Greetings, forex friends! Since there’s another ECB statement next week and most of the Euro Zone’s economic data are out, I thought that now would be a good time to give y’all a quick economic roundup.

Growth

- Final GDP estimate isn’t out yet, so no detailed GDP breakdown.

- With that said, the GDP of the Euro Zone as whole grew by 0.6% quarter-on-quarter in Q2 2017.

- This is a tick faster than Q1’s +0.5%.

- Looking at the available (yet incomplete data), stronger household spending among the Big Four Euro Zone economies seems to be the main driver.

- As for details, Germany printed a 0.8% increase (+0.4% previous), Spain printed a 0.7% rise (+0.4% previous), and Italy reported a 0.3% increase (+0.1% previous).

- French data not available yet.

- And for those who don’t know, the Big Four Euro Zone economies (In order from biggest: Germany, France, Italy, and Spain) account for around 76% of total GDP in the Euro Area.

- Getting back on topic, the stronger growth in consumer spending appears to have been partially offset by weaker growth in investments or fixed capital formation.

- Germany only printed a 1.0% increase (2.7% previous), +0.5% for France (+1.4% previous), and +0.8% for Spain (+2.1% previous).

- Italy’s fixed capital formation data not available yet.

- Moving on, the Euro Zone economy grew by 2.2% year-on-year.

- This is the fastest year-on-year growth in 25 quarters (or over six years).

- More importantly, the pace of annual growth is already faster than the ECB’s 2017 median forecast of 1.9%.

- It is still within the upper limit of the ECB’s forecast range of 1.6% to 2.2%, though.

- Again, no detailed breakdown yet, but looking at the available (yet incomplete data), stronger household spending appears to be a major driver again.

- And while gross fixed capital formation appears to be weaker quarter-on-quarter, the available data point to stronger investment growth year-on-year.

- Germany, in particular, printed an annual increase of 4.3% (+2.0% previous) in Q2.

- Stronger exports appear to be a driver as well.

- The stronger growth in exports wasn’t broad-based, though, since Germany printed weaker exports (+3.5% vs. +4.1% previous).

Inflation

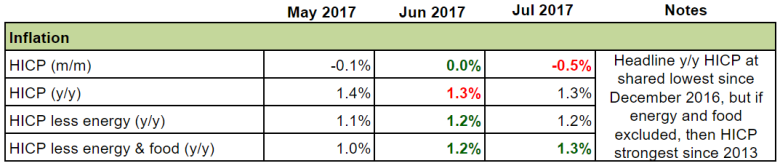

- Headline HICP slipped by -0.5% month-on-month in July.

- This is the steepest slide in six months.

- Most components took hits, with the 3.5% slump in the overall cost of non-energy industrial goods being the main drag.

- Year-on-year, HICP rose by 1.3% in July, which matched the annual pace set in June.

- This is a shared weakest reading since December 2016.

- Also, the ECB’s central projection is that HICP would print a 1.4% year-on-year increase in Q3, so the +1.3% printed in July is a poor start start.

- Even so, headline HICP averaged around 1.6% in 2017 (so far), so headline HICP is still beating the ECB’s forecast that headline HICP would average around 1.5% this year.

- Moving on, if food and energy prices are stripped from headline HICP to get at the underlying or core reading, then CPI actually accelerated from +1.2% to +1.3%.

- This is the strongest reading since August 2013.

- The ECB is forecasts that core HICP would average around 1.1% in 2017.

- So far, underlying HICP averages around 1.04%, so it’s getting there but there’s still room for improvement.

Business Conditions & Sentiment

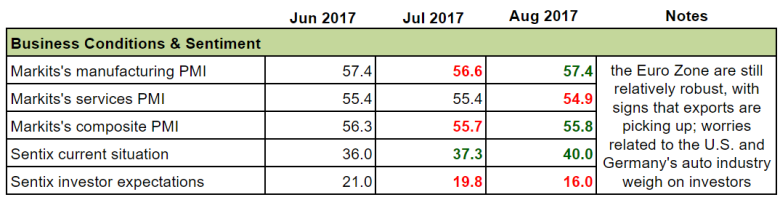

- According to Markit’s latest batch of PMI reports, the manufacturing PMI reading for the Euro Zone as a whole improved from 56.6 to 57.4.

- Commentary from Markit attributed the improving conditions in the manufacturing sector to “output and new orders rising at sharper rates in August.”

- New orders growth, in particular, “was boosted by the fastest rise in exports for six-and-a-half years.”

- Unfortunately, the services PMI reading deteriorated fom 55.4 to 54.9, which is a seven-month low.

- According to Markit, this was due to “growth of activity [easing] to a seven-month low.”

- Even so, Markit noted that the Euro Zone’s composite PMI ticked higher from 55.7 to 55.8.

- As such, the PMI readings are still positive overall.

- Also, additional commentary from Markit noted that “The latest PMI readings for the eurozone signal a continuation of the recent strong performance of the currency bloc’s economy. This stabilisation in the rate of expansion is pleasing, following signs of growth easing in recent months.”

- Moving on, the current conditions index from Sentix improved further to 40.0, which is in-line with Markit’s own findings.

- This is the highest reading since November 2007.

- However, investor expectations are falling even as economic conditions in the Euro Zone improve.

- According to Sentix, weaker expectations are related mostly to the U.S., although investors are worried mainly about Germany’s auto sector.

Consumer Spending & Labor Market

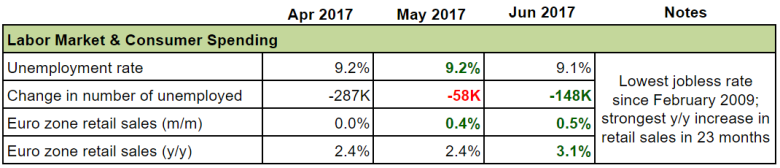

- The jobless rate for the whole Euro Zone ticked lower from 9.2% to 9.1% during the June period.

- This is the best and lowest reading since February 2009, which is great.

- Trend-wise, the jobless rate peaked at 12.1% during the April 2013 period and has been steadily sliding lower ever since, with only one uptick during all that time.

- The slide in the jobless rate appears to be healthy since the number of unemployed Europeans fell by 148K to 14,718K.

- Improving labor market conditions apparently translated into higher consumer spending, since retail sales volume in the Euro Zone jumped by 0.5% month-on-month in June.

- The increase in retail sales volume was due mainly to the sales of food, drinks, and tobacco rebounding by 0.7% (-0.2% previous).

- The 1.0% surge in sales reported by fuel stores also helped (+0.6% previous), although most other retail store types printed stronger sales as well.

- On a year-on-year basis, retail sales volume jumped by 3.1% (+2.4% previous).

- This is the strongest year-on-year increase in 23 months.

- The strong annual reading was driven mainly by the 3.5% increase in sales reported by automotive fuel stores (-0.6% previous).

- Other store types reported stronger sales as well, particularly sales of food, drinks, and tobacco (+3.1% vs. +2.4% previous).

Trade

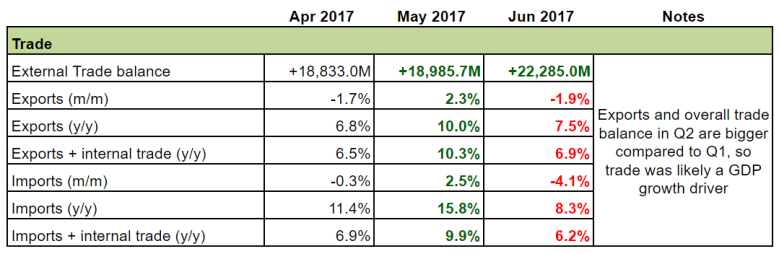

- The Euro Zone’s external trade surplus widened to €22,285 million in June.

- This is the widest trade surplus in 6 months.

- Exports actually fell by 1.9% month-on-month in June, but imports dropped by a harder 4.1%, which is why the trade surplus widened.

- Now that we have the trade data for June, we now know that the trade surplus for all of Q2 was 9.85% more compared to Q1, so trade was likely a driver.

Putting it all together

GDP growth in Q2 was really solid, especially the year-on-year reading, which is the strongest year-on-year reading in over six years, so it’s no real wonder why business sentiment remains high.

And while we don’t have the GDP breakdown yet, available (but incomplete) data are already hinting that stronger net trade and consumer spending were the main drivers while weaker business investment was the likely drag.

The strong net trade is noteworthy because of the euro’s recent strength, although there are signs that the stronger euro may already be having a negative effect since exports fell in June. It just so happens that imports dropped much harder, which is why the trade surplus still widened.

As such, it’s only right that “concerns were expressed about the risk of the exchange rate overshooting in the future,” as revealed in the latest ECB minutes.

With regard to inflation, the month-on-month slide in July is a bad start for Q3. Year-on-year, HICP rose by 1.3% in July, which matched the annual pace set in June. But this is a shared weakest reading since December 2016.

Moreover, the ECB’s central projection is that HICP would print a 1.4% year-on-year increase in Q3, so Q3 really is off to a poor start. But it’s not too bad.

Also, headline HICP averaged around 1.6% in 2017, so headline HICP is still beating the ECB’s forecast that headline HICP would average around 1.5% this year.

As for the core reading, the ECB tracks HICP less energy and food prices. And so far, that’s still subdued but the uptick from +1.2% to +1.3% is promising since it’s the strongest reading since August 2013.

However, the ECB expects core HICP to average around 1.1% in 2017. And so far, core HICP has yet to hit the mark since average core HICP is only 1.04%. It’s been inching higher, though, so there’s room for improvement.