Hello, forex friends! Oil finally had a major rally after several weeks of declines.

And since the latest inflation numbers for most of the major economies are out, I decided to take a look if oil prices are still weighing in on most of the major economies.

Hmm. Looks like we’re seeing lots of improvements for both the annualized headline and core readings. Time to dig deeper!

Oh, Australia releases its CPI readings on a quarterly rather than a monthly basis, so my commentary from the Global Inflation Roundup from two months ago is still applicable. You can read it here.

Also, do note that Australia will be releasing its Q4 2015 CPI this coming Wednesday (Jan. 27, 12:30 am GMT), so make sure to mark your forex calendars for that.

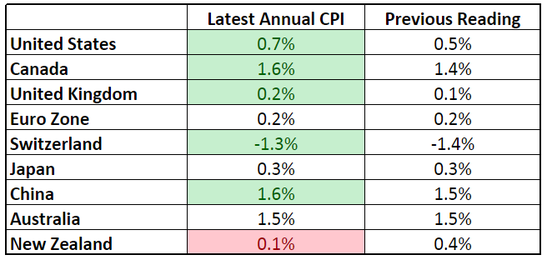

The U.S.

The headline reading for the December period ticked lower to -0.1% month-on-month after flattening out during the previous month. However, the annualized reading actually registered a 0.7% increase after advancing by 0.5% during the previous month.

The recent decline in oil prices took a toll on the monthly headline reading, with the -7.8% drop in fuel oil prices and -3.9% fall gasoline prices being the main drags.

But on an annualized basis, gasoline was far less of a drag (-19.7% vs. -24.1% previous) while fuel oil’s negative contribution was unchanged at -31.4%, which is still pretty horrible.

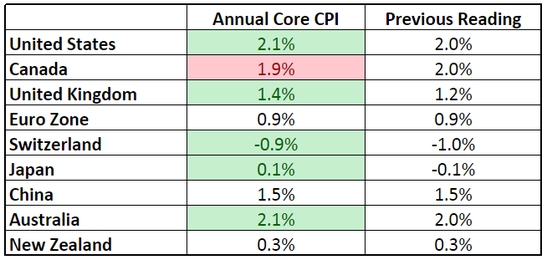

The annualized core reading, meanwhile, saw an uptick to 2.1% from 2.0% previously, which is great since it has been steadily increasing, signifying a healthy underlying trend.

Anyhow, the uptick was apparently due to slower declines for non-energy commodities (-0.4% vs. -0.6%) and apparel (-0.9% vs. -1.5% previous), accompanies by an increase in the price of used cars and trucks (0.4% vs. -0.6% previous).

Canada

Like the U.S., Canada’s headline reading for December printed a deeper 0.5% decline (-0.1% previous), but the annualized reading printed an improvement from 1.4% to 1.6%.

Unlike the U.S., Canada’s annualized core reading is rather worrying since it only registered a 1.9% increase (2.0% previous), which happens to be a 17-month low and also marks the second consecutive month of worsening core readings.

On a monthly basis, the headline reading’s deeper decline was due to negative contributions from 6 of the 8 major components, with the gasoline sub-component being even more of a drag due to the recent oil slump (-4.0% vs -0.3% previous).

But for the headline year-on-year reading, all of the 8 components were in positive territory, although the gasoline sub-component is still a drag, albeit not as horrible when compares to the previous month (-4.8% vs. -10.6% previous).

The U.K.

December headline CPI in the U.K. ticked higher to 0.1% month-on-month (0.0% previous) and 0.2% year-on-year (0.1% previous), which are both really low.

Also, the annualized reading is apparently an 11-month high, which is saying a lot.

On a more upbeat note, the annualized core reading also climbed higher to an 11-month high of 1.4%. This marks the third consecutive month of increasing core CPI readings.

According to the details of the report, the biggest downward contributors to the annualized reading were the 0.2% fall in the price of food and non-alcoholic beverages (+0.3% previous).

Interestingly enough, the transport component was the main driver (+1.8% vs. -0.2% previous), due to a 46% increase in airfares, which is far bigger when compared with the previous year’s 19% increase. Also, fuel oil prices also fell at a slower rate across the board on a yearly basis.

The Eurozone

The final month-on-month reading for the euro zone’s CPI flattened out during December, but the annualized reading printed a 0.2%, the same pace as in the previous month.

As for the annualized core reading, it increased by 0.9%, which is also the same rate of increase as last time. Oil-related components were less of a drag on an annualized basis, with the “fuels for transport” component down by 8.3% in December when it was down by 11.1% back in November.

The “heating oil” component was also down by 22.0%, which is a slight improvement over the previous month’s reading of -23.8%.

Among the major eurozone economies, Germany had a downtick from 0.3% to 0.2% while France saw an increase from 0.1% to 0.3%. Like Germany, Italy also had a downtick from 0.2% to 0.1%. As for Spain, its CPI readings are still down in the dumps, but it did see an improvement. (-0.1% vs. -0.4% previous).

Switzerland

Switzerland’s headline CPI reading declined by 1.3% year-on-year in December, after printing a 1.4% decline for four consecutive months. Transport prices continued the trend of having slightly less of a negative impact (-4.7% vs. -4.9% previous).

All other components were either stagnant or had a negative contribution. Only the cost of clothing and footwear (+0.6%) and education (+0.9%) had a positive contribution.

Incidentally, the higher cost of clothing, footwear, and education allowed the core reading to print a slight improvement.

China

China’s headline CPI advanced at a slightly faster pace during the December period (1.6% vs. 1.5% previous) while the core reading held steady at 1.5%.

The “transportation and communication” component is still the sole drag to China’s annualized headline CPI, but it saw a very slight improvement since it was only down by 1.3% from 1.4% previously.

The recent slump in oil prices was a major drag to the monthly reading since the “fuels and parts for vehicles” sub-component was down by 2.2% whereas it was only down by 1.3% previously.

But the same sub-component was less of a drag on an annualized basis (-11.7% vs. -12.4 previous), but it’s still pretty horrible.

New Zealand

The headline reading for New Zealand’s Q4 2015 CPI was down by 0.5% quarter-on-quarter after advancing by 0.3% in the previous quarter.

On an annualized basis, this translates to a 0.1% increase (0.4% previous), which is the slowest rate of increase since Q3 1999.

That’s a long time! On an annualized reading petrol was the main drag, with its negative contribution of 8.1%. On a quarterly basis, petrol was still the main drag, with a downward contribution of -7.0%.

Japan

Japan’s headline annualized CPI was steady at 0.3% during the November period while the core (all items less fresh food) reading was up by 0.1% after printing a 0.1% decrease in the previous month.

As for the so-called “core-core” reading (all items less food and energy), it was up by 0.9% after printing a 0.7% increase in the previous month.

Energy-related components continue to be the main drags, with the “fuel, light and water charges” component down by 6.8% (-7.0% previous) while the “transportation and communication” component was down by 2.8% (-3.3% previous).

It’s worth noting, however, that energy was less of a drag, with the energy index only down by 11.1% (-11.8% previous).

For the newbie forex traders out there, the sudden drop after March 2015 was due to the 8.0% consumption tax that gave CPI got an artificial boost. Just subtract 2.0% from the readings for comparison purposes.

Summary

Overall, oil prices are still weighing in on all the major economies, but the recent slump in oil prices had the most noticeable impact on the monthly readings while the annualized readings of most economies showed that oil was less of a drag, but is still a drag nevertheless.

And the recent slump will likely cause the deflationary influence of the previous oil slumps to pass through much more slowly unless we see a major recovery or oil prices trade sideways for the next few months.