Konnichiwa, forex friends!

The BOJ will be giving its monetary policy statement this Tuesday, so I thought that now would be a good time to give y’all an overview of how Japan’s economy is doing lately.

Note: As with all Economic Snapshots, there are nifty tables at the bottom, so you can skip to those if you’re a forex trader who’s in a hurry.

The bullet points provided highlight the underlying details and trends that give the numbers their proper context, however.

Growth

- No change from the previous Economic Snapshot of Japan

- The final estimate for Japan’s Q3 2016 GDP reading was revised lower from a 0.5% quarter-on-quarter expansion to just 0.3%.

- This marks the second quarter of weakening quarterly growth.

- The downgrade was due to private non-residential investments falling by 0.4% (+0.0% originally), weaker government spending (+0.3% vs. +0.4% originally), and weaker exports (+1.6% vs. +2.0% originally).

- These were partially offset by stronger consumer spending (+0.3% vs. +0.1% originally), stronger private residential investment (2.6% vs. 2.3% originally), and the 0.1% increase in government investment (-0.7% originally).

- Year-on-year, GDP grew by 1.1%, which is faster than the previous quarter’s 0.9% rate of expansion.

- The annual reading has been increasing at a faster pace for two consecutive quarters.

- On a year-on-year basis, inventories subtracted -0.3% from total GDP growth

- The only drag was the 1.8% drop in government investment (-2.2% previous), which subtracted 0.1% from total GDP growth.

- Net trade was the major driver, adding 0.7% to total GDP growth.

- In fact, net trade is also the reason why GDP grew at a faster annual rate since net trade only contributed +0.2% to total GDP growth in Q2.

- However, the larger contribution by net trade-in Q3 was due to imports slumping by 3.3% (-0.7% in Q2).

- Exports actually grew at a slower pace (+0.4% vs. +0.5% in Q2).

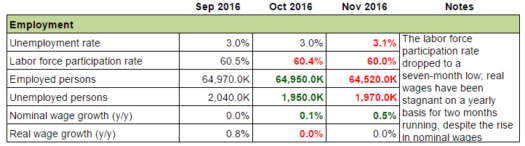

Employment

- Japan’s jobless deteriorated in November, ticking higher from 3.0% tp 3.1%.

- And the other labor indicators weren’t that good.

- First of all, the seasonally-unadjusted labor force fell from, 66.90 million to 66.49 million.

- Meanwhile, the working-age population held steady.

- As a result, the labor force participation rate dropped from 60.4% to 60.0%, a seven-month low.

- In addition, the number of employed people shrank from 64.95 million to 64.52 million.

- At the same time, the number of unemployed people rose from 1.95 million to 1.97 million.

- As for earnings, nominal wage growth accelerate in November, printing a 0.5% year-on-year increase after three consecutive months of stagnant growth.

- However, real wages (wages that take inflation into account) were stagnant for another month, which is a real disappointment.

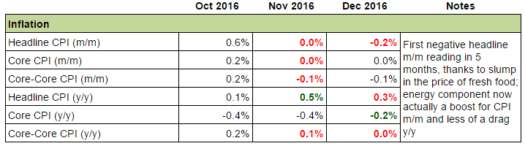

Inflation

- Headline CPI dipped by 0.2% month-on-month in December after stagnating in November.

- This is the first negative reading in 5 months.

- The negative reading was primarily due to the 0.9% drop in food prices (-0.1% previous).

- Fresh food, in particular, saw a 5.1% slump (-0.5% previous).

- Fresh food is stripped from the core reading, which is why the core reading stagnated.

- As for the so-called “core-core” reading (headline less food and energy), it fell by 0.1% month-on-month.

- That’s because the energy component is stripped from the “core-core” reading.

- And for reference, the cost of energy increased by 1.3% in December (+1.0% previous).

- Year-on-year, headline CPI increased by 0.3%, which is slower than November’s +0.5%.

- But on a more upbeat note, the yearly CPI readings have been in positive territory for three months running after six straight months of negative readings.

- Anyhow, the weaker increase in December was due to the slower increase in food prices (+2.5% vs. +3.6% previous).

- The rise in the price of fresh food items, in particular, saw a drastic slowdown (+13.8% vs. +21.6% previous).

- And since fresh food is not included in the core reading, the drop in the core reading for December ended up being softer (-0.2% vs. -0.4% previous).

- Other major drags to the headline reading are housing (-0.2%, same as previous) and energy (-4.4% vs. -6.7% previous).

- Energy and food items are not part of the “core-core” reading, which is why the reading was flat in December.

- In terms of trends, the core reading has been in negative territory on a year-on-year basis since March of this year.

- Meanwhile, the so-called “core-core” reading has been in positive territory since October 2013, with the stagnant readings for September and December being the only exceptions.

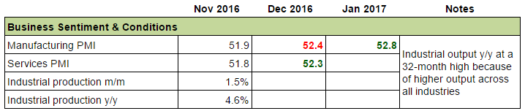

Business Conditions & Sentiment

- Industrial production jumped by 1.5% month-on-month in November after being stagnant in October.

- This puts an end to two straight months of deteriorating readings.

- In addition, November’s reading is the best reading in 8 months to boot.

- On a year-on-year basis, industrial production surged by 4.6% after contracting by 1.4% previously.

- This is a 32-month high and also puts an end to two straight months of deteriorating readings.

- The surge was due to industries reporting an increase in output across the board.

- Looking forward, the flash reading for Japan’s January manufacturing PMI from Markit-Nikkei improved further from 52.4 to 52.8.

- This is the best reading since March 2014.

- Manufacturing PMI has been trending ever higher after bottoming out at 47.7 back in May.

- Commentary from the PMI report noted that improvement was broad-based, since production, new orders, exports, sales, prices, and future expectations all improve while backlogs were fewer.

- More new work orders and higher output, in particular, were cited as the main reasons for the improved reading.

- Also, new export orders “rose at the quickest pace in over a year.“

- Moving on, Japan’s final services PMI jumped from 51.8 to 52.3 in December.

- December’s reading is an 11-month high.

- According to commentary from the PMI report, the jump was due to new orders increasing at the fastest rate since July 2015.

- Another good news is that “employment levels stabilized following a six-month period of job shedding.”

- Moreover, “cost burdens rose at the sharpest rate in nearly two years, while charges broadly stabilized.”

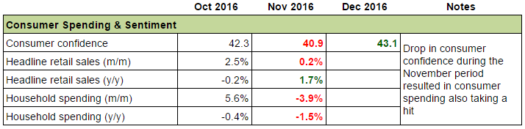

Consumer Sentiment & Spending

- After deteriorating for two months, consumer confidence in Japan jumped to 43.1 in December.

- This is a 39-month high.

- The improvement in confidence was broad-based, with increases in overall livelihood (42.0 vs. 40.7 previous), income growth (41.9 vs. 40.5 previous), and employment (45.7 vs. 42.5 previous).

- The drop in consumer confidence back in November took its toll since retail sales only increased by 0.2% month-on-month in November, which is a drastic slowdown from October’s +2.5%.

- On a more upbeat note, retail sales increased by 1.7% year-on-year.

- This is the first positive reading after eight straight months of negative readings.

- Also, this is the best reading since October 2015.

- However, seasonally-unadjusted total household spending in real terms (taking inflation into account), slumped by 3.9% month-on-month in November after increasing by 5.6% previously.

- On a year-on-year basis, total household spending fell by 1.5%.

- Total household spending has been in negative territory for nine months running already.

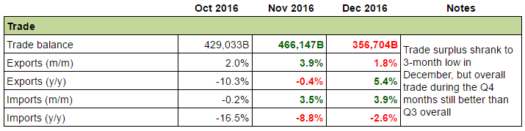

Trade

- Japan’s seasonally-adjusted trade surplus narrowed to ¥356,704 billion in December, a three-month low.

- The trade surplus shrank because exports grew at a weaker pace (+1.8% vs. +3.9% previous) while import growth accelerated (+3.9% vs. +3.5% previous).

- On a more upbeat note, the 1.8% month-on-month increase was enough to bring exports up to ¥6,165,409 billion, which is the highest figure since November 2015.

- That also the reason why exports surged by 5.4% year-on-year.

- Despite the 3.9% month-on-month increase in imports, meanwhile, imports have been contracting since January 2015.

- On a more upbeat note, the 2.6% year-on-year contraction is the softest decline, also since January 2015.

Putting it all together

Quarter-on-quarter GDP growth continues to slow, but year-on-year GDP growth continues to accelerate. And while Q3’s 1.1% year-on-year growth is already above the BOJ’s 2016 forecast range of +0.8% to +1.0%, it remains to be seen if Q4 could do the same.

Things are looking good (so far), though. For one, the monthly reading for industrial output in November is the best in 8 months while the annual reading is a 32-month high. These will contribute positively to quarter-on-quarter and year-on-year GDP growth respectively.

Consumer spending is more of a mixed picture since total household spending jumped in October but slumped in November. Average household spending during the available Q4 months is still higher on average compared to the Q3 months, however, so a positive contribution is also expected.

As for trade, the trade surplus shrank in December, but overall trade during the Q4 months is still better when compared to the Q3 months. Also, November’s trade surplus is the biggest reading since March 2011.

As for inflation, core CPI (all items less fresh food) fell by -0.2%. That’s obviously bad, but that sits right in the middle of the BOJ’s forecast range of -0.3% – -0.1%, so it’s no biggie. And looking forward, the PMI reports did not that prices were increasing, which should exert some inflationary pressure. However, this could be offset by the lack of growth in real wages.