Konnichiwa, forex friends! The BOJ will be announcing its monetary policy statement this Thursday. That event is usually a dud, but since it’s been a while since I made an economic roundup for Japan, I though that now would be a good time to do just that, so here you go.

Growth

- The final estimate for Japan’s Q1 2017 GDP growth was revised lower from a 0.5% quarter-on-quarter rate of expansion to just 0.3%.

- Japan’s economy has been growing at a steady +0.3% clip for three consecutive quarters now.

- The final estimate was downgraded because private consumption was weaker than originally estimated (+0.3% vs, +0.4% originally) and the same can be said for private residential investment (+0.3% vs. +0.7% originally).

- Quarter versus quarter, private consumption still picked up (+0.3% vs. +0.0% in Q4).

- Private residential investment also picked up the pace (+0.3% vs. +0.2% in Q4).

- Stronger growth in the above two components were offset by weaker private non-residential investment (+0.6% vs. +1.9% in Q4) and weaker exports (+2.1% vs. +3.4% in Q4), which is why quarterly GDP growth maintained the +0.3% pace.

- Year-on-year, GDP grew by 1.3%, which is slower than the previous quarter’s +1.6% annual pace of growth.

- This puts an end to three consecutive quarters of ever faster annual growth after bottoming out at +0.5% back in Q1 2016.

- It’s also a tad slower compared to the BOJ’s forecast of +1.6% for the year, so the Japanese economy needs to hustle in order to meet the BOJ’s forecast.

- The slower annual growth was due to imports increasing by 1.3% after falling 2.0% back in Q4 2017.

- The 0.9% fall in government spending was also a drag since it rose by 0.4% back in Q4.

- And the same can be said of the weaker annual growth in private residential investment (+6.1% vs. +7.2% in Q4).

- As for the drivers, private consumption maintained its +0.9% pace while private non-residential investment (+3.6% vs. +3.3% previous) and exports (+6.0% vs. +4.6% previous) both grew at a faster pace.

Employment

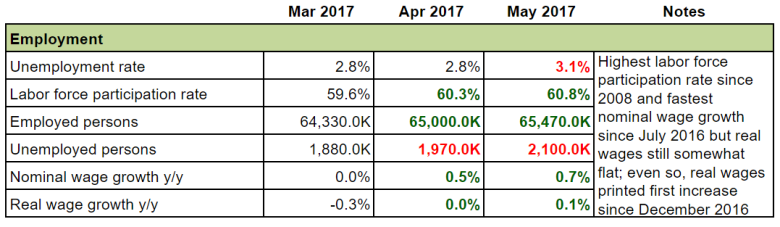

- Japan’s jobless rate jumped to from 2.8% to a five-month high of 3.1% in May.

- It’s not all bad, though, since the higher jobless rate was partially due to the labor force participation rate rising to 60.8%, which is a high not seen since early 2008.

- Also, the number of employed persons rose from 65 million to 65.47 million.

- This marks the fourth consecutive month of growing employment.

- The number of unemployed people did rise from 1.97 million to 2.1 million, though, so the Japanese economy wasn’t able to fully absorb the influx of new and returning workers.

- As for earnings, nominal wage growth accelerated in May by printing a 0.7% year-on-year increase.

- This marks the second month of wage growth after stagnant growth in March.

- In addition, this is the fastest annual growth in wages since July 2016.

- However, real wages (wages that take inflation into account) were still somewhat flat in May since it came in at +0.1%.

- Still, that’s a tick better than the flat reading in April and the negative reading recorded in March.

- Moreover, the 0.1% increase in May is also the first positive reading for real wages since December 2016.

Inflation

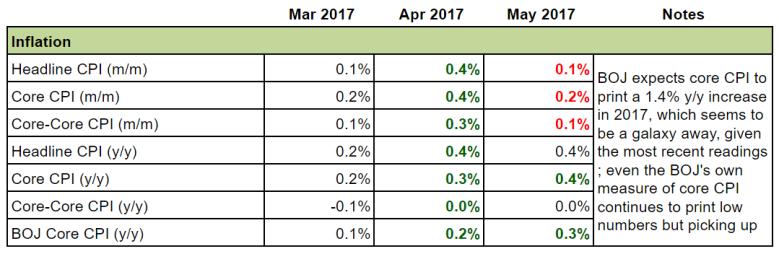

- Headline CPI ticked higher by 0.1% month-on-month in May, which is slower than the 0.4% increase in April.

- But on a slightly more optimistic note, headline monthly CPI has been in positive territory for three straight months after printing negative readings, also for three consecutive months.

- Even so, the weakness was broad-based, which is why both the core (headline less fresh food) and the so-called “core-core” (headline less food and energy) also took hits in May.

- Year-on-year, headline CPI increased by 0.4% in May, matching the increase reported in April.

- The main driver for annual CPI is the energy component while the slower increase in the cost of fresh food was one of the drags.

- That’s why the core reading, which excludes fresh food, picked up the pace while the “core-core” reading, which strips food and energy, printed another big, fat 0%.

- It should be noted, however, that the BOJ forecasts core CPI to print a 1.4% year-on-year increase in 2017, which seems to be a galaxy away, given the most recent readings.

- Speaking of the BOJ, the BOJ’s own measure of core CPI remains subdued.

- It’s appears to be picking up, though, since the +0.3% printed in May marks the second month of stronger readings and is the strongest reading since April 2016.

Business Conditions & Sentiment

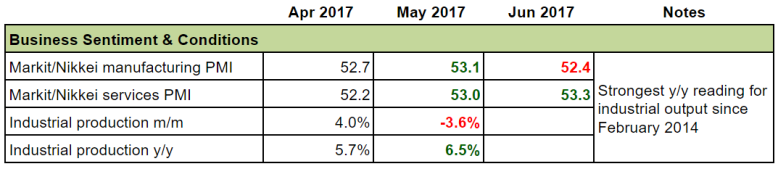

- Industrial production fell by 3.6% month-on-month in May after printing a solid 4.0% increase in April.

- This is the hardest drop in industrial production since March 2011.

Many industries took hits, with iron and steel production, electronic parts manufacturing, electrical machinery, transport equipment, and general purpose and business-oriented machinery production reporting the bulk of the loss in production. - On a year-on-year basis, however, industrial production surged by 6.5% since most components printed stronger readings on a year-on-year basis.

- This is the strongest reading since February 2014.

- It also marks the second month of stronger annual readings.

- Moreover, the annual reading for industrial production has been in positive territory for seven consecutive months now.

- Looking forward, manufacturing PMI from Markit-Nikkei fell from 53.1 to a three-month low of 52.4.

- Commentary from the PMI report blamed the weaker reading on weaker rises in both output and new orders.

- As for Japan’s services PMI, it rose from 53.0 to 53.3 in June.

- This is the best reading since August 2015 and marks the second month of improving readings.

- The PMI report attributed the stronger reading to a “solid” rise in both activity and new businesses, as well as the employment growing at the fastest pace in over four years.

Consumer Sentiment & Spending

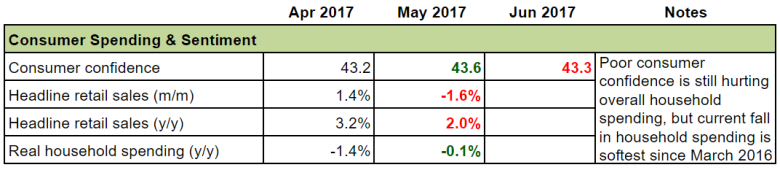

- Retail sales plunged by 1.6% month-on-month in May.

- This puts an end to four consecutive months of increases and is the hardest monthly drop since August 2016.

- Year-on-year, this translated to a 2.0% increase, which is a three-month low.

- However, seasonally-unadjusted total household spending in real terms (taking inflation into account) continues to fall, printing a 0.1% year-on-year decline in May.

- Household spending has been negative since March 2016.

- Even so, the reading in May is actually the softest decline since household spending turned negative in March 2016.

- Looking forward, consumer confidence in Japan eased from 43.6 to 43.3 in June.

- The improvement in confidence was broad-based, with increases in overall livelihood (42.0 vs. 40.7 previous), income growth (41.9 vs. 40.5 previous) and employment (45.7 vs. 42.5 previous).

- The slide in consumer confidence mainly reflected lower confidence in income growth and overall livelihood.

- This was partially offset by higher confidence in employment.

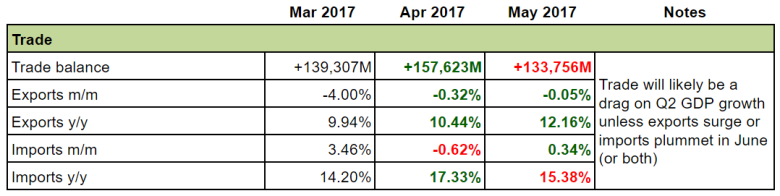

Trade

- Japan’s seasonally-adjusted trade surplus narrowed to ¥133,756 million in May.

- The trade surplus shrank because imports recovered after contracting previously (+0.34% vs. -0.62% previous), which was able to more than offset the weaker contraction in exports (-0.05% vs. -0.32% previous).

- Worse, trade will likely be a drag on Q2 GDP growth unless exports surge or imports plummet in June.

- And for reference, total surplus in Q1 was ¥886,018 million, thanks to the surge in exports back in February.

- In contrast, total surplus for the Q2 months amount to ¥291,379 million.

- Trade will also likely be a drag on the year-on-year reading since the trade surplus in Q2 2016 was ¥1,100,643.

- And again, total surplus for the Q2 2017 months amount to ¥291,379 million.

Putting it all together

Japan’s GDP growth of 1.3% year-on-year in Q1 was a not-so-good start towards the BOJ’s 1.6% forecast for GDP in 2017. And things currently don’t look so swell for Q2 since trade will likely be a drag on both quarter-and-quarter and year-on-year GDP growth. And the same can be said for retail sales, although total household spending shows that consumer spending will probably not be a problem, at least on year-on-year GDP growth.

As for inflation, the +0.4% year-on-year rise for the core CPI is really subdued. Heck, the BOJ’s own measure for core CPI came in at an even weaker +0.3%, which is a galaxy away from the BOJ’s super optimistic median forecast of 1.4% for 2017. It’s even weaker than the +0.6% forecast of the most pessimistic BOJ member out there, so I wouldn’t be surprise of the BOJ decides to scale down its CPI forecast a bit.

Looking forward, things do seem to look hopeful for inflation, though, since the PMI reports note that businesses are experiencing slightly higher costs, and more importantly, are passing on those higher costs. Wage growth also appears to be picking up slightly, although real wages are still pretty much flat.

Still, the BOJ has expressed (complained, to be more accurate) again and again that Japan still has a deflationary mindset. This influences inflation expectations and results in lower inflation. Basically, a self-fulfilling prophecy. As such, these weak signs that Japan is moving away from a deflationary mindset has an optimistic sparkle to it. It remains to be seen if these will be sustained, though.