and economists that the Bank of England (BOE) is still set to hike rates by Q1 or Q2 of next year. So, do the underlying fundamentals still support a potential rate hike?

Growth

The final reading for Q2 2015 GDP growth was unrevised at 0.7%, which is a welcome improvement over the previous quarter’s 0.4% expansion.

However, the year-on-year reading wasn’t that upbeat since it only registered a 2.4% increase, which is slower than the previous quarter’s 2.7% increase and also happens to be the slowest growth rate in seven quarters.

Looking at the details of the report, the slower annualized growth was due primarily to the 3.4% increase in gross fixed capital formation (net new investments in fixed assets such as roads, hospitals, bridges, etc.), which is much lower than Q2 2014’s 4.9%.

On a quarterly basis, the increase was due mainly to the 1.4% contribution from the positive trade balance, thanks to a 1.9% increase in exports and a 2.7% contraction in imports.Other components had minimal contributions, but household spending continues to be the backbone of the British economy with its 0.5% positive contribution to GDP growth.

The main drag, however, came from the 7.1% drop in gross fixed capital formation, which subtracted 1.3% from total GDP growth.

Employment

As I mentioned in an earlier write-up, forex traders reacted positively to the most recent employment readings since the current jobless rate of 5.4% (5.5% previous) is the lowest level in seven years.

Also, the employment rate climbed to 73.6%, which is the highest ever on record. Furthermore, the average earnings index, the main gauge for wage growth in the U.K., grew by 3.0% (2.9% previous) while the labor force participation rate remained steady at 77.9%.

The only disappointment was the claimant count change since it saw a 4.6K increase in the number of people claiming unemployment that could potentially come around and bite the British economy in the buns, but overall, the U.K. had a pretty solid jobs report.

Consumer Spending & Sentiment

Most analysts and forex traders, myself included, were blown away when the U.K. printed a monstrously bigger-than-expected increase in retail sales volume (1.9% actual v.s. 0.4% expected, -0.4% previous) for the month of September since we apparently underestimated the huge increase in food and beer sales due to the Rugby World Cup.

The knee-jerk reaction to the surprise reading was to send the pound higher, but forex traders later began unwinding some of their positions when they got wind that the surprise increase was due to the Rugby World Cup.The U.K. Office for National Statistics sheepishly mentioning in their report that “Feedback from food stores suggests that some of the growth seen this period can be attributed to promotions centered around the Rugby World Cup.”

This implies that the jump in consumer spending is likely unsustainable.

On an annualized basis, the sudden surge in retail sales also had a significant impact, pushing the reading to a 10-month high of 6.5% (3.5% previous).

Moving on, consumer sentiment is at odds with the surge in consumer spending since the GfK’s consumer confidence index for September dropped by four points to 3.0, with most indices seeing slight decreases.

The “major purchase” index, for example, dropped by three points to 14.0. Interestingly, the “savings” index actually posted a single point increase to 3.0, which implies that Britons are a bit more inclined to save.

Business Sentiment & Conditions

Total industrial output in August advanced by 1.9% on an annualized basis (0.7% previous) and 1.0% on a monthly basis (-0.3% previous) due mainly to the mining and quarrying sector, which soared by 17.7%.

The manufacturing sector, meanwhile, saw a 0.8% decrease in output. And the upcoming readings for manufacturing production probably won’t see an improvement since Markit’s since manufacturing PMI for September dipped to a three-month low (51.3 current, 51.6 previous).

Markit’s services PMI for September also doesn’t look too good since it suddenly dropped from 55.6 to 53.3, which is the weakest reading in two-and-a-half years. At least it’s still above the 50.0 level, so the services sector is still expanding.

Markit’s services PMI for September also doesn’t look too good since it suddenly dropped from 55.6 to 53.3, which is the weakest reading in two-and-a-half years. At least it’s still above the 50.0 level, so the services sector is still expanding.

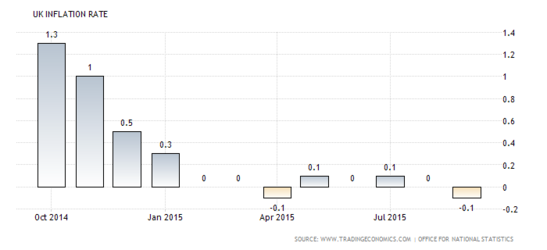

Inflation

I already mentioned it in my latest Global Inflation Update, but both the monthly and yearly readings for headline CPI in September dipped back into negative territory. And as I noted then, the main drag to the year-on-year reading was the “clothing and footwear” component, which dragged headline CPI down by 0.09%.

For the monthly reading, however, lower oil prices are a considerable drag since the 2.9% decline in the “fuels and lubricants” sub-component allowed the “transportation” index to drag the entire CPI reading into the red.

Summary & Conclusion

Aside from further tightening in the labor market, most of the other economic indicators aren’t really that optimistic, particularly CPI. To be fair, though, the BOE did warn in its latest meeting minutes that CPI would “likely remain close to zero before picking up around the turn of the year.”

There was also a sudden surge in retail sales, but it was likely a fluke due to the Rugby World Cup, so we’ll probably see some normalization in the coming months.That’s great and all, but are we set for a rate hike? Well, on the surface, it’s rather difficult to justify a rate hike, but rhetoric from the meeting minutes and from individual speeches have consistently shown that the likely path for rates is up.

Ian McCafferty, in particular, has been voting for a rate hike since he believes that if rates aren’t raised soon, then there’s a good chance that inflation will overshoot the BOE’s 2.00% target, and the solid domestic consumer spending and steady increase in wage growth certainly supports McCafferty’s view.